Last Updated May 8, 2026

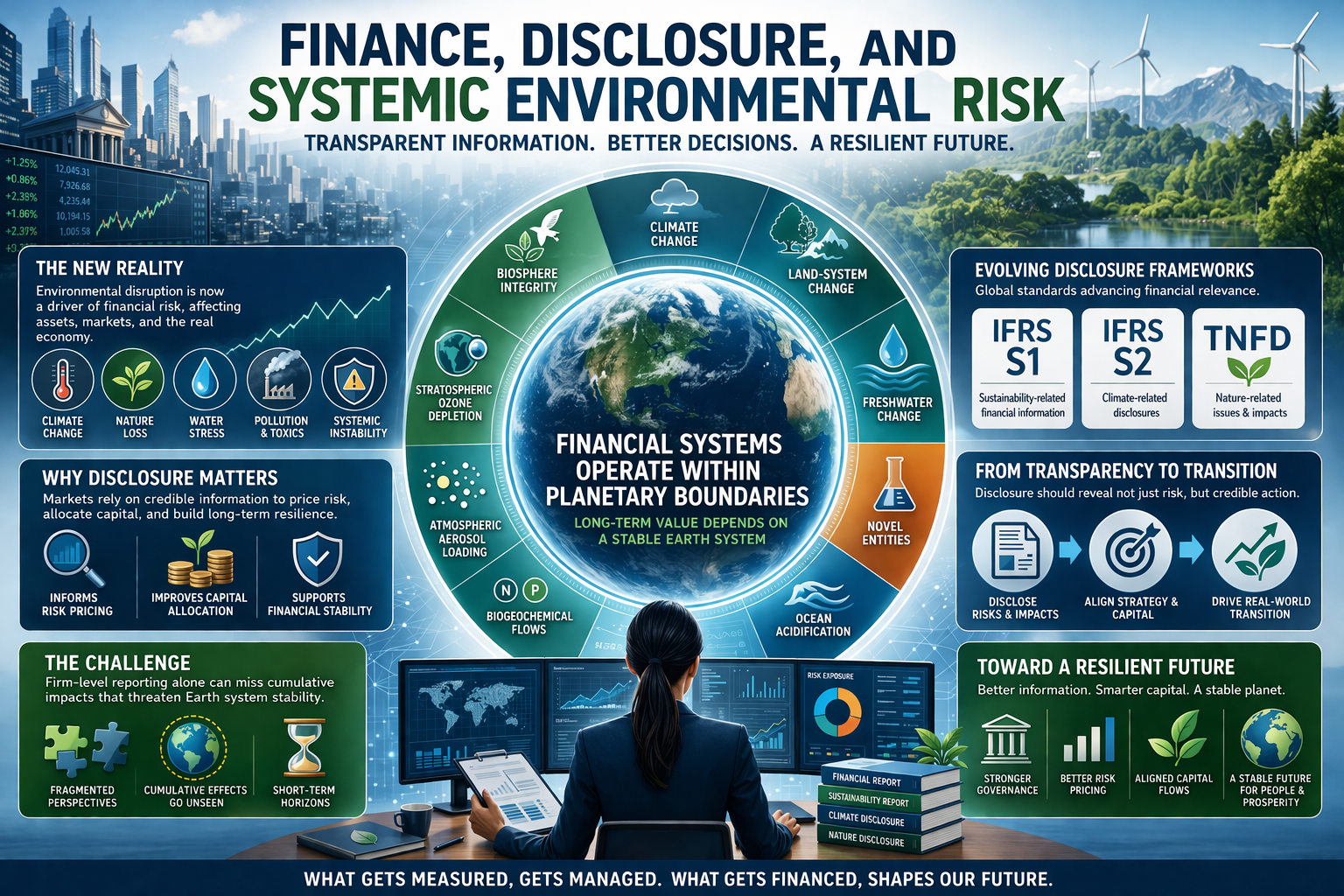

Finance, disclosure, and systemic environmental risk now belong together because environmental disruption is no longer a peripheral sustainability topic. It is increasingly a source of economy-wide instability affecting asset values, credit quality, insurance pricing, supply chains, infrastructure, regulation, sovereign risk, public budgets, and long-term growth. The planetary boundaries framework sharpens this point by showing that firms and financial systems operate inside a finite Earth system whose stability depends on a small number of interdependent biophysical processes. When those processes are destabilized, risk does not remain confined to isolated projects, sectors, or corporate balance sheets. It can propagate across portfolios, markets, institutions, and public systems.

This is why disclosure matters so much. Financial systems depend on information to price risk, allocate capital, assess future viability, manage solvency, evaluate transition credibility, and distinguish real risk reduction from risk transfer. If disclosure frameworks capture only narrow firm-level impacts while missing cumulative and systemic environmental pressures, they can understate the scale of the risk being financed. Current reporting frameworks represent important progress, but they also expose a larger challenge: how to make financial disclosure adequate to Earth-system instability rather than to firm-level optics alone.

Main Library

Publications

Article Map

Planetary Boundaries

Related Article

Business Strategy

Related Article

Earth-System Governance

Related Topic

Economic Systems

The central issue is not whether sustainability-related disclosure has improved. It has. IFRS S1 and IFRS S2 have made sustainability-related and climate-related financial disclosures more formal, comparable, and decision-oriented. TNFD has expanded the conversation beyond climate to nature-related dependencies, impacts, risks, and opportunities. Transition-plan guidance has also strengthened attention to whether firms can credibly adapt their strategies, capital expenditure, governance, and operating models to a lower-carbon and more climate-resilient economy. But planetary boundaries raise a deeper question: can entity-level disclosure frameworks capture systemic environmental risk when the most serious risks arise from cumulative pressures across firms, sectors, regions, portfolios, supply chains, and Earth-system processes?

This article examines finance, disclosure, and systemic environmental risk by explaining why environmental risk is increasingly systemic, how disclosure frameworks are evolving in response, why firm-level materiality can still miss cumulative Earth-system pressures, how finance changes when planetary boundaries are taken seriously, and what this means for investors, firms, regulators, engineers, analysts, insurers, auditors, and the governance of capital in an age of ecological overshoot.

Why Environmental Risk Becomes Systemic

Environmental risk becomes systemic when it affects not just individual firms or projects, but the wider conditions under which whole sectors and markets function. Climate instability can impair infrastructure, insurance markets, labor productivity, agriculture, energy reliability, sovereign fiscal stability, and financial stability. Nature loss can affect water systems, food production, raw materials, ecological resilience, disease dynamics, and social conflict. Pollution and novel entities can create regulatory, liability, and health burdens that propagate well beyond the point of original release. These are not merely local environmental incidents. They can alter the background conditions of economic coordination itself.

This is why the language of systemic environmental risk has become more important than narrower sustainability language. A company may experience a specific physical loss, but that loss may also signal wider instability affecting correlated assets, lenders, insurers, suppliers, workers, public budgets, and communities. The more environmental disruption affects multiple actors through shared Earth-system conditions, the less plausible it becomes to treat the problem as a series of isolated firm-level exposures.

Systemic risk also matters because it undermines a core financial assumption: that diversification can sufficiently manage exposure. Diversification works best when shocks are imperfectly correlated. But Earth-system disruption increasingly creates correlated stress across regions, sectors, and asset classes. A destabilized climate, degraded biosphere, or disrupted hydrological system can transmit pressure through food systems, commodity markets, logistics, migration, sovereign risk, and insurance simultaneously. At that point, finance is not dealing with isolated sustainability incidents. It is dealing with threats to the stability of the investment environment itself.

Planetary boundaries make this systemic character visible. Climate change, biosphere integrity, freshwater change, land-system change, biogeochemical flows, ocean acidification, aerosol loading, ozone depletion, and novel entities are not separate accounting categories. They are interacting Earth-system processes. Financial risk frameworks that isolate climate from water, biodiversity, land, chemicals, food systems, infrastructure, and public health may therefore miss the way environmental pressures amplify each other.

The systemic character of environmental risk also means that private risk management and public risk management cannot be cleanly separated. When insurers withdraw from exposed geographies, governments may become insurers of last resort. When food-system shocks spread through commodity markets, public budgets and household welfare are affected. When climate or nature risks impair infrastructure, local governments, lenders, households, and firms are exposed together. Finance therefore needs to understand environmental risk as part of a broader political economy of instability.

For companion essays, see Planetary Boundaries and Earth System Resilience, Tipping Points, Feedback Loops, and Cascading Ecological Change, and Earth System Governance in an Age of Limits.

Why Disclosure Matters to Finance

Disclosure matters to finance because financial systems depend on credible information about present exposure and future prospects. Investors, creditors, insurers, auditors, regulators, and boards need to understand what could affect enterprise value, solvency, funding costs, resilience, and strategic viability. Sustainability-related disclosure standards have become more significant precisely because environmental disruption is no longer a peripheral concern. They help make environmental risk more legible to financial decision-makers, but they also reveal the difficulty of translating Earth-system instability into entity-level reporting.

In principle, better disclosure should improve capital allocation by reducing opacity and helping markets recognize environmental risk earlier. But disclosure does not automatically produce adequate risk recognition. It depends on what is measured, what counts as material, what time horizon is used, what assumptions define transition risk, whether nature dependencies are considered, whether supply-chain impacts are included, and whether the framework captures cumulative system effects or only firm-specific exposures.

This is where disclosure becomes more than a reporting exercise. It becomes part of the informational infrastructure of finance. Markets can only respond to risks that become legible in forms recognized by accounting, supervision, governance, audit, insurance, ratings, and investment practice. If Earth-system disruption is poorly represented in disclosure, capital may continue to flow toward activities that intensify instability even while investors believe they are making informed decisions.

Disclosure also shapes institutional accountability. Boards and executives cannot credibly claim to manage sustainability-related risk if they cannot describe the exposures, dependencies, assumptions, metrics, and transition plans that define their strategy. Regulators cannot supervise systemic risk if information remains fragmented. Investors cannot price long-run resilience if reporting focuses only on near-term financial impacts. In that sense, disclosure is not merely a transparency tool. It is part of the governance architecture through which environmental risk becomes financially actionable.

Yet disclosure must be treated carefully. More data does not automatically mean better judgment. A disclosure regime can be detailed but still incomplete, comparable but still ecologically thin, audited but still too narrow, or decision-useful for one investor while failing to reveal system-wide destabilization. The goal is not disclosure volume. The goal is disclosure that makes risk, dependency, impact, uncertainty, and transition credibility visible enough to inform decisions that matter.

Finance therefore needs disclosure that can support three linked questions: how environmental change affects the entity, how the entity affects environmental stability, and whether the entity’s transition pathway is credible under plausible Earth-system and policy conditions.

From Firm-Level Risk to Earth-System Risk

A central challenge in sustainable finance is the difference between firm-level risk and Earth-system risk. Firm-level risk asks how environmental change affects the reporting entity. Earth-system risk asks whether the aggregate activities of firms and financiers are destabilizing the ecological systems on which the economy itself depends. These are related but not identical questions. A portfolio can be constructed to manage near-term financial exposure while still financing cumulative pressures that intensify long-run systemic instability.

This distinction is one reason the planetary boundaries framework matters for finance. It highlights that the economy is nested inside the Earth system, not outside it. Once that is recognized, disclosure cannot stop with enterprise resilience alone. It also has to ask whether financed activities are compatible with the stability of the systems that make future returns possible.

This gap between entity risk and system risk is one of the main reasons conventional financial logic can appear rational in the short term while remaining ecologically destabilizing in aggregate. Each firm may disclose what matters to its own prospects. Each lender may assess its own portfolio. Each investor may hedge sector-specific exposure. Yet the sum of these individually rational decisions may still finance patterns of overshoot that threaten macroeconomic stability. Earth-system risk exposes the limits of firm-bounded financial reasoning.

The distinction also matters for portfolio construction. A portfolio can reduce exposure to high-risk firms by divesting or reallocating, but the underlying systemic risk may remain if the economy as a whole continues to exceed ecological limits. This creates a difference between risk transfer and risk reduction. Finance can move exposure around without reducing the aggregate environmental pressure that produces systemic risk in the first place.

This matters especially for universal owners, pension funds, sovereign wealth funds, insurers, development banks, and public financial institutions. Such actors are exposed to broad economic performance, public stability, and cross-sector conditions. They cannot fully diversify away from a destabilized Earth system. For them, systemic environmental risk is not only an issue of portfolio selection. It is a question of whether capital allocation contributes to the stability of the economy in which returns are generated.

| Risk lens | Core question | What it can miss |

|---|---|---|

| Firm-level financial risk | How could environmental change affect this entity’s prospects? | Cumulative pressures created by many firms across sectors and supply chains. |

| Portfolio exposure | How exposed is this portfolio to environmental risk? | Risk transferred away from one portfolio may remain in the economy as systemic instability. |

| Disclosure adequacy | Is reported information decision-useful, comparable, and auditable? | Disclosure may be complete within its scope while the scope remains too narrow. |

| Earth-system risk | Are financed activities compatible with planetary stability? | Requires aggregation, thresholds, value-chain data, scenario analysis, and boundary logic. |

Planetary-boundary finance therefore has to hold two views at once: the view from the reporting entity and the view from the Earth system. Without both, disclosure can become more sophisticated while capital remains ecologically misaligned.

Current Disclosure Frameworks and Their Significance

Current disclosure frameworks represent a major shift in how environmental information is treated in finance. Sustainability-related and climate-related reporting requirements are increasingly being formalized within a global reporting architecture tied to financial prospects through the ISSB’s IFRS S1 and IFRS S2 standards. Nature-related disclosure has also advanced through TNFD’s recommendations, which provide a risk-management and disclosure framework for nature-related dependencies, impacts, risks, and opportunities.

The significance lies not only in standardization, but in what the change reveals about the current transition. Finance is moving from a world in which environmental disclosure was often discretionary, partial, and reputational toward one in which sustainability-related information is increasingly treated as relevant to financial decision-making, risk management, and oversight. That is a major institutional change, even if it remains incomplete.

For decades, sustainability information often sat beside financial reporting rather than within its core logic. Newer frameworks signal that environmental conditions can no longer be treated as optional context. They are becoming part of the architecture through which markets evaluate prospects, resilience, and stewardship. Climate, nature, water, land, biodiversity, and transition credibility are moving closer to the domains of accounting, audit, governance, and supervision.

The incomplete part is equally important. Disclosure frameworks still operate through reporting entities, materiality judgments, jurisdictional adoption, sector-specific implementation, data availability, assurance systems, and governance practices. They make systemic environmental risk more visible, but they do not automatically translate planetary boundaries into capital-allocation rules. Disclosure is necessary infrastructure for transition, not the transition itself.

Disclosure frameworks also differ in scope and purpose. IFRS S1 and S2 are focused on sustainability-related and climate-related financial disclosures useful to users of general-purpose financial reports. TNFD extends structured attention to nature-related dependencies, impacts, risks, and opportunities. NGFS scenarios support climate-related financial-risk analysis for central banks and supervisors. These tools are complementary, but none of them alone supplies a complete planetary-boundary finance system.

The emerging challenge is interoperability: how climate disclosure, nature disclosure, transition-plan disclosure, scenario analysis, portfolio data, and planetary-boundary diagnostics can be combined without producing fragmented reporting that is too complex to govern and too narrow to reveal systemic risk.

What IFRS S1 and S2 Do and Do Not Solve

IFRS S1 and S2 help by creating a clearer baseline for reporting sustainability-related and climate-related financial information. IFRS S1 establishes overarching disclosure requirements for sustainability-related risks and opportunities that could reasonably be expected to affect an entity’s prospects. IFRS S2 sets out specific climate-related disclosure requirements, including disclosures related to governance, strategy, risk management, metrics, targets, and climate resilience.

But these standards do not fully solve the problem of systemic environmental risk. Their core logic remains anchored in what could reasonably be expected to affect the reporting entity’s prospects. That is highly consequential, but it can leave a gap between what is financially material to the firm and what is materially destabilizing to the Earth system. A firm may comply with disclosure requirements while the aggregate activities of its sector remain misaligned with planetary stability.

This is not a flaw unique to one reporting standard. It is a structural difficulty in translating Earth-system risk into entity-based reporting. Financial disclosure frameworks are designed around the organization as the reporting unit. Planetary instability is driven by cumulative activity across many units, many sectors, many supply chains, and many jurisdictions. The result is that disclosure can become more rigorous while still remaining only partially adequate to the scale of the problem.

The practical implication is that IFRS S1 and S2 should be understood as foundational but not sufficient. They improve the quality of sustainability-related and climate-related financial information, but planetary-boundary thinking asks additional questions. Are reported strategies compatible with absolute ecological limits? Do disclosed targets reduce system pressure or merely improve relative performance? Are financed emissions, land impacts, water dependencies, and nature-related risks addressed across value chains? Are transition plans credible under plausible policy, technology, physical-risk, and liability scenarios?

IFRS S2 also matters because transition disclosure increasingly connects strategy to future viability. If a firm has climate-related transition plans, the usefulness of disclosure depends on whether those plans are linked to governance, targets, capital expenditure, business-model changes, assumptions, dependencies, and scenario analysis. A transition plan that is not connected to investment decisions and risk management is not a strategy. It is a narrative.

Planetary-boundary finance therefore treats IFRS S1 and S2 as part of a broader information architecture. They help make entity-level sustainability and climate information decision-useful, but the next step is connecting that information to system-level environmental pressure, portfolio aggregation, nature dependencies, and transition credibility.

TNFD and the Rise of Nature-Related Disclosure

Nature-related disclosure is important because it expands financial attention beyond climate into dependencies, impacts, risks, and opportunities associated with ecosystems, biodiversity, land, freshwater, oceans, soil, and wider ecological systems. TNFD’s recommendations are designed to provide companies and financial institutions with a framework to identify, assess, manage, and disclose nature-related issues. This matters because many financially relevant environmental risks are mediated through nature rather than through climate alone.

Water stress, ecosystem degradation, land conversion, soil decline, biodiversity loss, and disrupted ecological functions can affect agriculture, infrastructure, health, logistics, commodity prices, and social stability. Nature-related disclosure also helps correct a major weakness in climate-centered sustainable finance. A financial system can make progress on carbon visibility while remaining blind to other Earth-system processes that are equally important for long-run resilience.

At the same time, nature-related disclosure is difficult precisely because ecological systems are heterogeneous, place-based, interdependent, and less easily reduced to one dominant metric than climate. This makes TNFD especially significant. It attempts to build an analytical bridge between ecological complexity and financial reporting practice. That effort is still evolving, but it marks an important step toward a broader understanding of systemic environmental risk.

TNFD also brings location into financial analysis more directly. Nature-related dependencies and impacts often cannot be understood without knowing where activity occurs. A water-intensive facility in a water-abundant basin is different from the same facility in a stressed watershed. A supply chain dependent on land conversion has a different risk profile depending on biome, governance context, Indigenous land rights, biodiversity value, and regulatory exposure. Planetary-boundary finance therefore requires not only better metrics, but better spatial intelligence.

Nature-related disclosure also highlights the relationship between finance and justice. Land conversion, biodiversity loss, ecosystem degradation, and water stress frequently affect communities whose rights, knowledge, and livelihoods are tied to specific places. A financial risk framework that treats nature only as an asset base or dependency can miss social conflict, rights claims, Indigenous stewardship, and unequal exposure. Better nature disclosure should therefore connect ecological conditions with governance, rights, and accountability.

Climate remains central, but climate-only finance is too narrow for a planetary-boundary world. Nature-related disclosure moves finance closer to the fuller architecture of Earth-system risk.

Why Cumulative Impacts Are Hard to Disclose

Cumulative impacts are hard to disclose because financial reporting is built around entities, while planetary destabilization is driven by aggregates, interactions, and thresholds. A company can disclose its own risk management and exposure, but that does not automatically show whether the sum of many firms’ activities is pushing climate, water, biodiversity, or chemical pressures beyond safer ranges. In business terms, the reporting unit and the ecological unit often do not line up.

This is exactly why planetary-boundary thinking matters for business and finance. Anchoring corporate activities in the planetary boundaries framework requires fuller and more accurate information about corporate environmental performance because what gets measured shapes what gets done. But the measurement challenge is difficult: corporate accounts, financial disclosures, value-chain data, portfolio holdings, and Earth-system indicators are not naturally organized around the same boundaries.

Cumulative effects are also difficult because they are often delayed, indirect, and distributed across jurisdictions. A bank financing agricultural expansion, a logistics firm enabling higher throughput, a chemical producer increasing persistent pollutants, and an insurer underwriting environmentally fragile growth may each see only part of the picture. Yet the Earth system receives the whole. Disclosure that remains fragmented by legal entity can therefore obscure the aggregate destabilization being financed.

There is also a time-horizon problem. Many environmental pressures accumulate slowly and then express themselves through nonlinear shocks, threshold effects, regulatory changes, litigation, asset impairment, insurance repricing, or social conflict. Financial reporting systems built around annual cycles can struggle to represent long-lag systemic pressures. That does not make them irrelevant. It means they need to be supplemented by scenario analysis, stress testing, boundary-alignment assessment, value-chain impact accounting, and portfolio-level aggregation.

Cumulative impacts are also difficult because value chains overlap. The same physical activity may appear across multiple portfolios, supply chains, insurers, lenders, and buyers. This creates risks of double counting, undercounting, and responsibility diffusion. A credible disclosure architecture needs clear accounting boundaries, attribution logic, source provenance, and uncertainty treatment. Without those, cumulative-risk analysis can become either too vague to guide decisions or too precise to be credible.

The central difficulty is therefore not only data availability. It is conceptual fit. Financial disclosure must learn to speak across the boundaries between legal entities, portfolios, value chains, ecosystems, jurisdictions, and planetary processes.

Finance Under Conditions of Planetary Overshoot

Once planetary overshoot is recognized, finance itself has to be reinterpreted. Capital markets are not just passive observers of environmental disruption. They help shape it through lending, underwriting, investment, insurance, valuation, and stewardship. If capital continues to flow toward activities that deepen overshoot, then finance is not merely exposed to systemic environmental risk. It is also helping reproduce that risk.

This changes the meaning of fiduciary prudence and risk governance. The question is no longer only whether environmental disruption will affect portfolios. It is also whether portfolios are financing activities incompatible with the Earth-system conditions on which long-run portfolio stability depends. That is a harder question, but it is the one planetary-boundary thinking pushes finance to confront.

This also means that finance cannot treat planetary instability only as an exogenous shock. In many cases, financial systems are deeply implicated in the scaling of high-emission infrastructure, land transformation, chemically intensive production, and extractive growth models. Under conditions of overshoot, finance becomes both a conduit of instability and a potential lever of transition. That dual role gives disclosure even greater importance, because the informational architecture of finance influences whether capital remains locked into overshoot or begins to move differently.

The systemic character of environmental risk also complicates conventional fiduciary reasoning. If every investor tries to avoid the worst exposed assets while the overall system continues to destabilize, the result may be relative portfolio protection without systemic resilience. Universal owners, long-term asset owners, insurers, pension funds, development banks, and public financial institutions therefore face a different problem than short-horizon traders. They cannot fully diversify away from a destabilized Earth system.

Finance under conditions of planetary overshoot therefore requires a distinction between avoiding risk and reducing risk. Avoiding risk may protect a balance sheet temporarily. Reducing systemic risk requires changing the real economy activities that produce ecological destabilization. Disclosure can help distinguish these two strategies, but only if it includes the information needed to evaluate whether capital allocation is actually shifting system pressure.

For companion essays, see Business Strategy Within Planetary Boundaries, Planetary Boundaries, Justice, and Global Inequality, and Planetary Boundaries and Doughnut Economics.

Capital Allocation, Pricing, and Systemic Misalignment

Disclosure is ultimately relevant because it shapes capital allocation and pricing. If environmental risks are underdisclosed, delayed, or framed too narrowly, markets may continue to underprice ecological instability and overfinance fragile business models. Conversely, better disclosure can help reveal transition risk, physical exposure, dependency on stressed ecosystems, and misalignment with emerging policy or social expectations.

Yet there remains a deeper issue of systemic misalignment. Even well-disclosed markets can continue to fund overshoot if the decision rules remain short-term, fragmented, or focused only on relative performance. Finance, in other words, can become more transparent without becoming adequately planetary. The challenge is not just to disclose more. It is to disclose in ways that make capital markets more responsive to absolute ecological conditions.

Systemic misalignment arises when financial logic continues to reward activities that generate returns under assumptions of ecological underpricing, delayed regulation, weak liability regimes, or unstable but still functioning Earth systems. The longer those assumptions persist in capital allocation, the more likely finance is to amplify the eventual disorder of transition. In that sense, mispricing is not only a market imperfection. It is part of how systemic environmental risk accumulates.

Planetary-boundary finance therefore requires a distinction between relative improvement and absolute alignment. A company may reduce emissions intensity while total emissions continue to rise. A portfolio may outperform peers on ESG scores while still financing activities that exceed ecological ceilings. A bank may improve disclosure while its lending remains locked into land conversion, fossil infrastructure, or chemical expansion. Systemic alignment requires asking whether capital flows are moving toward activities compatible with stable Earth-system conditions, not simply whether reporting has improved.

This also affects valuation. Cash-flow models, discount rates, terminal values, collateral assessments, and credit ratings often depend on assumptions about future operating conditions. If those assumptions fail to account for ecological destabilization, regulatory tightening, insurance withdrawal, water stress, litigation, infrastructure impairment, or nature-related dependency, valuation can overstate durability. Planetary-boundary finance therefore asks whether pricing models are embedding a false picture of environmental stability.

Capital allocation becomes credible only when it distinguishes between activities that are profitable because they solve transition problems and activities that are profitable because ecological costs remain externalized. That distinction is one of the central tests of financial strategy in an age of overshoot.

From Disclosure to Transition Credibility

One of the next challenges for finance is moving from disclosure quality to transition credibility. It is no longer enough for firms and financial actors simply to report exposure. They increasingly need to show whether their strategies, financing choices, governance systems, and capital plans are compatible with credible transition pathways. Transition-plan disclosure guidance reflects that shift by moving attention from static reporting toward the substance of strategic adaptation.

Transition credibility matters because capital markets are not evaluating static entities. They are evaluating organizations embedded in changing ecological, regulatory, technological, and political conditions. A firm that discloses major climate or nature exposure without a credible transition strategy may be more informative than before, but it is not necessarily more resilient. Likewise, an investor that maps risks without changing allocation logic may be disclosing exposure while continuing to fund instability.

In this sense, disclosure is becoming less about sustainability signaling and more about whether organizations can justify their future viability. The stronger the evidence for planetary overshoot becomes, the more disclosure will be judged not only by completeness, but by whether it supports believable adaptation to finite Earth-system conditions.

Credibility depends on the relationship between stated goals and actual financial decisions. A transition plan is weak if capital expenditure, lending, underwriting, procurement, lobbying, executive incentives, and product strategy remain misaligned with the stated pathway. A credible plan should therefore connect governance, metrics, targets, investment, risk management, and accountability. It should also show how uncertainty is handled and what would trigger course correction.

Transition credibility also requires attention to dependencies. A firm may disclose that its transition depends on grid decarbonization, new technologies, policy incentives, supplier action, carbon removal, minerals access, water availability, or customer adoption. Those dependencies should be treated as strategic assumptions, not footnotes. If a plan depends on uncertain external conditions, investors and regulators need to understand the risk that the plan cannot be implemented as stated.

Financial actors face the same challenge. A bank, asset manager, insurer, or pension fund may publish climate or nature commitments, but credibility depends on portfolio construction, stewardship, engagement escalation, sector exclusions, underwriting criteria, policy advocacy, and the treatment of high-impact assets. Disclosure becomes meaningful only when it can be traced into the decisions that allocate capital.

Scenario Analysis, Stress Testing, and Model Risk

Scenario analysis and stress testing are essential because systemic environmental risk cannot be understood only through historical data. The past is not a stable guide when climate systems, ecosystems, legal regimes, technologies, policies, and social expectations are changing together. Financial institutions therefore need forward-looking tools that explore physical risk, transition risk, nature-related risk, disorderly adjustment, policy delay, and tail-risk conditions.

NGFS climate scenarios are one important example of this forward-looking infrastructure. They help central banks, supervisors, and financial institutions explore how the global economy and financial system might evolve under different levels of climate-policy ambition and physical climate impacts. But scenario tools must be used with methodological humility. They depend on assumptions, models, damage functions, socioeconomic pathways, technology pathways, policy pathways, and uncertain physical-risk estimates.

This is not a reason to reject scenario analysis. It is a reason to treat scenarios as structured decision tools rather than predictions. A scenario is useful when it helps institutions ask better questions: what happens if transition is delayed, if physical losses intensify, if insurance retreat accelerates, if nature-related risks compound climate stress, if regulation tightens suddenly, or if multiple regions experience correlated shocks?

Scenario analysis also reveals the limits of purely climate-centered financial risk. Climate scenarios are indispensable, but planetary-boundary finance also needs to incorporate nature loss, freshwater disruption, land pressure, nutrient loading, chemical risks, and novel entities. A climate-only stress test may miss risks that travel through agriculture, public health, water systems, litigation, ecosystem services, and supply-chain fragility.

Model risk is therefore part of environmental-risk governance. If a model understates physical damages, omits tipping dynamics, ignores ecosystem dependencies, downplays tail risks, or treats social stability as exogenous, it can create false confidence. Good disclosure should document not only scenario results, but assumptions, limitations, uncertainty, and decision use. The question is not whether a model can produce a number. It is whether the number is interpreted with enough humility to guide prudent action.

Scenario analysis should therefore be linked to governance triggers. If a scenario reveals unacceptable exposure, what changes? Are lending criteria revised? Are underwriting standards tightened? Are capital buffers reconsidered? Are engagement plans escalated? Are transition assumptions updated? Without such links, scenario analysis becomes a technical exercise rather than a governance tool.

What Better Disclosure Would Need to Do

Better disclosure would need to do at least six things. First, it would need to connect firm-level reporting to Earth-system conditions more explicitly. Second, it would need to improve treatment of cumulative effects and value-chain dependencies. Third, it would need to extend time horizons beyond narrow near-term materiality. Fourth, it would need to help markets distinguish between business models that are merely well managed today and those that are actually viable within finite ecological limits. Fifth, it would need to make assumptions auditable so analysts can understand how thresholds, scenarios, transition pathways, and nature-risk judgments were constructed. Sixth, it would need to connect disclosure to actual capital-allocation decisions.

This does not mean every disclosure regime should become a full planetary-accounting system overnight. But it does mean disclosure should increasingly illuminate not only how environmental change affects firms, but how firms and financiers affect environmental stability. Without that two-way perspective, financial reporting will struggle to capture systemic environmental risk with the seriousness it now requires.

Better disclosure would also need stronger interoperability across climate, nature, and wider sustainability-related reporting so that risk is not split into disconnected silos. It would need more comparable metrics where comparison is possible, more contextual interpretation where simple comparison is misleading, and more explicit treatment of uncertainty where Earth-system dynamics cannot be reduced to precise short-term forecasts. In short, it would need to become both broader and more ecologically literate.

For engineers and data teams, this implies a major infrastructure challenge. Disclosure systems need data lineage, source validation, versioned assumptions, threshold registries, spatial joins, scenario libraries, portfolio mapping, audit trails, uncertainty fields, and reproducible exports. The question is not simply whether a report contains the right words. It is whether the underlying information architecture can support decision-grade analysis.

For regulators and standard-setters, the challenge is to make disclosure useful without pretending that disclosure alone solves systemic risk. Rules can improve transparency, comparability, and accountability, but they must be complemented by supervision, prudential analysis, stewardship expectations, transition-plan scrutiny, assurance, and public policy capable of reducing the real-economy pressures that disclosure reveals.

Better disclosure is therefore not a decorative reporting exercise. It is infrastructure for systemic risk governance. Its purpose is to help capital see the planet on which capital depends.

Why This Matters for Planetary Boundaries

Finance matters for planetary boundaries because capital allocation helps determine which infrastructures, technologies, supply chains, land uses, extraction systems, and business models expand. If finance continues to treat planetary instability as an externality, disclosure may improve while the real economy remains misaligned. If finance begins to recognize planetary boundaries as strategic and systemic constraints, capital can become part of the transition toward lower pressure and greater resilience.

Planetary boundaries matter for finance because they expose the limits of firm-level risk thinking. A financial system can diversify, disclose, hedge, and reprice selected risks while still depending on a destabilizing Earth system. That is not resilience. It is a form of accounting sophistication inside a deteriorating material context.

The strongest interpretation is therefore not disclosure as reputation management, nor sustainability reporting as a supplement to financial analysis. It is disclosure as infrastructure for understanding the relationship between capital allocation and Earth-system stability. The task is to make the environmental conditions of finance visible, auditable, and actionable.

This matters because the financial system cannot diversify away from an unstable planet. It can only transfer selected exposures temporarily. Long-run financial stability depends on reducing the systemic pressures that make portfolios, economies, and public systems fragile in the first place.

Planetary-boundary finance therefore asks whether disclosure, valuation, stewardship, underwriting, lending, investment, insurance, and regulation are evolving quickly enough to recognize the truth that Earth-system stability is not external to finance. It is one of finance’s deepest dependencies.

Mathematical Lens: Portfolio Exposure, Boundary Pressure, and Disclosure Adequacy

Systemic environmental risk can be modeled as a relationship between portfolio exposure, boundary pressure, disclosure adequacy, transition credibility, and uncertainty. Let \(E_{p,i}\) represent portfolio \(p\)’s exposure to environmental pressure \(i\), where \(i\) may refer to climate, land-system change, freshwater stress, biodiversity loss, nitrogen surplus, chemical pollution, or another boundary-relevant process. Let \(B_i\) represent a safe or policy-relevant threshold for that pressure. A simple boundary-pressure ratio can be written as:

P_{p,i} = \frac{E_{p,i}}{B_i}

\]

Interpretation: If \(P_{p,i} < 1\), the portfolio’s exposure is below the selected threshold. If \(P_{p,i} > 1\), it exceeds the threshold.

Disclosure adequacy can be represented as a score \(D_{p,i}\) between 0 and 1, where higher values indicate more complete, decision-useful, and auditable disclosure. A disclosure-adjusted exposure score can then be written as:

R_{p,i} = P_{p,i} \times (1 + (1 – D_{p,i}))

\]

Interpretation: High boundary pressure is more dangerous when disclosure is weak because the risk is both elevated and poorly visible.

Transition credibility can be added. Let \(T_{p,i}\) represent the credibility of transition plans associated with portfolio exposure \(i\). A transition-adjusted score becomes:

Q_{p,i} = R_{p,i} \times (1 + (1 – T_{p,i}))

\]

Interpretation: Risk rises when boundary pressure is high, disclosure is weak, and transition plans lack credibility.

Uncertainty should also be explicit. Let \(U_{p,i}\) represent uncertainty in exposure, threshold, disclosure, or transition assumptions. An uncertainty-adjusted risk score can be written as:

Z_{p,i} = Q_{p,i} \times (1 + U_{p,i})

\]

Interpretation: High uncertainty increases governance concern when exposure is already material and disclosure is incomplete.

A systemic portfolio score can then be represented as:

Z_p = \sum_{i=1}^{n} w_i Z_{p,i}

\]

Interpretation: \(w_i\) represents the weight assigned to each boundary-relevant pressure based on severity, uncertainty, irreversibility, exposure, or transition relevance.

Finally, a real-economy impact adjustment can distinguish risk transfer from risk reduction. Let \(A_p\) represent the degree to which capital allocation in portfolio \(p\) is aligned with reducing real-economy pressure, scaled from 0 to 1:

S_p = Z_p \times (1 – A_p)

\]

Interpretation: Portfolio risk is more concerning when exposure is high and capital allocation is not credibly reducing real-economy boundary pressure.

| Term | Meaning | Analytical role |

|---|---|---|

| \(E_{p,i}\) | Portfolio exposure to environmental pressure \(i\) | Captures financed or portfolio-linked exposure. |

| \(B_i\) | Boundary or policy-relevant threshold | Represents the selected safe, fair, or regulatory benchmark. |

| \(P_{p,i}\) | Boundary-pressure ratio | Shows whether exposure exceeds the selected threshold. |

| \(D_{p,i}\) | Disclosure adequacy | Represents completeness, auditability, comparability, and decision usefulness. |

| \(T_{p,i}\) | Transition credibility | Represents whether disclosed plans are believable and linked to capital decisions. |

| \(U_{p,i}\) | Uncertainty | Captures data, threshold, scenario, model, and interpretation uncertainty. |

| \(A_p\) | Real-economy alignment | Distinguishes risk transfer from risk reduction. |

This mathematical lens is not a substitute for financial analysis, ecological science, or regulatory judgment. Its purpose is to clarify the architecture of the problem. Systemic environmental risk depends not only on exposure, but on the adequacy of disclosure systems that make exposure visible, comparable, auditable, and actionable.

Advanced Python Workflow: Portfolio-Level Boundary and Disclosure Risk Scoring

The following Python workflow models portfolio-level systemic environmental risk by combining boundary pressure, disclosure quality, transition credibility, uncertainty, and real-economy alignment. It is illustrative rather than definitive, but it shows how financial institutions, analysts, or sustainability teams could build an auditable scoring pipeline.

"""

Portfolio-level boundary and disclosure risk scoring.

This workflow models systemic environmental risk by combining:

- portfolio exposure

- boundary-relevant thresholds

- disclosure adequacy

- transition credibility

- uncertainty penalties

- real-economy alignment

The data are illustrative. Replace them with documented issuer data,

portfolio holdings, emissions data, nature-related metrics, audited

disclosures, and institution-specific thresholds before applied use.

"""

from __future__ import annotations

from dataclasses import dataclass

from pathlib import Path

from typing import Literal

import numpy as np

import pandas as pd

BoundaryDomain = Literal[

"climate",

"water",

"land",

"biosphere",

"nitrogen",

"novel_entities",

]

@dataclass(frozen=True)

class BoundarySpec:

"""Metadata for a boundary-relevant risk domain."""

domain: BoundaryDomain

threshold: float

weight: float

unit: str

rationale: str

def build_boundary_specs() -> dict[str, BoundarySpec]:

"""Create illustrative boundary-domain metadata."""

specs = [

BoundarySpec(

domain="climate",

threshold=1.0,

weight=1.5,

unit="portfolio pressure index",

rationale="Climate transition and physical risk proxy",

),

BoundarySpec(

domain="water",

threshold=1.0,

weight=1.1,

unit="portfolio pressure index",

rationale="Water stress and dependency proxy",

),

BoundarySpec(

domain="land",

threshold=1.0,

weight=1.0,

unit="portfolio pressure index",

rationale="Land conversion and land-use intensity proxy",

),

BoundarySpec(

domain="biosphere",

threshold=1.0,

weight=1.3,

unit="portfolio pressure index",

rationale="Biodiversity and ecosystem dependency proxy",

),

BoundarySpec(

domain="nitrogen",

threshold=1.0,

weight=0.9,

unit="portfolio pressure index",

rationale="Nutrient pollution exposure proxy",

),

BoundarySpec(

domain="novel_entities",

threshold=1.0,

weight=1.2,

unit="portfolio pressure index",

rationale="Chemical and synthetic-material risk proxy",

),

]

return {spec.domain: spec for spec in specs}

def build_sample_portfolio() -> pd.DataFrame:

"""

Create illustrative issuer-domain exposure data.

Scores are scaled:

- exposure_pressure: 0 means no pressure; values above 1 exceed threshold

- disclosure_adequacy: 0 means poor disclosure; 1 means strong disclosure

- transition_credibility: 0 means weak transition credibility; 1 means strong credibility

- uncertainty: 0 means low uncertainty; 1 means high uncertainty

- real_economy_alignment: 0 means no credible pressure reduction; 1 means strong alignment

"""

return pd.DataFrame(

{

"issuer": [

"Utility A",

"Agribusiness B",

"Chemicals C",

"Infrastructure D",

"Bank E",

"Retail F",

"Insurer G",

],

"portfolio_weight": [0.16, 0.15, 0.14, 0.18, 0.20, 0.09, 0.08],

"domain": [

"climate",

"land",

"novel_entities",

"water",

"climate",

"biosphere",

"water",

],

"exposure_pressure": [1.45, 1.25, 1.70, 1.10, 1.35, 0.95, 1.20],

"disclosure_adequacy": [0.70, 0.42, 0.35, 0.62, 0.78, 0.50, 0.55],

"transition_credibility": [0.55, 0.38, 0.30, 0.58, 0.64, 0.45, 0.48],

"uncertainty": [0.25, 0.40, 0.50, 0.30, 0.20, 0.35, 0.45],

"real_economy_alignment": [0.52, 0.34, 0.25, 0.55, 0.60, 0.42, 0.46],

}

)

def score_issuer_domain_risk(

portfolio: pd.DataFrame,

specs: dict[str, BoundarySpec],

) -> pd.DataFrame:

"""Score issuer-level systemic environmental risk."""

scored = portfolio.copy()

scored["boundary_threshold"] = scored["domain"].map(

lambda domain: specs[domain].threshold

)

scored["domain_weight"] = scored["domain"].map(

lambda domain: specs[domain].weight

)

if scored["boundary_threshold"].isna().any():

missing = scored.loc[scored["boundary_threshold"].isna(), "domain"].unique()

raise ValueError(f"Missing boundary specifications for domains: {missing}")

scored["boundary_pressure_ratio"] = (

scored["exposure_pressure"] / scored["boundary_threshold"]

)

scored["disclosure_gap"] = 1 - scored["disclosure_adequacy"]

scored["transition_gap"] = 1 - scored["transition_credibility"]

scored["alignment_gap"] = 1 - scored["real_economy_alignment"]

scored["risk_score"] = (

scored["boundary_pressure_ratio"]

* (1 + scored["disclosure_gap"])

* (1 + scored["transition_gap"])

* (1 + scored["uncertainty"])

* (1 + scored["alignment_gap"])

* scored["domain_weight"]

)

scored["portfolio_contribution"] = (

scored["portfolio_weight"] * scored["risk_score"]

)

scored["risk_class"] = pd.cut(

scored["portfolio_contribution"],

bins=[-np.inf, 0.30, 0.60, 1.00, np.inf],

labels=["lower", "moderate", "elevated", "severe"],

)

scored["priority"] = np.select(

[

scored["disclosure_adequacy"] < 0.45,

scored["transition_credibility"] < 0.45,

scored["uncertainty"] > 0.45,

scored["real_economy_alignment"] < 0.40,

scored["boundary_pressure_ratio"] > 1.25,

],

[

"improve_disclosure_quality",

"assess_transition_plan_credibility",

"reduce_uncertainty_and_model_risk",

"strengthen_real_economy_alignment",

"reduce_boundary_pressure_exposure",

],

default="maintain_monitoring_and_engagement",

)

return scored.sort_values(

"portfolio_contribution",

ascending=False,

).reset_index(drop=True)

def summarize_portfolio(scored: pd.DataFrame) -> tuple[pd.DataFrame, pd.DataFrame]:

"""Create portfolio-level and domain-level summaries."""

domain_summary = (

scored.groupby("domain")

.agg(

portfolio_weight=("portfolio_weight", "sum"),

weighted_risk=("portfolio_contribution", "sum"),

mean_disclosure_adequacy=("disclosure_adequacy", "mean"),

mean_transition_credibility=("transition_credibility", "mean"),

mean_uncertainty=("uncertainty", "mean"),

mean_real_economy_alignment=("real_economy_alignment", "mean"),

)

.reset_index()

.sort_values("weighted_risk", ascending=False)

)

total_risk = scored["portfolio_contribution"].sum()

portfolio_summary = pd.DataFrame(

{

"portfolio_systemic_environmental_risk": [total_risk],

"weighted_disclosure_adequacy": [

np.average(

scored["disclosure_adequacy"],

weights=scored["portfolio_weight"],

)

],

"weighted_transition_credibility": [

np.average(

scored["transition_credibility"],

weights=scored["portfolio_weight"],

)

],

"weighted_uncertainty": [

np.average(

scored["uncertainty"],

weights=scored["portfolio_weight"],

)

],

"weighted_real_economy_alignment": [

np.average(

scored["real_economy_alignment"],

weights=scored["portfolio_weight"],

)

],

}

)

return portfolio_summary, domain_summary

def run_sensitivity(scored: pd.DataFrame) -> pd.DataFrame:

"""

Test sensitivity to disclosure, transition, and alignment assumptions.

This is useful because risk scores often depend heavily on whether

analysts trust disclosure and transition-plan evidence.

"""

scenarios = {

"baseline": {

"disclosure_multiplier": 1.0,

"transition_multiplier": 1.0,

"alignment_multiplier": 1.0,

},

"skeptical_disclosure": {

"disclosure_multiplier": 0.8,

"transition_multiplier": 1.0,

"alignment_multiplier": 1.0,

},

"skeptical_transition": {

"disclosure_multiplier": 1.0,

"transition_multiplier": 0.8,

"alignment_multiplier": 1.0,

},

"skeptical_alignment": {

"disclosure_multiplier": 1.0,

"transition_multiplier": 1.0,

"alignment_multiplier": 0.8,

},

"stress_case": {

"disclosure_multiplier": 0.75,

"transition_multiplier": 0.75,

"alignment_multiplier": 0.75,

},

}

frames = []

for scenario_name, params in scenarios.items():

scenario = scored.copy()

scenario["scenario"] = scenario_name

scenario["adjusted_disclosure"] = (

scenario["disclosure_adequacy"] * params["disclosure_multiplier"]

).clip(0, 1)

scenario["adjusted_transition"] = (

scenario["transition_credibility"] * params["transition_multiplier"]

).clip(0, 1)

scenario["adjusted_alignment"] = (

scenario["real_economy_alignment"] * params["alignment_multiplier"]

).clip(0, 1)

scenario["adjusted_risk_score"] = (

scenario["boundary_pressure_ratio"]

* (1 + (1 - scenario["adjusted_disclosure"]))

* (1 + (1 - scenario["adjusted_transition"]))

* (1 + scenario["uncertainty"])

* (1 + (1 - scenario["adjusted_alignment"]))

* scenario["domain_weight"]

)

scenario["adjusted_portfolio_contribution"] = (

scenario["portfolio_weight"] * scenario["adjusted_risk_score"]

)

frames.append(scenario)

return pd.concat(frames, ignore_index=True)

def main() -> None:

"""Run the portfolio boundary-risk workflow."""

output_dir = Path(

"articles/finance-disclosure-and-systemic-environmental-risk/outputs"

)

output_dir.mkdir(parents=True, exist_ok=True)

specs = build_boundary_specs()

portfolio = build_sample_portfolio()

scored = score_issuer_domain_risk(portfolio, specs)

portfolio_summary, domain_summary = summarize_portfolio(scored)

sensitivity = run_sensitivity(scored)

scored.to_csv(output_dir / "issuer_domain_boundary_risk.csv", index=False)

portfolio_summary.to_csv(output_dir / "portfolio_summary.csv", index=False)

domain_summary.to_csv(output_dir / "domain_summary.csv", index=False)

sensitivity.to_csv(output_dir / "sensitivity_analysis.csv", index=False)

display_columns = [

"issuer",

"domain",

"portfolio_weight",

"boundary_pressure_ratio",

"disclosure_adequacy",

"transition_credibility",

"uncertainty",

"real_economy_alignment",

"portfolio_contribution",

"risk_class",

"priority",

]

print("\nIssuer-domain boundary risk:")

print(scored[display_columns].round(3).to_string(index=False))

print("\nPortfolio summary:")

print(portfolio_summary.round(3).to_string(index=False))

print("\nDomain summary:")

print(domain_summary.round(3).to_string(index=False))

if __name__ == "__main__":

main()

This workflow separates exposure, disclosure quality, transition credibility, uncertainty, real-economy alignment, and portfolio contribution. That separation matters because a portfolio can appear low risk if disclosure is treated as complete, but high risk if disclosure quality is weak, transition plans are not credible, or capital allocation is not reducing real-economy pressure.

The workflow also creates domain summaries so analysts can see whether risk is concentrated in climate, water, land, biosphere, nitrogen, or novel-entity pressures. This is important because different domains require different governance responses. Climate risk may require transition-plan scrutiny and scenario analysis. Water risk may require basin-level exposure analysis. Novel-entity risk may require chemical-risk mapping and regulatory monitoring. Biodiversity risk may require spatial ecological data and supply-chain traceability.

Advanced R Workflow: Disclosure Adequacy and Systemic Risk Dashboarding

The following R workflow prepares a dashboard-ready view of issuer-level environmental risk, disclosure adequacy, transition credibility, uncertainty, real-economy alignment, and portfolio contribution. It is designed for reporting teams that need to compare issuers, domains, and scenarios without collapsing the entire analysis into a single opaque score.

# Portfolio-level systemic environmental risk dashboard

#

# This workflow combines:

# - boundary pressure

# - disclosure adequacy

# - transition credibility

# - uncertainty

# - real-economy alignment

# - portfolio weight

#

# Values are illustrative and should be replaced with documented data.

library(readr)

library(dplyr)

library(tidyr)

portfolio <- tibble::tibble(

issuer = c(

"Utility A",

"Agribusiness B",

"Chemicals C",

"Infrastructure D",

"Bank E",

"Retail F",

"Insurer G"

),

portfolio_weight = c(0.16, 0.15, 0.14, 0.18, 0.20, 0.09, 0.08),

domain = c(

"climate",

"land",

"novel_entities",

"water",

"climate",

"biosphere",

"water"

),

exposure_pressure = c(1.45, 1.25, 1.70, 1.10, 1.35, 0.95, 1.20),

disclosure_adequacy = c(0.70, 0.42, 0.35, 0.62, 0.78, 0.50, 0.55),

transition_credibility = c(0.55, 0.38, 0.30, 0.58, 0.64, 0.45, 0.48),

uncertainty = c(0.25, 0.40, 0.50, 0.30, 0.20, 0.35, 0.45),

real_economy_alignment = c(0.52, 0.34, 0.25, 0.55, 0.60, 0.42, 0.46)

)

boundary_specs <- tibble::tibble(

domain = c(

"climate",

"water",

"land",

"biosphere",

"nitrogen",

"novel_entities"

),

boundary_threshold = c(1, 1, 1, 1, 1, 1),

domain_weight = c(1.5, 1.1, 1.0, 1.3, 0.9, 1.2)

)

scored <- portfolio %>%

left_join(boundary_specs, by = "domain") %>%

mutate(

boundary_pressure_ratio = exposure_pressure / boundary_threshold,

disclosure_gap = 1 - disclosure_adequacy,

transition_gap = 1 - transition_credibility,

alignment_gap = 1 - real_economy_alignment,

risk_score = boundary_pressure_ratio *

(1 + disclosure_gap) *

(1 + transition_gap) *

(1 + uncertainty) *

(1 + alignment_gap) *

domain_weight,

portfolio_contribution = portfolio_weight * risk_score,

risk_class = case_when(

portfolio_contribution < 0.30 ~ "lower",

portfolio_contribution < 0.60 ~ "moderate",

portfolio_contribution < 1.00 ~ "elevated",

TRUE ~ "severe"

),

priority = case_when(

disclosure_adequacy < 0.45 ~

"improve_disclosure_quality",

transition_credibility < 0.45 ~

"assess_transition_plan_credibility",

uncertainty > 0.45 ~

"reduce_uncertainty_and_model_risk",

real_economy_alignment < 0.40 ~

"strengthen_real_economy_alignment",

boundary_pressure_ratio > 1.25 ~

"reduce_boundary_pressure_exposure",

TRUE ~

"maintain_monitoring_and_engagement"

)

)

domain_summary <- scored %>%

group_by(domain) %>%

summarise(

portfolio_weight = sum(portfolio_weight),

weighted_risk = sum(portfolio_contribution),

mean_disclosure_adequacy = mean(disclosure_adequacy),

mean_transition_credibility = mean(transition_credibility),

mean_uncertainty = mean(uncertainty),

mean_real_economy_alignment = mean(real_economy_alignment),

.groups = "drop"

) %>%

arrange(desc(weighted_risk))

issuer_summary <- scored %>%

arrange(desc(portfolio_contribution))

portfolio_summary <- scored %>%

summarise(

portfolio_systemic_environmental_risk = sum(portfolio_contribution),

weighted_disclosure_adequacy = weighted.mean(

disclosure_adequacy,

portfolio_weight

),

weighted_transition_credibility = weighted.mean(

transition_credibility,

portfolio_weight

),

weighted_uncertainty = weighted.mean(

uncertainty,

portfolio_weight

),

weighted_real_economy_alignment = weighted.mean(

real_economy_alignment,

portfolio_weight

)

)

scenario_parameters <- tibble::tibble(

scenario = c(

"baseline",

"skeptical_disclosure",

"skeptical_transition",

"skeptical_alignment",

"stress_case"

),

disclosure_multiplier = c(1.00, 0.80, 1.00, 1.00, 0.75),

transition_multiplier = c(1.00, 1.00, 0.80, 1.00, 0.75),

alignment_multiplier = c(1.00, 1.00, 1.00, 0.80, 0.75)

)

scenario_scores <- scored %>%

crossing(scenario_parameters) %>%

mutate(

adjusted_disclosure = pmin(

1,

disclosure_adequacy * disclosure_multiplier

),

adjusted_transition = pmin(

1,

transition_credibility * transition_multiplier

),

adjusted_alignment = pmin(

1,

real_economy_alignment * alignment_multiplier

),

adjusted_risk_score = boundary_pressure_ratio *

(1 + (1 - adjusted_disclosure)) *

(1 + (1 - adjusted_transition)) *

(1 + uncertainty) *

(1 + (1 - adjusted_alignment)) *

domain_weight,

adjusted_portfolio_contribution = portfolio_weight * adjusted_risk_score

)

scenario_summary <- scenario_scores %>%

group_by(scenario) %>%

summarise(

total_adjusted_portfolio_risk = sum(adjusted_portfolio_contribution),

weighted_adjusted_disclosure = weighted.mean(

adjusted_disclosure,

portfolio_weight

),

weighted_adjusted_transition = weighted.mean(

adjusted_transition,

portfolio_weight

),

weighted_adjusted_alignment = weighted.mean(

adjusted_alignment,

portfolio_weight

),

.groups = "drop"

) %>%

arrange(desc(total_adjusted_portfolio_risk))

dashboard_long <- scored %>%

select(

issuer,

domain,

portfolio_weight,

boundary_pressure_ratio,

disclosure_adequacy,

transition_credibility,

uncertainty,

real_economy_alignment,

portfolio_contribution

) %>%

pivot_longer(

cols = c(

boundary_pressure_ratio,

disclosure_adequacy,

transition_credibility,

uncertainty,

real_economy_alignment,

portfolio_contribution

),

names_to = "metric",

values_to = "value"

)

output_dir <- "articles/finance-disclosure-and-systemic-environmental-risk/outputs"

dir.create(

output_dir,

recursive = TRUE,

showWarnings = FALSE

)

write_csv(

scored,

file.path(output_dir, "r_issuer_scores.csv")

)

write_csv(

domain_summary,

file.path(output_dir, "r_domain_summary.csv")

)

write_csv(

issuer_summary,

file.path(output_dir, "r_issuer_summary.csv")

)

write_csv(

portfolio_summary,

file.path(output_dir, "r_portfolio_summary.csv")

)

write_csv(

scenario_scores,

file.path(output_dir, "r_scenario_scores.csv")

)

write_csv(

scenario_summary,

file.path(output_dir, "r_scenario_summary.csv")

)

write_csv(

dashboard_long,

file.path(output_dir, "r_dashboard_long.csv")

)

print(domain_summary)

print(portfolio_summary)

print(scenario_summary)

This R workflow is designed for transparency. It does not treat disclosure adequacy, transition credibility, real-economy alignment, boundary pressure, and uncertainty as interchangeable. Instead, it gives analysts a structure for seeing where risk arises. A high-risk issuer may be problematic because exposure is high, because disclosure is weak, because the transition plan lacks credibility, because uncertainty is large, because real-economy alignment is poor, or because the issuer represents a large share of the portfolio. Each explanation implies a different governance response.

The scenario output also matters. If risk increases sharply when disclosure, transition, or alignment assumptions are made more skeptical, the portfolio may be relying on fragile claims. That is precisely the kind of issue disclosure analysis should reveal before it becomes a repricing event, supervisory concern, or litigation risk.

Advanced Go Workflow: Lightweight Portfolio-Risk Scoring Service

The following Go workflow translates disclosure adequacy and systemic environmental risk diagnostics into a lightweight scoring service. Go is useful for command-line tools, internal APIs, disclosure-quality checks, portfolio screening, and operational risk dashboards. This example reads issuer-domain records from a CSV file and reports boundary pressure, risk score, portfolio contribution, risk class, and recommended priority.

package main

import (

"encoding/csv"

"errors"

"fmt"

"os"

"strconv"

)

type IssuerExposure struct {

Issuer string

PortfolioWeight float64

Domain string

ExposurePressure float64

DisclosureAdequacy float64

TransitionCredibility float64

Uncertainty float64

RealEconomyAlignment float64

}

func parseFloat(value string) (float64, error) {

parsed, err := strconv.ParseFloat(value, 64)

if err != nil {

return 0, fmt.Errorf("invalid numeric value %q: %w", value, err)

}

return parsed, nil

}

func parseIssuerExposure(row []string) (IssuerExposure, error) {

if len(row) < 8 {

return IssuerExposure{}, errors.New("expected at least 8 columns")

}

values := make([]float64, 6)

for i := 1; i < 7; i++ {

parsed, err := parseFloat(row[i])

if err != nil {

return IssuerExposure{}, err

}

values[i-1] = parsed

}

return IssuerExposure{

Issuer: row[0],

PortfolioWeight: values[0],

Domain: row[2],

ExposurePressure: values[1],

DisclosureAdequacy: values[2],

TransitionCredibility: values[3],

Uncertainty: values[4],

RealEconomyAlignment: values[5],

}, nil

}

func domainWeight(domain string) float64 {

switch domain {

case "climate":

return 1.5

case "water":

return 1.1

case "land":

return 1.0

case "biosphere":

return 1.3

case "nitrogen":

return 0.9

case "novel_entities":

return 1.2

default:

return 1.0

}

}

func boundaryThreshold(domain string) float64 {

// Illustrative normalized threshold.

return 1.0

}

func boundaryPressureRatio(item IssuerExposure) float64 {

threshold := boundaryThreshold(item.Domain)

if threshold <= 0 {

return 0

}

return item.ExposurePressure / threshold

}

func riskScore(item IssuerExposure) float64 {

disclosureGap := 1 - item.DisclosureAdequacy

transitionGap := 1 - item.TransitionCredibility

alignmentGap := 1 - item.RealEconomyAlignment

return boundaryPressureRatio(item) *

(1 + disclosureGap) *

(1 + transitionGap) *

(1 + item.Uncertainty) *

(1 + alignmentGap) *

domainWeight(item.Domain)

}

func portfolioContribution(item IssuerExposure) float64 {

return item.PortfolioWeight * riskScore(item)

}

func riskClass(contribution float64) string {

switch {

case contribution < 0.30:

return "lower"

case contribution < 0.60:

return "moderate"

case contribution < 1.00:

return "elevated"

default:

return "severe"

}

}

func priority(item IssuerExposure) string {

switch {

case item.DisclosureAdequacy < 0.45:

return "improve_disclosure_quality"

case item.TransitionCredibility < 0.45:

return "assess_transition_plan_credibility"

case item.Uncertainty > 0.45:

return "reduce_uncertainty_and_model_risk"

case item.RealEconomyAlignment < 0.40:

return "strengthen_real_economy_alignment"

case boundaryPressureRatio(item) > 1.25:

return "reduce_boundary_pressure_exposure"

default:

return "maintain_monitoring_and_engagement"

}

}

func main() {

if len(os.Args) < 2 {

fmt.Println("usage: portfolio-boundary-risk issuer_exposures.csv")

os.Exit(1)

}

file, err := os.Open(os.Args[1])

if err != nil {

fmt.Println("error opening file:", err)

os.Exit(1)

}

defer file.Close()

reader := csv.NewReader(file)

rows, err := reader.ReadAll()

if err != nil {

fmt.Println("error reading CSV:", err)

os.Exit(1)

}

totalPortfolioRisk := 0.0

for i, row := range rows {

if i == 0 {

continue

}

item, err := parseIssuerExposure(row)

if err != nil {

fmt.Println("parse error:", err)

continue

}

score := riskScore(item)

contribution := portfolioContribution(item)

totalPortfolioRisk += contribution

fmt.Printf(

"issuer=%s domain=%s pressure_ratio=%.3f disclosure=%.3f transition=%.3f uncertainty=%.3f alignment=%.3f risk_score=%.3f contribution=%.3f class=%s priority=%s\n",

item.Issuer,

item.Domain,

boundaryPressureRatio(item),

item.DisclosureAdequacy,

item.TransitionCredibility,

item.Uncertainty,

item.RealEconomyAlignment,

score,

contribution,

riskClass(contribution),

priority(item),

)

}

fmt.Printf("portfolio_systemic_environmental_risk=%.3f\n", totalPortfolioRisk)

}

The Go workflow shows how disclosure and boundary-risk diagnostics can move from article-level explanation into operational systems. A lightweight service could support internal dashboards, portfolio monitoring, issuer screening, disclosure-quality scoring, due-diligence workflows, stewardship escalation, or regulator-facing analytical tools.

A production implementation should include schema validation, portfolio identifiers, issuer identifiers, instrument-level exposure, security-to-issuer mapping, source metadata, assurance status, threshold documentation, scenario versioning, transition-plan evidence, spatial nature-risk fields, uncertainty intervals, audit trails, and access controls. The goal is not a black-box risk score. It is a transparent scoring layer that makes environmental-risk assumptions visible enough for governance.

Engineering Extensions in the GitHub Repository

The accompanying GitHub repository extends the article workflow beyond Python, R, and Go into a broader engineering scaffold. The article body keeps Python and R visible because they are accessible tools for sustainability analytics, disclosure analysis, dashboard preparation, and reproducible reporting. Go provides a compact service layer. The repository, however, is structured for readers who want to translate finance, disclosure, and systemic environmental risk into more technical systems: auditable databases, scoring engines, APIs, embedded monitoring, scenario simulation, edge anomaly detection, and accelerator-aware environmental data pipelines.

The SQL scaffold is intended for issuer records, portfolio holdings, instrument mappings, boundary-domain metadata, disclosure-quality scores, transition-plan evidence, real-economy-alignment fields, source provenance, scoring runs, scenario assumptions, uncertainty fields, and audit trails. Rust can support high-integrity scoring engines or command-line tools where type safety and reproducibility matter. Go can support lightweight services and diagnostic APIs. C and C++ can support embedded threshold monitoring, local signal processing, or scenario simulation. TinyML can support low-power anomaly detection at the edge, while PYNQ-oriented scaffolding can support accelerated preprocessing of sensor or portfolio-risk streams.

This engineering layer matters because disclosure is only as reliable as the systems that produce it. If a disclosure architecture cannot track data lineage, version assumptions, document thresholds, expose uncertainty, or reproduce outputs, it may create the appearance of rigor without the substance of decision-grade analysis. Planetary-boundary finance therefore requires not only better reporting language, but better data infrastructure.

A mature implementation should also include documentation for assurance status, reporting boundaries, financed exposure, supply-chain coverage, nature-risk spatial joins, transition-plan dependencies, model limitations, and review workflows. Disclosure systems should be designed not only to publish reports, but to support capital allocation, supervision, stewardship, and public accountability.

GitHub Repository

Complete Code Repository

The full code distribution for this article, including Python, R, and Go workflows plus extended engineering scaffolding for SQL, Rust, C, C++, TinyML, and PYNQ-oriented systemic environmental risk and disclosure diagnostics, is available on GitHub.

Common Misunderstandings

A common misunderstanding is that disclosure alone solves environmental risk. It does not. Disclosure is an information tool, not a substitute for transition, governance, regulation, capital reallocation, or changes in business models. Better disclosure can make risk more visible, but visibility does not guarantee action.

Another misunderstanding is that climate disclosure is enough. Climate is central, but nature loss, water disruption, pollution, land-system change, and novel entities also generate financially relevant and systemic risks. Climate-only frameworks are not sufficient for a fuller treatment of environmental dependence and impact.

A third misunderstanding is that if a risk is not yet clearly material to one firm, it is not strategically significant. In planetary-boundary terms, that is too narrow. Systemic environmental risk can be growing even when entity-level materiality still looks partial or delayed. That gap is one of the main reasons current disclosure practice remains under pressure to evolve.

A further misunderstanding is that more disclosure automatically means better capital allocation. This is not guaranteed. Information can still be ignored, discounted, short-termized, or subordinated to existing incentives. Disclosure matters because it creates the possibility of better decisions, but that possibility depends on governance, regulation, market norms, assurance, and the willingness of financial actors to act on what is being revealed.

Another misunderstanding is that scenario analysis produces predictions. It does not. Scenarios are structured explorations of possible futures under explicit assumptions. Their value depends on how clearly those assumptions are disclosed and whether the results change governance and capital-allocation decisions.

Finally, systemic environmental risk should not be confused with ordinary portfolio volatility. Portfolio volatility can sometimes be diversified. A destabilized Earth system cannot. Finance cannot diversify away from the material conditions of the economy itself.

Related Articles

- What Are Planetary Boundaries?

- The Origins of the Planetary Boundaries Framework

- Safe Operating Space and the Logic of Thresholds

- How Planetary Boundaries Are Measured

- Planetary Boundaries and Earth System Resilience

- Tipping Points, Feedback Loops, and Cascading Ecological Change

- Novel Entities and the Problem of Synthetic Overload

- Business Strategy Within Planetary Boundaries

- Earth System Governance in an Age of Limits

- Planetary Boundaries, Justice, and Global Inequality

- Planetary Boundaries and Doughnut Economics

- Critiques of the Planetary Boundaries Framework

- The Future of Planetary Stewardship

Further Reading

- IFRS Foundation (n.d.) IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information. Available at: https://www.ifrs.org/issued-standards/ifrs-sustainability-standards-navigator/ifrs-s1-general-requirements/.

- IFRS Foundation (n.d.) IFRS S2 Climate-related Disclosures. Available at: https://www.ifrs.org/issued-standards/ifrs-sustainability-standards-navigator/ifrs-s2-climate-related-disclosures/.

- IFRS Foundation (2025) Disclosing Information About an Entity’s Climate-related Transition, Including Information About Transition Plans, in Accordance with IFRS S2. Available at: https://www.ifrs.org/news-and-events/news/2025/06/ifrs-publishes-guidance-disclosures-transition-plans/.

- Network for Greening the Financial System (2024) NGFS Climate Scenarios for Central Banks and Supervisors: Phase V. Available at: https://www.ngfs.net/en/publications-and-statistics/publications/ngfs-climate-scenarios-central-banks-and-supervisors-phase-v.

- Task Force on Climate-related Financial Disclosures (2017) Final Report: Recommendations of the Task Force on Climate-related Financial Disclosures. Available at: https://assets.bbhub.io/company/sites/60/2021/10/FINAL-2017-TCFD-Report.pdf.

- Taskforce on Nature-related Financial Disclosures (2023) Recommendations of the Taskforce on Nature-related Financial Disclosures. Available at: https://tnfd.global/recommendations/.

- Taskforce on Nature-related Financial Disclosures (2023) Executive Summary of the TNFD Recommendations. Available at: https://tnfd.global/wp-content/uploads/2023/09/Executive_summary_of_the_TNFD_recommendations.pdf.

- Crona, B., Wassénius, E., Parlato, G. and Kashyap, S. (2024) Doing Business Within Planetary Boundaries. Stockholm: Stockholm Resilience Centre and Beijer Institute of Ecological Economics. Available at: https://www.stockholmresilience.org/research/synthesis-reports/doing-business-within-planetary-boundaries.html.

- Richardson, K. et al. (2023) ‘Earth beyond six of nine planetary boundaries’, Science Advances, 9(37), eadh2458. Available at: https://www.science.org/doi/10.1126/sciadv.adh2458.

- Rockström, J. et al. (2009) ‘A safe operating space for humanity’, Nature, 461, pp. 472–475. Available at: https://www.nature.com/articles/461472a.