Last Updated May 9, 2026

Monetary policy, central banking, and financial conditions are central to economic analysis because they shape the terms under which money, credit, liquidity, and macroeconomic adjustment are organized across time. Interest rates influence borrowing, saving, asset valuation, and debt service. Central banks help govern settlement, reserves, emergency liquidity, and the broader monetary architecture on which modern finance depends. Financial conditions translate these institutional settings into the lived structure of credit availability, refinancing capacity, market confidence, and balance-sheet strain. Together, they influence not only inflation and output, but also employment, investment, asset prices, public debt management, and the resilience of the wider economic order.

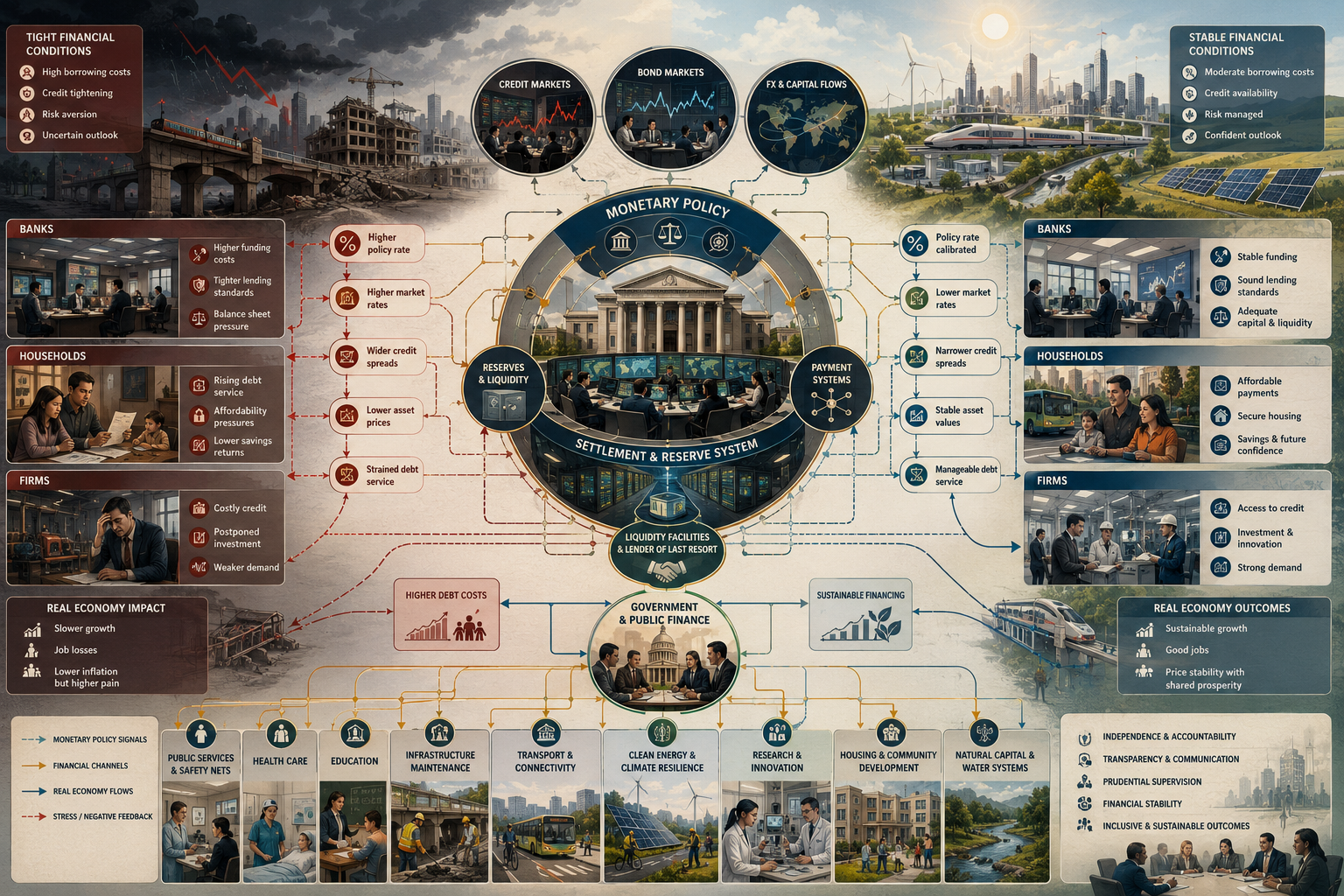

Monetary policy is often presented in simplified terms, as if central banks merely raise rates to slow inflation or lower rates to support growth. In reality, monetary governance is more complex. Central banks operate within financial systems shaped by banking structures, debt hierarchies, collateral practices, payment infrastructures, and public expectations. A change in policy rates affects these systems unevenly. It may cool some sectors quickly, barely reach others, and intensify balance-sheet pressure where leverage is already high. The monetary transmission mechanism is therefore not mechanical. It is institutional, distributive, and historically contingent.

These questions matter because financial conditions can tighten or loosen far beyond the formal policy rate alone. Credit spreads, asset prices, bank funding costs, exchange rates, liquidity stress, and risk appetite all influence whether households can refinance, firms can invest, and governments can fund essential commitments on sustainable terms. Monetary policy thus works partly through expectations and pricing, but also through the broader architecture of financial intermediation and systemic confidence.

Main Library

Publications

Article Map

Economic Systems

Related Topic

Sustainable Development

Related Topic

Institutions & Governance

Related Topic

Risk & Resilience

Within a sustainable systems framework, monetary policy, central banking, and financial conditions must be evaluated not only in relation to inflation control or cyclical management, but also in relation to resilience, investment quality, public capacity, and the distribution of adjustment burden. A society may stabilize prices while damaging housing affordability, suppressing productive investment, increasing debt stress, and deepening dependence on fragile financial structures. The serious study of monetary governance therefore asks not only whether policy is tight or loose, but what financial conditions are being produced, who absorbs the resulting strain, and whether the monetary order supports durable collective life under uncertainty.

Why This Topic Matters

Monetary policy, central banking, and financial conditions matter because modern economies are organized through money-denominated promises extending across time. Households borrow for housing and education. Firms finance inventories, payroll, and capital projects. Governments issue debt to sustain public goods, infrastructure, and crisis response. Banks and markets constantly refinance, price, hedge, and roll over claims. The terms under which these activities occur are shaped profoundly by monetary governance.

This matters analytically because monetary systems are not neutral backdrops. A change in rates can alter consumption, business investment, exchange rates, asset valuations, and public borrowing costs. A shift in liquidity conditions can determine whether ordinary financial stress remains manageable or becomes systemic. Central banks are therefore deeply implicated in how the macroeconomy absorbs disturbance and distributes adjustment.

These issues also matter politically. Tight monetary conditions may restrain inflation while increasing unemployment, debt-service burdens, and financial strain. Loose monetary conditions may support activity while encouraging leverage, asset inflation, and speculative excess. The central bank’s role is therefore never wholly technical. It affects who can refinance easily, who must absorb higher cost, which sectors cool first, and how much fragility is tolerated in pursuit of nominal stability.

It also matters because financial conditions often shape real outcomes before they show up clearly in conventional macroeconomic statistics. A society can appear stable in output terms while credit quietly dries up, household debt burdens intensify, and investment plans are deferred. Monetary analysis therefore helps reveal how future slowdown is often incubated in present financial conditions.

For this reason, the study of monetary governance belongs at the intersection of macroeconomics, banking, finance, and political economy. It shows how a modern society manages time, confidence, and coordinated adjustment through institutions that stand near the center of the economic order.

It is also one of the clearest places where abstract macroeconomic categories become materially real. A rate decision becomes a mortgage payment, a bond repricing, a delayed factory expansion, a weaker labor market, or a more expensive public refinancing cycle. Monetary policy is therefore one of the principal ways institutional decisions are transmitted into everyday economic life.

What Monetary Policy Is

Monetary policy refers to the set of tools through which central banks influence interest rates, liquidity conditions, reserve availability, and broader monetary and financial circumstances in pursuit of macroeconomic objectives. These objectives usually include price stability, financial stability, and in some systems a degree of responsibility for employment or output stabilization.

This matters because monetary policy is often reduced to a single number: the policy rate. But the rate is only one part of a wider framework. Central banks also manage reserves, influence short-term money markets, provide emergency liquidity, communicate future guidance, supervise parts of the banking system, and sometimes purchase assets outright in exceptional conditions. Monetary policy is therefore better understood as governance of a monetary-financial environment rather than as one dial turned up or down.

Monetary policy is also relational. It operates through banks, bond markets, exchange rates, collateral practices, and expectations. It does not move directly from central-bank announcement to household decision without institutional mediation. This means that the effect of monetary policy depends on the structure of the financial system and the balance-sheet condition of borrowers, lenders, and governments.

A serious account must therefore treat monetary policy as an institutional transmission process, not as a purely abstract control mechanism. The key question is not only what the central bank intends, but how policy settings travel through the real financial structure of the economy.

This broader view is essential because economies differ in credit structure, bank dependence, capital-market depth, housing finance, and public debt design. The same policy stance can therefore produce very different real effects across countries, periods, and sectors.

Monetary policy is therefore never a universal lever applied to a frictionless field. It is a structured intervention into a historically formed financial system whose channels, delays, asymmetries, and vulnerabilities determine what the policy can actually accomplish.

At its deepest level, monetary policy governs the price and availability of time. It shapes how expensive it is to bring future income, production, housing, public investment, or speculative gain into the present. This is why monetary systems are always systems of power as well as systems of price coordination.

What Central Banks Do

Central banks sit at the core of the monetary hierarchy because they issue reserves, support settlement among banks, influence short-term interest rates, and act as lenders of last resort under certain conditions. In many systems they also supervise banks, monitor systemic stability, and serve as key public institutions for crisis containment. They are therefore not merely analysts of the economy. They are active governors of the monetary infrastructure itself.

This matters because central banks help make money credible. Payment systems depend on settlement finality. Banks depend on reserve access and emergency liquidity. Government debt markets often depend on expectations about central-bank stability. In stress, the central bank can become the institution that determines whether uncertainty remains localized or becomes generalized panic.

Central banks also matter because they connect public authority to financial markets. They stand at the boundary where state legitimacy, banking stability, and market pricing meet. This makes them powerful, but it also places them under intense distributive and political pressure. A central bank that raises rates sharply changes more than inflation expectations; it changes refinancing conditions, employment risks, asset valuations, and the fiscal environment in which elected governments operate.

A research-grade account therefore treats central banks as institutional actors within political economy, not as detached technicians acting outside history or conflict. Their mandates, tools, and interventions reflect choices about what kinds of stability matter most and who is expected to bear adjustment cost.

Central banks therefore cannot be understood merely by their statutes. They must be understood through what they actually stabilize, what they permit to fail, and what they implicitly prioritize when tradeoffs become unavoidable.

They also embody a deeper constitutional question about capitalism itself: who ultimately guarantees the continuity of money and settlement when private financial institutions are unable to do so on their own. Central banking is, in this sense, a public answer to the instability of privately mediated credit systems.

This public answer is never neutral in practice. The design of emergency lending, collateral eligibility, reserve access, bank supervision, and crisis facilities determines which institutions stand closest to monetary safety and which remain exposed when stress arrives.

Policy Rates and the Price of Credit

The policy rate is the central bank’s key reference rate for short-term monetary conditions. By influencing interbank funding and the general structure of money-market pricing, it helps shape borrowing costs across the wider economy. Mortgage rates, business loans, bond yields, and the discount rates used in valuation all tend to be affected, though never perfectly or uniformly.

This matters because the price of credit influences the timing of expenditure. Lower rates may encourage firms to invest and households to borrow, while higher rates can slow these activities by increasing financing cost and debt-service burden. Policy rates therefore affect not only present spending, but the willingness to commit resources to long-duration projects whose returns arrive in the future.

But the relationship is never one-to-one. Lending rates include risk premia, bank margins, collateral conditions, and market expectations. A rate cut in a crisis may not translate into easier credit if banks are impaired or risk-averse. A rate hike may hit highly indebted households quickly while leaving cash-rich firms relatively insulated. Monetary policy therefore changes the price of credit through a structure already marked by asymmetry.

For that reason, analysis of rates must always include financial context. The same policy move can produce very different real outcomes depending on leverage, confidence, and the composition of debt in the system.

The deeper point is that interest rates are not simply prices in a narrow market sense. They are social prices for time, liquidity, and access to credible future claims under institutional conditions set partly by public authority.

They also act as intertemporal signals. A low-rate environment encourages present commitment relative to future uncertainty; a high-rate environment disciplines present borrowing by making future repayment more burdensome. Monetary policy therefore helps structure the tempo of the economy as well as its price conditions.

This temporal role is especially important for long-horizon systems. Infrastructure, housing, energy transition, public health readiness, and climate adaptation all depend on financing costs across time. When the price of time rises sharply, some futures become harder to build even if their social need becomes more urgent.

Financial Conditions Beyond the Policy Rate

Financial conditions refer to the broader environment through which monetary policy is transmitted and through which financing becomes easier or harder across the economy. They include policy rates, but also credit spreads, equity prices, bond yields, exchange rates, bank lending standards, leverage conditions, risk appetite, collateral quality, and market liquidity.

This matters because the official policy stance may not tell the full story. Financial conditions can loosen even when the policy rate is unchanged if risk premiums compress, asset prices rise, and banks lend aggressively. They can tighten sharply even without a rate increase if markets become fearful, bank balance sheets weaken, or liquidity becomes scarce. Monetary governance must therefore be read through a wider financial lens.

Financial conditions also matter because they are often the practical reality faced by firms and households. A business seeking credit does not borrow at the overnight policy rate. A household refinancing a mortgage faces the full structure of lending terms, underwriting standards, and market conditions. What matters in lived economic terms is the effective cost and availability of finance, not the central-bank instrument alone.

A research-grade analysis therefore treats financial conditions as the macro-financial translation layer between central-bank intent and the actual behavior of banks, markets, firms, and households.

This broader perspective is especially important in periods of stress, when formal monetary stance and actual financing conditions can diverge sharply. The economy may then be much tighter or looser than headline policy numbers suggest.

Financial conditions also help explain why central banks pay close attention to signals outside the consumer price index. Markets can reprice long before output or employment data reveal the cumulative effect. In this sense, financial conditions are both transmission channel and early warning system.

They are also distributional. A broad easing of financial conditions may first lift asset prices and refinancing opportunities for those already close to financial markets. A tightening may first strike marginal borrowers, small firms, local governments, and households exposed to variable-rate debt. Financial conditions are therefore never a purely aggregate condition.

Transmission Mechanisms: How Policy Reaches the Real Economy

Monetary policy affects the real economy through several transmission channels. Changes in rates alter borrowing costs for households and firms. Asset-price movements change wealth and collateral values. Exchange-rate shifts affect import prices and external competitiveness. Bank-lending conditions influence the availability of credit. Expectations about future policy shape current decisions on investment, wages, and pricing.

This matters because each channel works differently and at different speeds. Housing markets may respond quickly in mortgage-intensive economies. Business investment may respond more slowly if uncertainty remains high. Exchange-rate effects may matter more in open economies. Bank-lending effects may dominate in systems where firms depend heavily on banks rather than capital markets. Monetary transmission is therefore heterogeneous by design.

Transmission also depends on balance sheets. Highly indebted households may cut spending sharply when rates rise. Firms with long-term fixed-rate financing may feel less immediate pressure. Governments with short-duration debt may face faster fiscal strain than those with longer-maturity structures. The macroeconomic meaning of policy thus depends on who is exposed and how.

A serious treatment of monetary policy must therefore avoid abstract uniformity. Policy reaches the economy through institutions, contracts, and balance sheets that distribute its effects unevenly across sectors and social groups.

This is one reason central banking is inseparable from financial structure. The same policy philosophy can yield different outcomes depending on whether the economy is driven by fixed-rate mortgages, floating-rate debt, bank credit, bond markets, or external borrowing.

Transmission also has a temporal problem: some effects are immediate, others delayed, and some become visible only after the initial policy cycle appears to have done its work. Monetary governance therefore operates under uncertainty not only about magnitude, but about timing.

Because of these lags and asymmetries, monetary policy can overcorrect. A central bank may keep conditions tight while the cumulative effects are still moving through housing, investment, banking, and employment. A serious systems view therefore treats transmission as a delayed chain of institutional reactions, not an instant command.

Liquidity, Reserves, and the Infrastructure of Settlement

Modern monetary systems depend on reserves and settlement infrastructure. Banks clear obligations using reserve balances at the central bank, and the smooth functioning of payments depends on confidence that settlement will occur reliably. Liquidity therefore is not merely about convenience. It is part of the underlying machinery that makes modern exchange possible.

This matters because crises often begin or intensify when liquidity becomes scarce or unevenly distributed. Institutions that appear solvent can still fail if they cannot meet immediate obligations. Central banks manage this risk by influencing reserve conditions in normal times and, when needed, by supplying emergency liquidity so that settlement breakdown does not turn into full systemic panic.

Liquidity also matters because it shapes how money-like private claims are valued. Bank deposits function as money partly because central-bank-backed settlement makes them credible. Wholesale markets depend on confidence that collateral can be financed and payment flows will not seize up. Monetary order is therefore deeply infrastructural.

For this reason, the central bank must be understood not only as a rate setter, but as a governor of liquidity architecture. Its role in preserving settlement capacity is one of the hidden foundations of macroeconomic continuity.

In ordinary times this infrastructure is easy to overlook precisely because it works. But when it fails or even appears vulnerable, the economy quickly discovers how much of everyday stability depends on institutions most people rarely see directly.

Reserves and settlement are therefore not merely technical plumbing. They are part of the public scaffolding that allows private finance to appear seamless in normal conditions. Once that scaffolding becomes strained, the distinction between technical and political monetary questions narrows rapidly.

Liquidity also reveals hierarchy. Institutions with direct or indirect access to central-bank liquidity are positioned differently from those outside the core system. Crisis exposes this hierarchy by showing whose liabilities are treated as money-like and whose are allowed to break under stress.

Inflation Targeting, Expectations, and Credibility

Many central banks operate with explicit or implicit inflation targets, using monetary policy to keep inflation close to a stated objective over time. This framework is built partly on the idea that stable and credible expectations help prevent temporary shocks from becoming persistent inflationary processes.

This matters because expectations can influence pricing and wage behavior before actual inflation fully spreads. If firms and households believe the central bank will eventually restore price stability, they may be less likely to build extreme inflation assumptions into contracts and decisions. Credibility, in this sense, is a coordinating device.

But credibility has limits. Expectations are not formed only by central-bank communication. They are shaped by lived price movements, labor-market conditions, energy costs, political trust, and the perceived realism of policy. A central bank may be credible in ordinary demand cycles yet face harder challenges when inflation is being driven by supply shocks, geopolitical disruption, or repeated energy strain. In such cases, restoring credibility may require more than rhetorical firmness.

A research-grade treatment therefore sees inflation targeting as one institutional framework among others, not as a complete theory of price stability. Its success depends partly on the material and political context in which it operates.

Credibility is thus not simply asserted by technocratic confidence. It is earned when institutions can plausibly guide the economy back toward stability without producing adjustment costs so destructive that the public begins doubting the legitimacy of the entire strategy.

This means that credibility has a social basis. A monetary regime remains credible not only because markets believe it can discipline prices, but because the broader polity continues to regard its methods as tolerable, intelligible, and not fundamentally one-sided in how they allocate pain.

Credibility also depends on coordination with the rest of the economic system. When inflation arises from energy, supply chains, housing, market power, or public underinvestment, monetary credibility is strengthened when other institutions address those sources directly rather than leaving the central bank to suppress symptoms through demand contraction alone.

Employment, Output, and the Dual Burden of Adjustment

Monetary tightening is often justified as necessary to reduce inflationary pressure. Yet higher rates also weaken credit demand, slow investment, reduce asset values, and can raise unemployment. This makes monetary governance a problem of dual burden: price instability is costly, but so is disinflation achieved through large-scale output loss and labor-market damage.

This matters because adjustment is not socially neutral. Labor markets often absorb monetary tightening more visibly and more rapidly than profit margins or wealth concentration do. Unemployment, weaker bargaining power, and deferred hiring become part of the path through which inflation is brought down. This is one reason monetary policy cannot be understood as merely technical optimization.

Output also matters because prolonged weakness damages future capacity. If rates remain high long enough to suppress productive investment, maintenance, or skill formation, monetary stabilization can carry longer-run developmental cost. The economy may emerge with lower inflation but also with weaker infrastructure, reduced housing supply, or damaged public balance sheets.

A serious framework therefore asks not only whether inflation is being reduced, but how, through whose adjustment, and with what consequences for future capacity and social legitimacy.

The central issue is not whether tradeoffs exist, but whether institutions confront them honestly. Monetary policy that treats labor-market pain as an incidental byproduct rather than a core part of its transmission risks obscuring the full political economy of stabilization.

This is especially important when inflation is not primarily wage-driven. In such cases, labor-market sacrifice may be asked to do disproportionate disinflationary work for a problem rooted partly in supply conditions, energy shocks, or market structure elsewhere in the system.

Employment also has social memory. Lost work, delayed hiring, canceled apprenticeships, and weakened bargaining power can outlast the immediate policy cycle. A monetary regime that repeatedly stabilizes prices by weakening labor may generate long-term social costs that do not appear in short-run inflation metrics.

Asset Prices, Wealth Effects, and Financial Valuation

Monetary policy influences asset prices by changing discount rates, financing conditions, and investor expectations. Lower rates tend to support higher valuations for equities, bonds, housing, and other assets by making future income streams more valuable in present terms and by reducing the cost of leverage. Higher rates tend to reverse some of these effects.

This matters because asset prices affect both spending and inequality. Rising asset values can support wealth effects, making some households and firms feel richer and more willing to spend or invest. But asset inflation also tends to benefit those who already own financial and real assets, while worsening affordability for those trying to enter housing or capital markets later.

Valuation effects also matter for financial stability. When long periods of low rates encourage leverage and risk-taking, the eventual adjustment to tighter conditions can be disorderly. Bonds lose value, growth stocks reprice, real estate cools, and weak balance sheets come under pressure. The monetary cycle is therefore closely linked to valuation regimes.

A research-grade treatment of monetary policy must therefore include asset-price channels as integral, not peripheral. Central banking shapes not only inflation and employment, but the structure of wealth, leverage, and financial sensitivity across the whole economy.

This also means that monetary stabilization can create intertemporal tension: policies that support the economy in the short run may contribute to financial exuberance, while policies that restrain excess later may do so by reversing gains that had already become embedded in household plans and institutional balance sheets.

Asset-price channels therefore show how monetary policy can widen or narrow social distance. A regime that repeatedly protects financial valuations while allowing labor insecurity or housing exclusion to intensify may preserve nominal calm while quietly undermining broader legitimacy.

The valuation channel also demonstrates why “financial stability” cannot be added to monetary policy as an afterthought. A rate environment that produces fragile valuations, leverage dependence, or duration mismatch can store instability for later even when inflation and employment appear stable in the present.

Housing, Debt Service, and Household Exposure

Housing is one of the most important channels through which monetary policy reaches everyday life. Mortgage rates influence monthly payments, housing affordability, refinancing decisions, and construction activity. Where households carry variable-rate debt or must refinance frequently, policy changes can alter disposable income quickly and sharply.

This matters because housing is both shelter and a major balance-sheet asset. Rate increases can slow speculative appreciation and cool excess demand, but they can also raise debt-service burdens for existing borrowers and lock prospective buyers out of the market. Lower rates can support housing access for some while bidding prices upward and intensifying affordability problems in supply-constrained markets.

Household exposure also matters because debt burdens are not distributed evenly. Renters, owners with fixed-rate mortgages, owners with floating-rate debt, landlords, developers, and first-time buyers all experience monetary change differently. The housing channel is therefore not a single effect but a field of differentiated impacts.

For this reason, housing reveals the social depth of monetary policy. Central-bank decisions are not confined to bond traders and banks; they enter kitchens, rent burdens, family budgets, and long-horizon life planning.

Housing also demonstrates why monetary policy cannot compensate fully for structural supply problems. High rates may cool prices, but they may also reduce construction. Low rates may support finance, but they may worsen speculative demand if supply is inelastic. Monetary policy therefore interacts with housing systems it does not fully control.

This makes housing one of the clearest examples of how financial conditions meet institutional structure. Zoning, public housing policy, construction costs, land constraints, and credit design all determine whether monetary easing becomes broader access or merely higher prices.

A sustainable monetary framework therefore cannot ignore housing. If rate policy repeatedly destabilizes affordability, construction, and household debt burdens, then monetary governance is shaping the social foundations of economic life, not merely the pace of aggregate demand.

Banking Stability, Lender of Last Resort, and Crisis Containment

Central banks serve as lenders of last resort because banking systems are structurally vulnerable to liquidity stress. Banks promise deposit access while holding illiquid longer-duration assets. When confidence weakens, even solvent institutions can face destabilizing runs or wholesale funding freezes. The central bank’s ability to supply liquidity in these moments is one of the defining features of modern monetary order.

This matters because financial crises cannot be prevented or contained by rates alone. In acute stress, liquidity backstops, collateral frameworks, emergency lending facilities, and clear public communication become crucial. The central bank then acts not merely as a macroeconomic manager, but as a system stabilizer.

Lender-of-last-resort action also raises difficult political questions. Emergency support can prevent catastrophic spillover, but it may also reinforce expectations that sufficiently important institutions will be protected in future crises. This creates tension between systemic rescue and moral hazard.

A serious account therefore treats crisis containment as both necessary and contested. Central banks protect the wider economy when they stabilize finance, but in doing so they also reveal that private financial systems depend deeply on public backstops when stress becomes severe.

This is one reason monetary authority and regulatory authority are never fully separable. Decisions about which collateral is accepted, which institutions are supported, and which liabilities are protected all shape the practical structure of safety in the financial system.

Crisis containment also reveals the hierarchy embedded in finance. Some institutions sit close enough to core payment, settlement, and funding systems that their instability rapidly becomes a public matter. Central-bank rescue is therefore never just about generosity; it is about the recognition that some forms of private fragility have already become systemic.

The lender-of-last-resort role also creates a design challenge: emergency liquidity should protect the system without permanently subsidizing fragile business models. That requires strong supervision, resolution capacity, capital standards, liquidity rules, and accountability before the crisis, not merely improvisation during it.

Exchange Rates, Capital Flows, and Open-Economy Constraints

Monetary policy operates differently in open economies because exchange rates, foreign borrowing, and capital flows alter the transmission process. Higher rates may support the domestic currency and reduce imported inflation, but they may also attract volatile capital inflows and strain domestic borrowers. Lower rates may support local demand, but they can weaken the currency and increase import costs, especially in energy-dependent economies.

This matters because monetary sovereignty is uneven. Countries with reserve currencies, deep domestic financial markets, and lower dependence on foreign-currency borrowing have more room to maneuver than countries exposed to external funding stress. Financial conditions in large economies can also spill across borders, shaping borrowing costs and exchange-rate pressures elsewhere.

Open-economy constraints are especially important where food, energy, and capital goods are heavily imported. Exchange-rate depreciation can transmit external inflation quickly into domestic prices, while abrupt capital outflows can destabilize funding and public finance. Monetary policy must then balance domestic stabilization against external vulnerability.

A research-grade treatment therefore situates central banking within global monetary hierarchy rather than treating each country as an isolated macroeconomic unit. Financial conditions are international as well as domestic.

This global dimension also means that central banks may import difficult tradeoffs from abroad. Tightening in a dominant-currency economy can harden conditions elsewhere even when domestic circumstances would otherwise call for more supportive policy.

Open-economy monetary governance is therefore also geopolitical. Currency status, reserve accumulation, trade invoicing, and external debt structure all shape what central banks can credibly do without triggering larger disturbances through the international system.

For sustainable systems, this matters because countries exposed to external monetary pressure may struggle to finance adaptation, infrastructure, food security, or energy transition on tolerable terms. Monetary hierarchy can therefore become an obstacle to resilience, not merely a technical feature of exchange-rate management.

Monetary Policy, Fiscal Interaction, and Public Debt

Monetary and fiscal policy are often discussed as separate domains, but in practice they are deeply intertwined. Higher interest rates raise the cost of servicing public debt, alter the fiscal space available for investment and stabilization, and change the political environment in which governments make budgetary choices. Conversely, large fiscal expansions can affect aggregate demand, bond issuance, and expectations about future rates and inflation.

This matters because macroeconomic governance is not modular. A central bank tightening aggressively while governments are trying to protect households, finance infrastructure, or sustain recovery creates a combined policy environment that may be internally tense. In some cases the policies complement one another; in others they partially offset or complicate each other.

Public debt structure also matters. Governments with long-duration debt may absorb higher rates more slowly than those rolling over debt quickly. Monetary tightening may therefore have delayed but significant fiscal consequences, especially where public investment depends on continuous borrowing access.

A serious account of monetary governance must therefore include the public balance sheet. Central banking affects not only private credit and inflation, but the financial conditions under which democratic governments can fund collective commitments.

The relationship is especially important in periods of structural transition, when societies may need large-scale public investment at exactly the moment higher rates make borrowing more expensive. Monetary and fiscal institutions must then negotiate not only stabilization, but the timing and affordability of the future itself.

This interaction is one of the central reasons monetary policy cannot be evaluated purely in isolation. A rate path that appears reasonable in inflation terms may still have profound consequences for the viability of infrastructure programs, social protection, and long-horizon public adaptation.

A sustainable economic framework therefore asks whether monetary and fiscal institutions are aligned around durable public capacity or whether they repeatedly undermine one another: fiscal policy trying to build resilience while monetary conditions make resilience more expensive, or monetary policy trying to stabilize prices while fiscal policy fails to address the supply-side weaknesses behind inflation.

Distributional Effects of Monetary Governance

Monetary policy has distributional effects because households and firms occupy different positions in relation to debt, assets, wages, and credit access. Lower rates often benefit asset holders, leveraged investors, borrowers able to refinance, and sectors sensitive to valuation. Higher rates may benefit savers with liquid balances while imposing greater burden on indebted households, marginal borrowers, and rate-sensitive employers.

This matters because monetary policy is sometimes described as distributionally neutral, as if it only affects aggregates. In reality, it works through channels that are socially structured from the start. Some actors sit close to central-bank-supported liquidity; others face finance through costly retail channels. Some hold appreciating assets; others rely mainly on wages. The same policy move can therefore widen or narrow inequality depending on context.

Distribution also matters politically. If inflation control is achieved disproportionately through labor-market weakness or household debt stress while wealthier groups are protected through stronger asset positions, legitimacy may erode. Conversely, prolonged monetary accommodation that fuels asset inflation can deepen wealth concentration and housing exclusion even if aggregate demand remains supported.

A research-grade treatment therefore places distribution inside the core of monetary analysis. Central banking governs not only the level of activity, but the pattern through which burden and opportunity are distributed across the economy.

This does not mean central banks can solve every distributive problem. It does mean that their actions are never outside distributional reality, even when their mandates are written in technocratic language.

Distributional analysis also makes visible a deeper tension: a monetary regime can be formally successful on inflation or market-stability terms while contributing to longer-run patterns of exclusion, indebted dependence, and unequal asset access that weaken social resilience overall.

The distributional lens therefore changes the question from “Did policy work?” to “For whom did policy work, through what channel, and at what social cost?” That is a more honest way to evaluate monetary governance in a stratified economy.

Historical Lessons from Monetary Regimes and Central Bank Evolution

Historically, central banks and monetary regimes have changed substantially as financial systems, political orders, and macroeconomic ideas evolved. The role of central banks in gold-standard systems differed from their role in welfare-capitalist mixed economies, in inflation-targeting eras, and in periods shaped by quantitative easing, global capital mobility, and repeated financial rescue.

This matters because monetary governance is not timeless. What counts as sound central banking in one historical setting may be insufficient in another. Regimes organized around gold convertibility, fixed exchange rates, strict anti-inflationary discipline, or active crisis management each embody different assumptions about the balance between markets, public authority, employment, finance, and external constraint.

Historical experience also reveals that central-bank roles tend to expand in crisis. Institutions initially framed narrowly around payments, convertibility, or reserve management often become broader stabilizers when financial breakdown threatens the wider economy. The central bank’s real function is therefore often discovered most clearly under extreme pressure rather than in tranquil doctrine.

A research-grade approach treats central banking as historically contingent institution-building. It asks not only what central banks are formally mandated to do, but how changing monetary regimes reveal shifting ideas about sovereignty, stability, and public responsibility in capitalist economies.

History also teaches that monetary arrangements which seem neutral or natural in one era often later appear highly political. Central-banking orthodoxy changes not only because theory changes, but because crises reveal what existing regimes had been unable or unwilling to stabilize.

Historical perspective is therefore indispensable for resisting presentism. The current monetary regime is not the final form of central banking, but one institutional settlement among others, likely to be revised again when new crises reveal its limits, blind spots, and distributional assumptions.

The deeper historical lesson is that monetary systems are always social systems. They organize trust, hierarchy, discipline, rescue, and time. Their technical details matter precisely because they carry such large social consequences.

Monetary Policy, Central Banking, and Sustainable Systems

Within sustainable systems, monetary policy must be judged not only by whether it stabilizes prices, but by whether the financial conditions it creates support resilient, productive, and socially viable forms of investment. A monetary order that repeatedly fuels asset inflation, housing exclusion, speculative leverage, and underinvestment in infrastructure may be formally stable while materially unsustainable.

This matters because long-horizon transitions such as energy transformation, water resilience, adaptation infrastructure, public health readiness, and digital security all depend on financing conditions. If rates, spreads, and risk structures make long-term public or productive investment chronically difficult while leaving short-horizon speculation comparatively attractive, monetary governance may undermine the very resilience the broader economy requires.

Sustainable systems therefore require more than periodic crisis rescue. They require monetary and financial conditions compatible with maintenance, adaptation, and broad-based capability-building. This may include lower volatility in core funding conditions, stronger coordination with fiscal institutions, and prudential rules that prevent fragility from crowding out patient investment.

In this sense, central banking becomes part of systems design. The question is whether monetary governance helps societies navigate uncertainty while preserving capacity, or whether it repeatedly shifts adjustment burden onto households, public budgets, and undermaintained infrastructures while stabilizing only the narrowest definition of macroeconomic order.

This also means that the monetary question is inseparable from the temporal question. Financial conditions today shape what becomes buildable, maintainable, and governable tomorrow. The central bank therefore participates, indirectly but powerfully, in deciding what kinds of futures remain economically credible.

A sustainable monetary framework would therefore not only aim at short-run nominal coherence, but also at a financial environment that does not systematically penalize repair, prevention, and long-horizon resilience relative to speculation, leverage, and short-duration gain.

Such a framework would also recognize that price stability and resilience are not enemies. Energy security, housing supply, infrastructure maintenance, and climate adaptation can reduce future inflation vulnerability. Monetary governance should therefore be coordinated with the investments and institutions that make future price stability less dependent on repeated demand suppression.

How Monetary Systems Should Be Judged

Monetary systems should not be judged only by the level of the policy rate, the inflation target, or the immediate response of asset markets. A broader economic systems framework asks how monetary governance shapes credit access, debt-service burdens, investment horizons, liquidity resilience, public finance, distribution, and future capacity.

| Dimension | Narrow Question | Systems Question |

|---|---|---|

| Policy Rate | Did the central bank raise or lower rates? | How did the rate change affect real borrowing costs, debt service, investment, housing, and public finance? |

| Financial Conditions | Is policy tight or loose? | What are credit spreads, lending standards, asset prices, exchange rates, liquidity, and risk appetite actually doing? |

| Transmission | Will policy affect demand? | Through which institutions, balance sheets, contracts, and sectors does policy reach the real economy? |

| Inflation | Is inflation returning to target? | Is disinflation achieved through supply repair, expectations stability, labor-market pain, or household debt stress? |

| Employment | Is unemployment rising or falling? | Who bears labor-market adjustment, and what long-run capacity is lost through suppressed hiring or investment? |

| Financial Stability | Are banks solvent? | Are liquidity, collateral, duration risk, and funding structures resilient under stress? |

| Public Debt | Are rates affecting government borrowing? | Do monetary conditions preserve or undermine fiscal capacity for infrastructure, services, and adaptation? |

| Sustainability | Is nominal stability preserved? | Do monetary and financial conditions support long-horizon resilience, productive investment, and equitable adjustment? |

This framework prevents a common mistake: treating monetary policy as a neutral technical adjustment to aggregate variables. Monetary governance always operates through a structured economy of assets, debts, institutions, households, firms, banks, and states. Its effects are therefore practical, distributed, and historically specific.

The central question is not simply whether the central bank is credible or whether the policy rate is appropriate. The deeper question is whether monetary institutions help the wider economy remain stable, investable, fair enough to command legitimacy, and resilient enough to face long-run social and ecological uncertainty.

Mathematical Lens

Mathematics can clarify monetary policy, central banking, and financial conditions by making real rates, debt-service burdens, reaction functions, asset valuation, exchange-rate pressure, financial conditions, liquidity coverage, and investment affordability explicit. These equations do not determine the correct policy stance, but they reveal the channels through which monetary governance reaches the economy.

1. Real Interest Rate

r = i – \pi^e

\]

Interpretation: The real interest rate \(r\) equals the nominal interest rate \(i\) minus expected inflation \(\pi^e\). This helps show why nominal rates alone do not determine the effective cost of borrowing.

2. Debt-Service Burden

DSR = \frac{Debt\ Service}{Income}

\]

Interpretation: The debt-service ratio \(DSR\) compares required debt payments with income. Higher rates can raise debt-service burdens quickly where liabilities reprice frequently.

3. Stylized Monetary Reaction Function

i = i^* + a(\pi – \pi^*) + b(Y – Y^*)

\]

Interpretation: A stylized policy rule links the policy rate \(i\) to a neutral reference rate \(i^*\), the inflation gap \(\pi – \pi^*\), and the output gap \(Y – Y^*\). It formalizes the idea that policy may react to both inflation and real economic slack.

4. Asset Valuation Logic

PV = \sum_{t=1}^{T} \frac{CF_t}{(1+i)^t}

\]

Interpretation: Present value \(PV\) equals the discounted value of future cash flows \(CF_t\). When discount rates rise, the present value of future cash flows generally falls, which helps explain why tighter policy often pressures asset valuations.

5. Exchange-Rate Pressure

\Delta ER = f(i – i_{world}, Risk, Capital\ Flows)

\]

Interpretation: Exchange-rate pressure depends partly on rate differentials, perceived risk, and capital flows. This simplified expression captures why open-economy monetary policy is constrained by international financial conditions.

6. Financial Conditions as Composite Restraint

FCI = f(i, Spreads, Equity\ Prices, Exchange\ Rate, Lending\ Standards, Liquidity)

\]

Interpretation: A financial-conditions index \(FCI\) represents the broader stance of finance, including rates, spreads, asset prices, exchange rates, lending standards, and liquidity. Effective monetary stance is broader than the policy rate alone.

7. Liquidity Coverage

LCR = \frac{Liquid\ Assets}{Short\text{-}Term\ Outflows}

\]

Interpretation: The liquidity coverage ratio \(LCR\) compares liquid assets with short-term outflows. It helps evaluate whether an institution can withstand funding stress without immediate destabilizing sales or emergency support.

8. Public Debt-Service Pressure

DS_{public} = iD

\]

Interpretation: Public debt service \(DS_{public}\) equals the interest rate \(i\) multiplied by the public debt stock \(D\). Higher rates can therefore alter fiscal space, especially when debt rolls over quickly.

9. Sustainable Investment Affordability

IA = R_s – C_f

\]

Interpretation: Investment affordability \(IA\) can be represented as expected social return \(R_s\) minus financing cost \(C_f\). Long-horizon public and resilience investments become harder to finance when monetary tightening raises borrowing costs faster than expected social returns.

10. Practical Interpretation

The mathematical lens clarifies several structural points. Real borrowing cost depends on inflation expectations, not nominal rates alone. Higher rates can raise debt-service stress where balance sheets are exposed. Monetary policy often responds to both inflation and real activity conditions. Asset prices are sensitive to discount-rate changes. Exchange rates and credit spreads mediate the broader stance of policy. Liquidity matters because solvent institutions can still fail under funding stress. Public debt service and sustainable investment affordability are shaped by rate conditions.

Formalization helps reveal mechanism, but it does not determine what weight should be assigned to employment, inflation, housing stress, financial stability, public investment, or long-run resilience. Those remain institutional, ethical, and political questions.

Python Workflow: Monetary Policy, Central Banking, and Financial Conditions

Python is useful for turning monetary-policy concepts into reproducible calculations. The following compact workflow models a real interest rate, debt-service burden, stylized policy rule, financial-conditions index, asset repricing, and sustainable-investment affordability.

# Monetary Policy, Central Banking, and Financial Conditions

# Simple Python workflow

import pandas as pd

# Real interest rate

nominal_rate = 0.055

expected_inflation = 0.025

real_rate = nominal_rate - expected_inflation

print("Real interest rate:", round(real_rate, 3))

# Debt-service burden

debt_service = 1800

income = 6000

dsr = debt_service / income

print("Debt-service ratio:", round(dsr, 3))

# Stylized policy reaction function

neutral_rate = 0.03

inflation_gap = 0.02

output_gap = -0.01

a = 1.2

b = 0.5

policy_rate = neutral_rate + a * inflation_gap + b * output_gap

print("Implied policy rate:", round(policy_rate, 3))

# Simple financial conditions index

spread = 0.02

equity_decline = -0.08

exchange_rate_pressure = 0.03

lending_tightness = 0.04

liquidity_stress = 0.05

fci = (

nominal_rate

+ spread

+ exchange_rate_pressure

+ lending_tightness

+ liquidity_stress

- equity_decline

)

print("Stylized financial conditions index:", round(fci, 3))

# Asset valuation sensitivity

cash_flow = 100

discount_rate_before = 0.04

discount_rate_after = 0.06

duration = 10

pv_before = sum(cash_flow / ((1 + discount_rate_before) ** t) for t in range(1, duration + 1))

pv_after = sum(cash_flow / ((1 + discount_rate_after) ** t) for t in range(1, duration + 1))

valuation_change = (pv_after - pv_before) / pv_before

print("Valuation change after rate shock:", round(valuation_change, 3))

# Sustainable investment affordability

expected_social_return = 0.085

financing_cost = 0.045

rate_shock = 0.015

post_shock_financing_cost = financing_cost + rate_shock

investment_affordability_gap = expected_social_return - post_shock_financing_cost

print("Investment affordability gap:", round(investment_affordability_gap, 3))

df = pd.DataFrame({

"Metric": [

"Real Interest Rate",

"Debt-Service Ratio",

"Implied Policy Rate",

"Financial Conditions Index",

"Valuation Change",

"Investment Affordability Gap"

],

"Value": [

real_rate,

dsr,

policy_rate,

fci,

valuation_change,

investment_affordability_gap

]

})

print(df)

This workflow is useful because it links policy stance, balance-sheet pressure, financial restraint, valuation sensitivity, and long-horizon investment affordability within one simplified analytical frame. It shows why monetary policy cannot be evaluated only by the policy rate or inflation target. What matters is how monetary settings travel through debt, assets, liquidity, public finance, and investment horizons.

The full GitHub repository expands this example into real-rate scenarios, debt-service exposure, financial-conditions indices, asset-repricing simulations, bank-liquidity stress, open-economy pressure, public debt-service interaction, sustainable-investment affordability, SQL queries, R and Stata replication workflows, Julia simulations, and article-ready figures.

R Workflow: Monetary Policy, Central Banking, and Financial Conditions

R is useful for monetary-policy summaries, debt-service comparison, financial-conditions graphics, and publication-ready outputs. The following compact workflow performs the same real-rate, debt-service, policy-rule, financial-conditions, valuation, and investment-affordability calculations in R.

# Monetary Policy, Central Banking, and Financial Conditions

# Simple R workflow

# Real interest rate

nominal_rate <- 0.055

expected_inflation <- 0.025

real_rate <- nominal_rate - expected_inflation

cat("Real interest rate:", round(real_rate, 3), "\n")

# Debt-service burden

debt_service <- 1800

income <- 6000

dsr <- debt_service / income

cat("Debt-service ratio:", round(dsr, 3), "\n")

# Stylized policy reaction function

neutral_rate <- 0.03

inflation_gap <- 0.02

output_gap <- -0.01

a <- 1.2

b <- 0.5

policy_rate <- neutral_rate + a * inflation_gap + b * output_gap

cat("Implied policy rate:", round(policy_rate, 3), "\n")

# Simple financial conditions index

spread <- 0.02

equity_decline <- -0.08

exchange_rate_pressure <- 0.03

lending_tightness <- 0.04

liquidity_stress <- 0.05

fci <- nominal_rate +

spread +

exchange_rate_pressure +

lending_tightness +

liquidity_stress -

equity_decline

cat("Stylized financial conditions index:", round(fci, 3), "\n")

# Asset valuation sensitivity

cash_flow <- 100

discount_rate_before <- 0.04

discount_rate_after <- 0.06

duration <- 10

pv_before <- sum(cash_flow / ((1 + discount_rate_before) ^ (1:duration)))

pv_after <- sum(cash_flow / ((1 + discount_rate_after) ^ (1:duration)))

valuation_change <- (pv_after - pv_before) / pv_before

cat("Valuation change after rate shock:", round(valuation_change, 3), "\n")

# Sustainable investment affordability

expected_social_return <- 0.085

financing_cost <- 0.045

rate_shock <- 0.015

post_shock_financing_cost <- financing_cost + rate_shock

investment_affordability_gap <- expected_social_return - post_shock_financing_cost

cat("Investment affordability gap:", round(investment_affordability_gap, 3), "\n")

summary_df <- data.frame(

Metric = c(

"Real Interest Rate",

"Debt-Service Ratio",

"Implied Policy Rate",

"Financial Conditions Index",

"Valuation Change",

"Investment Affordability Gap"

),

Value = c(

real_rate,

dsr,

policy_rate,

fci,

valuation_change,

investment_affordability_gap

)

)

print(summary_df)

This R workflow is deliberately compact for article readability. In the full repository, R reads structured policy-rate, debt-service, financial-conditions, asset-valuation, liquidity, open-economy, public-debt, and sustainable-investment scenarios; calculates real rates, policy-rule rates, debt-service exposure, financial-conditions indices, and investment affordability; and visualizes monetary tightening, financial stress, and resilience-financing tradeoffs.

Future Economic Systems articles can extend this foundation with central-bank policy series, yield curves, household debt data, bank balance sheets, credit spreads, exchange-rate data, debt-maturity profiles, asset-price data, mortgage-rate series, and public investment finance datasets.

GitHub Repository

The article body includes selected computational examples so the conceptual, institutional, and mathematical argument remains readable. The full repository contains the expanded research infrastructure: Python real-rate and financial-conditions analysis, R monetary-policy summaries, Stata applied monetary economics replication workflows, SQL monetary and balance-sheet scenario tables, Julia policy-rate simulations, debt-service stress, asset repricing, bank-liquidity analysis, open-economy pressure, public-debt interaction, sustainable-investment affordability, documentation, reproducible sample data, and article-ready figures and tables.

Complete Code Repository

The full code distribution for this article, including selected article examples and advanced research-style computational scaffolding for real interest rates, debt-service burdens, policy reaction functions, financial-conditions indices, asset valuation, bank liquidity, lender-of-last-resort stress, exchange-rate pressure, public-debt service, sustainable-investment affordability, reproducibility documentation, and cross-language economic analysis, is available on GitHub.

Conclusion

Monetary policy, central banking, and financial conditions are central to economic analysis because they show how modern economies govern money, credit, liquidity, and adjustment across time. Central banks do more than move rates. They help maintain settlement infrastructure, influence borrowing conditions, shape asset valuations, contain panic, and structure the monetary environment in which households, firms, banks, markets, and governments make decisions.

To understand an economic system seriously, one must therefore ask not only what the policy rate is, but how financial conditions are evolving, how transmission works through debt and balance sheets, who bears the burden of adjustment, and whether monetary governance supports resilient and productive forms of investment rather than merely preserving nominal order in the short run. These questions reveal whether the monetary system is widening future possibility or organizing stability through increasingly unequal and fragile forms of economic adjustment.

The serious study of monetary governance also reveals why central banking cannot be separated from public legitimacy. A monetary order may control inflation while worsening housing exclusion, suppressing labor, increasing debt stress, or making public investment harder to finance. It may also support activity while encouraging leverage and speculative asset inflation. The challenge is therefore not merely technical calibration, but institutional judgment about the kind of stability being pursued.

In a sustainable economic system, monetary policy must be coordinated with fiscal capacity, financial regulation, housing systems, energy transition, infrastructure investment, and household security. Price stability matters, but it should not be purchased by undermining the foundations of long-run resilience. Central banking is one of the key institutions through which societies govern uncertainty. Its deepest test is whether it helps make durable, equitable, and future-oriented economic life possible.

Related Reading

- Economic Systems

- Money, Banking, Credit, and Financial Intermediation

- Finance, Leverage, and Systemic Risk

- Macroeconomic Stability, Business Cycles, and Crisis

- Inflation, Energy Shocks, and Supply Constraints

- Fiscal Policy, Taxation, and Public Investment

- Public Finance, State Capacity, and Collective Goods

- Risk & Resilience

- Sustainable Development

Further Reading

- Bank for International Settlements (BIS) (n.d.). Monetary Policy and Financial Stability. Available at: https://www.bis.org/

- Bank of England (n.d.). Monetary Policy. Available at: https://www.bankofengland.co.uk/monetary-policy

- European Central Bank (ECB) (n.d.). Monetary Policy. Available at: https://www.ecb.europa.eu/mopo/html/index.en.html

- Federal Reserve (n.d.). Monetary Policy. Available at: https://www.federalreserve.gov/monetarypolicy.htm

- Federal Reserve Bank of Chicago (n.d.). National Financial Conditions Index. Available at: https://www.chicagofed.org/research/data/nfci/current-data

- International Monetary Fund (IMF) (n.d.). Monetary Policy. Available at: https://www.imf.org/en/Topics/monetary-policy

- International Monetary Fund (IMF) (n.d.). Global Financial Stability Report. Available at: https://www.imf.org/en/Publications/GFSR

References

- Bank for International Settlements (BIS) (n.d.). Monetary Policy and Financial Stability. Available at: https://www.bis.org/

- Bank of England (n.d.). Monetary Policy. Available at: https://www.bankofengland.co.uk/monetary-policy

- European Central Bank (ECB) (n.d.). Monetary Policy. Available at: https://www.ecb.europa.eu/mopo/html/index.en.html

- Federal Reserve (n.d.). Monetary Policy. Available at: https://www.federalreserve.gov/monetarypolicy.htm

- Federal Reserve Bank of Chicago (n.d.). National Financial Conditions Index. Available at: https://www.chicagofed.org/research/data/nfci/current-data

- International Monetary Fund (IMF) (n.d.). Monetary Policy. Available at: https://www.imf.org/en/Topics/monetary-policy

- International Monetary Fund (IMF) (n.d.). Global Financial Stability Report. Available at: https://www.imf.org/en/Publications/GFSR