Last Updated May 9, 2026

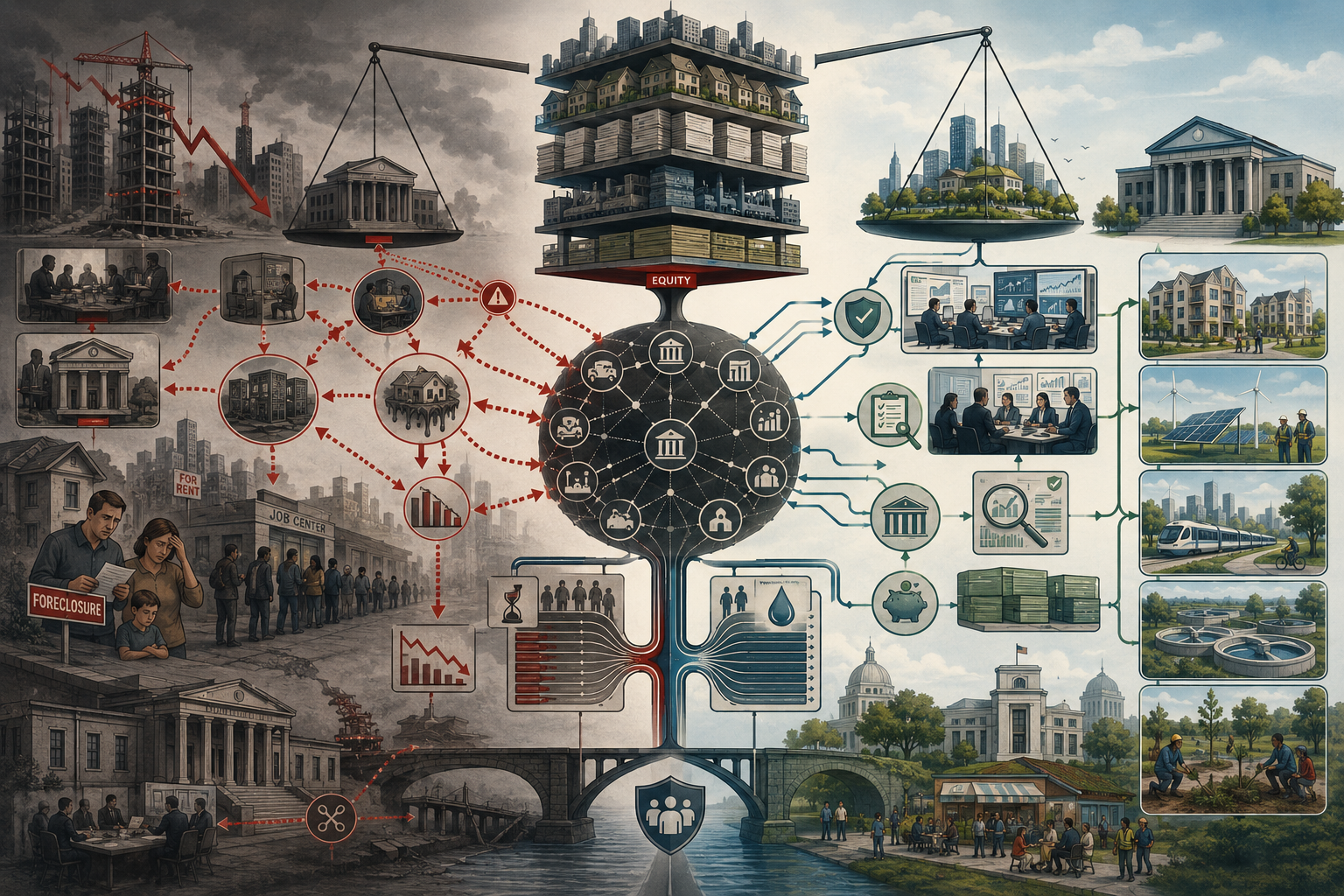

Finance, leverage, and systemic risk are central to economic analysis because modern economies operate not only through production and exchange, but through layered claims, balance sheets, collateral structures, liquidity promises, and expectations about refinancing, repayment, and public support. Finance is often justified as the mechanism through which savings are mobilized, risk is allocated, liquidity is provided, and investment is made possible across time. In that narrow sense, it appears as a supporting system for the wider economy. But finance does more than support production. It transforms claims, amplifies incentives, redistributes uncertainty, and structures who is exposed to loss when conditions change.

Leverage intensifies these effects by allowing assets, income streams, or collateral to support obligations far larger than the underlying equity base. When asset prices rise, funding remains cheap, and liquidity appears abundant, leverage can magnify returns and make large-scale investment or speculation possible. But when prices fall, refinancing tightens, collateral values decline, or confidence weakens, leverage magnifies losses just as forcefully. What looked efficient under calm conditions can become fragile under stress.

Systemic risk emerges when these arrangements become so interconnected that distress in one part of the financial structure can spread rapidly across institutions, markets, households, public balance sheets, and the wider economy. To understand leverage and systemic risk seriously, one must move beyond isolated firm-level reasoning. Individual actors may appear rational when borrowing against rising asset prices, extending maturity mismatch, or relying on short-term funding in pursuit of higher returns. Yet what seems prudent or profitable at the level of one institution can become dangerous at the level of the system when many actors follow similar strategies simultaneously.

Main Library

Publications

Article Map

Economic Systems

Related Topic

Sustainable Development

Related Topic

Institutions & Governance

Related Topic

Risk & Resilience

Within a sustainable systems framework, finance, leverage, and systemic risk must be examined not only in relation to crisis prevention, but also in relation to resilience, public capacity, long-horizon investment, ecological transition, and the governance of uncertainty. A financial system may generate high returns while underpricing ecological exposure, destabilizing housing, misallocating credit, and depending on public rescue when private risk-taking fails. The deeper question is not only how leverage works, but what kinds of futures a leveraged system makes possible, fragile, or unfinanceable.

Why This Topic Matters

Finance, leverage, and systemic risk matter because modern economies do not operate only through flows of production and exchange. They also operate through stocks of claims, expectations of repayment, maturity structures, collateral values, and institutions that promise liquidity under conditions that may not always be stable. When these financial structures are sound, they can support investment, coordination, and resilience. When they become overextended, opaque, or excessively leveraged, they can destabilize the very economic systems they are meant to support.

This matters analytically because leverage changes the scale of exposure relative to underlying equity or cash flow. It allows actors to control larger positions with less of their own capital, magnifying returns when prices rise or funding is cheap. But it also magnifies loss when prices fall, revenue weakens, or refinancing becomes difficult. In highly connected systems, many actors may discover at once that what looked manageable individually has become collectively unstable.

These issues also matter politically. Losses from financial instability are rarely borne only by the institutions that took the risk. Credit contraction can reduce employment, depress public revenues, damage household wealth, and trigger interventions by central banks and states. Financial gains may be privatized in expansion while systemic losses are socialized in collapse. This is one reason systemic risk is never purely a technical matter. It raises questions of governance, legitimacy, accountability, and whose balance sheets are ultimately expected to absorb failure.

Systemic risk is therefore not just about rare crisis events. It is about how an economy structures vulnerability in normal times. It concerns whether the search for yield, liquidity, and leverage quietly accumulates exposures that only become visible once stress has already spread.

Finance is also one of the principal places where uncertainty is converted into tradable form. Instruments that seem to disperse risk can also obscure its concentration. What appears diversified at the level of contract design may remain fragile at the level of the system if many actors depend on the same assumptions about liquidity, growth, collateral, or public rescue.

What Finance Does

Finance coordinates claims across time. It links current funds to future return, enables households and firms to smooth spending, allows investment to occur before all savings have been accumulated, and permits risk to be transferred or pooled across institutions. In this sense, finance performs useful functions. It supports capital formation, liquidity management, payment systems, and the infrastructures of credit on which complex economies depend.

But finance does not merely transfer resources. It transforms them. It converts short-term liabilities into long-term assets, illiquid positions into seemingly liquid claims, risky income streams into rated securities, and uncertain futures into priced contracts. This transformation is what makes finance dynamic, but it is also what makes it fragile. Every such transformation depends on assumptions about confidence, rollover, market depth, and institutional support.

Finance therefore operates as a system of organized promise. It structures who can access liquidity, who can refinance, who can hedge, who can obtain collateralized funding, and who must bear residual risk. To study finance seriously is to study not just capital allocation, but the architecture through which uncertainty is distributed and made temporarily governable.

A research-grade account must therefore resist the tendency to treat finance as either purely parasitic or purely productive. It is both enabling and potentially destabilizing. Its value depends on how it is structured, what it finances, how losses are allocated, and whether its private incentives align with public resilience.

Finance also governs pace. It accelerates investment and speculation by relaxing immediate resource constraints, but it can also accelerate collapse when claims are too dense, buffers too thin, or expectations too synchronized. Its role in the economy is inseparable from its role in shaping speed, sensitivity, and reversibility.

What Leverage Is

Leverage refers to the use of borrowed funds or other fixed obligations to expand exposure beyond what an actor’s own equity would otherwise support. A leveraged institution controls a larger asset position relative to its own capital base than an unleveraged one. This can occur through traditional borrowing, repo funding, derivatives exposure, margin lending, securitization structures, off-balance-sheet vehicles, and other arrangements that create claims larger than the underlying equity cushion.

Leverage is not merely an accounting ratio. It is a structural relation between promise and buffer. The higher the leverage, the smaller the loss required to wipe out a given amount of equity. What appears manageable under stable prices can become dangerous under modest adverse movement when the buffer protecting creditors, depositors, counterparties, or public backstops is thin.

Leverage can also be direct or indirect. A household mortgage is a clear form of leverage. So is corporate borrowing for asset acquisition. But leverage can also be embedded in structured products, collateral chains, derivatives books, private funds, and off-balance-sheet vehicles. One of the central difficulties of systemic analysis is that leverage often exists in forms more opaque than simple debt-to-equity metrics suggest.

Leverage is therefore best understood not only as a ratio, but as a systemic amplifier. It allows a larger present to be constructed out of a smaller capital base, while simultaneously making the future more sensitive to changes in prices, funding, and confidence.

Leverage also changes behavior. When upside is magnified relative to equity and downside is partly shifted to creditors, counterparties, or public backstops, actors may rationally prefer thinner buffers than collective resilience would require. This is one reason leverage is never merely a private choice. It is a governance problem.

Why Leverage Is Attractive

Leverage is attractive because it increases return on equity when conditions are favorable. If borrowed funds can be obtained cheaply and invested in assets yielding more than their financing cost, the spread accrues disproportionately to the equity holder. This is one of the basic reasons finance repeatedly expands leverage during periods of stability, low interest rates, rising asset prices, or compressed risk spreads.

Leverage can look prudent from the viewpoint of individual optimization. Managers may be rewarded for higher returns. Investors may seek amplified gains. Institutions may compete in environments where remaining underleveraged appears conservative to the point of underperformance. The pressures toward leverage are therefore built into compensation systems, competitive norms, benchmark comparisons, and expectations about financial sophistication.

Leverage is also attractive because it can make large-scale investment possible without requiring full prior equity funding. Infrastructure, housing, industrial expansion, working-capital management, public investment, and business growth often depend on some use of debt. The issue is not leverage as such, but what kind of leverage, on what terms, backed by what cash flows or public purposes, and governed under what safeguards.

The central problem is that the same mechanisms that make leverage attractive in ordinary times can make systems brittle under stress. The pursuit of higher return through thinner equity buffers tends to create fragility precisely because success encourages imitation and scale.

Leverage also thrives on narrative. Rising markets create stories of permanent liquidity, improved diversification, superior risk management, structurally higher valuations, or a new financial regime. These narratives help normalize leverage by making contingency appear temporary and by reclassifying fragility as innovation.

Fragility and Balance-Sheet Amplification

Leverage makes financial systems fragile because losses are absorbed first by relatively small equity buffers. A modest decline in asset values can therefore generate a disproportionate decline in net worth. Once equity becomes impaired, lenders may withdraw funding, margin requirements may rise, counterparties may demand additional collateral, and institutions may be forced to sell assets quickly into falling markets.

Balance-sheet deterioration is rarely isolated. Declining asset values worsen leverage ratios, which can force deleveraging, which can push prices lower, which can worsen balance sheets further. What begins as a price movement becomes a balance-sheet spiral. This is one of the core mechanisms through which financial distress becomes self-reinforcing.

Fragility also arises because many liabilities are contractual and time-specific while asset values are uncertain and market-dependent. Interest must be paid, collateral posted, funding rolled, and obligations met even when prices move sharply or liquidity vanishes. Financial systems are vulnerable not only because assets may lose value, but because fixed claims remain fixed when everything else becomes unstable.

This balance-sheet amplification is one reason financial crises can seem sudden. The underlying vulnerability may have built slowly over years, but once the cushion is thin enough and the trigger arrives, deterioration accelerates rapidly because the system itself magnifies the shock.

The deeper issue is that fragility is endogenous to the structure of finance. It is produced by the interaction between asset valuation, debt obligations, liquidity promises, collateral rules, and institutional behavior. The system generates its own sensitivity by building too much present capacity on too little loss-absorbing space.

Systemic Risk Beyond the Individual Firm

Systemic risk refers to the possibility that distress in one part of the financial system can spread broadly enough to impair the functioning of the system as a whole and thereby damage the wider economy. This distinguishes it from ordinary firm-level risk. A single institution can fail without threatening the system if it is small, isolated, or easily resolved. Systemic institutions, markets, and funding channels matter because their failure or retrenchment can destabilize credit, payments, liquidity, and confidence across many others.

The financial system is not merely a collection of separate actors. It is a network of balance sheets, collateral links, payment obligations, shared exposures, correlated strategies, and expectations about public response. The behavior of one institution affects the solvency, liquidity, and strategy of others. Risk is therefore endogenous to the structure of interconnection.

Systemic risk also means that what appears diversified from the viewpoint of one institution may still be concentrated at the level of the system. Many firms can hold “different” assets while relying on similar funding models, similar collateral assumptions, similar models of volatility, or similar macroeconomic conditions. Correlation often becomes most visible precisely when the system is already under stress.

A serious analysis of finance must therefore shift from microprudence to macroprudence. The question is not only whether each institution appears safe in isolation, but whether their collective behavior generates a stable or unstable system.

Systemic risk is a problem of composition. Actions that are prudent for one balance sheet can become destructive when generalized. Selling assets to preserve solvency, hoarding cash to preserve liquidity, or tightening collateral to preserve lending discipline may all be individually rational and collectively destabilizing.

Interconnectedness, Contagion, and Network Effects

Financial institutions are connected through interbank lending, repo markets, derivatives exposures, payment obligations, shared asset holdings, clearing systems, collateral chains, and common funding providers. These connections make ordinary financial coordination possible, but they also create channels of contagion. A funding shock, default, or asset-sale pressure in one part of the network can propagate rapidly through others.

Contagion is not only psychological panic. It often moves through concrete contractual and balance-sheet linkages. If one institution fails to meet obligations, another institution’s asset becomes impaired. If one fund sells into a falling market, identical or correlated holdings elsewhere lose value. If one part of the network is suspected of weakness, counterparties may retreat from a much broader set of institutions.

Network effects also matter because resilience is not determined only by the number of connections, but by their structure. Dense interconnection can spread shocks rapidly. Heavy concentration in a few hubs can create single points of failure. Chains of collateral or funding dependence can generate complexity that obscures where the real vulnerability lies until stress forces revelation.

Contagion therefore shows why transparency and simplicity matter. A system may appear robust when connections are profitable and liquid, yet become extremely fragile when those same connections serve as channels for rapid loss transmission.

Interconnection also alters politics. Institutions that sit at critical nodes of payment, collateral, clearing, settlement, or funding networks acquire outsized systemic importance. Their private decisions can have public consequences disproportionate to their formal ownership or balance-sheet size.

Liquidity Risk, Funding Risk, and Runs

Liquidity risk arises when institutions or markets cannot obtain cash or cash-equivalent funding quickly enough to meet obligations without severe loss. Funding risk is the related danger that short-term liabilities cannot be rolled over on acceptable terms. These problems are especially acute in systems that rely on short-term borrowing to support long-duration or hard-to-sell assets.

Solvency and liquidity are different. An institution may hold assets that exceed liabilities over the long run and still fail if it cannot meet immediate payment demands. This is the logic behind bank runs, wholesale funding freezes, margin spirals, and sudden withdrawals from money-like instruments. The timing of cash flow matters as much as the total value of assets on paper.

Runs are not limited to retail depositors standing in lines outside banks. Modern runs can occur in repo markets, money-market funds, prime brokerage relationships, stable funding facilities, digital platforms, private funds, or any domain where claimants lose confidence and rush toward safer instruments. Contemporary runs are often institutional, digital, and rapid.

The study of runs reveals the political core of finance. Systems that promise liquidity against illiquid assets depend implicitly or explicitly on institutions willing to stabilize them in stress. The question is always who receives that stabilization, under what terms, and after how much damage has already been done.

Liquidity crises also reveal how much of normal financial life depends on continual renewal of trust. Funding is often assumed rather than secured in any deep sense. The moment that assumption weakens, entire chains of leverage can become unstable before slower-moving measures of solvency have time to matter.

Collateral, Fire Sales, and Procyclicality

Collateral is central to leveraged finance because it secures borrowing and determines which institutions can access funding cheaply. But collateral values are not fixed. When asset prices fall, the same institutions that looked well-secured may be required to post more collateral, reduce leverage, or liquidate assets. This can trigger fire sales in which many actors attempt to sell simultaneously into thin or fearful markets.

Fire sales are procyclical. They reinforce the direction of stress. Falling prices worsen balance sheets, worsening balance sheets force sales, forced sales push prices lower, and lower prices then worsen balance sheets elsewhere. Collateral rules that seem prudent individually can therefore become destabilizing collectively.

Procyclicality is one of the deepest problems in financial governance. Practices that appear conservative at the level of a single creditor or firm can intensify downturns when adopted broadly. Margin calls, collateral haircuts, mark-to-market losses, liquidity rules, and risk-model adjustments can all strengthen the same spiral if they move with the cycle rather than against it.

For this reason, systemic resilience often requires countercyclical institutions and buffers. Left purely to market discipline, collateralized leverage tends to become most expansive in good times and most destructive in bad times.

Procyclicality also has a knowledge problem. It often appears only after the turn. Rules calibrated on recent history seem prudent while they are building the very fragility that later makes them systemically destabilizing.

Shadow Banking and Hidden Leverage

Hidden leverage often accumulates outside the most visible regulatory perimeter. Investment funds, securitization vehicles, derivatives structures, private-credit arrangements, money-market instruments, structured products, repo chains, and market-based funding channels can all perform leverage-like functions without appearing as conventional bank debt. These forms of leverage may be contractual, synthetic, or embedded in valuation and collateral arrangements rather than in straightforward loans.

Hidden leverage is difficult to monitor. Institutions can appear lightly leveraged on one measure while remaining highly exposed through off-balance-sheet obligations, derivative positions, liquidity commitments, or dependence on short-term secured funding. The system may therefore look safer than it is because measurement conventions do not fully capture the structure of contingent obligation.

Shadow banking also matters because it relies heavily on confidence in collateral and market liquidity. When those weaken, institutions without stable public backstops can face rapid runs that spill back into the regulated banking core. The distinction between regulated and unregulated finance often breaks down precisely when systemic support becomes unavoidable.

A research-grade treatment of leverage must therefore treat legal form with caution. The real question is not whether an institution is called a bank, but whether it performs bank-like liquidity and leverage functions under fragile funding conditions.

Shadow banking also reveals how financial systems evolve around rules. Regulation can harden one part of the perimeter while risk migrates elsewhere, often into structures celebrated as innovative until their dependence on systemic support becomes undeniable.

Asset Prices, Speculation, and the Cycle of Euphoria

Leverage and systemic risk are closely tied to asset-price dynamics. Rising asset prices improve collateral values, make balance sheets look stronger, lower measured leverage ratios, and encourage both lenders and borrowers to expand positions further. This can create a self-reinforcing cycle in which price appreciation validates additional leverage, which then supports additional price appreciation.

Speculative dynamics often appear rational while they are unfolding. Participants observe rising prices, expanding liquidity, and low default rates and infer that greater leverage is manageable. Yet the apparent stability is partly produced by the same upward cycle that is increasing fragility beneath the surface. The system becomes most confident near the point of greatest hidden vulnerability.

Euphoria is therefore not just a psychological phenomenon. It is institutionalized through risk models, collateral practices, compensation systems, benchmark comparisons, analyst narratives, and the social pressure not to underperform in rising markets. Speculation becomes systemic when it is financed and normalized at scale.

When reversal comes, what had seemed like wealth creation can reveal itself as balance-sheet inflation built on unstable expectations. The price cycle and the leverage cycle are therefore often two sides of the same systemic process.

Speculative euphoria also deforms allocation. Credit that might have supported maintenance, productive upgrading, public infrastructure, or resilience can be drawn into rising asset classes because mark-to-market gains appear faster, cleaner, and more prestigious than slower forms of long-horizon investment.

Endogenous Instability and the Production of Crisis

One of the most important insights in systemic finance is that instability is often endogenous. It is produced by the normal functioning of the system rather than imposed entirely from outside. Stability itself can breed risk-taking: successful refinancing, rising collateral values, compressed spreads, low recent losses, and calm volatility can encourage more aggressive funding structures and thinner margins of safety.

This changes how crisis is interpreted. Rather than viewing panic as an irrational interruption of an otherwise stable order, one must often see it as the revelation of fragility accumulated during the calm. The conditions that make a boom appear orderly may be the same conditions that are making it dangerous.

Endogenous instability also explains why reform is often politically difficult. The very actors benefiting from expansion have little incentive to slow leverage, widen buffers, or restrain speculative gain while the upswing continues. This creates a systematic bias toward reacting after fragility becomes visible rather than preventing it beforehand.

A research-grade framework therefore treats crisis not only as breakdown but as diagnosis. It reveals what the system had been depending on all along: refinancing, cheap leverage, stable collateral, narrow volatility, correlated optimism, and public willingness to absorb extreme failure when private structures proved incapable of self-stabilization.

Endogenous instability is therefore not an exception to finance. It is a recurrent tendency of systems that reward risk expansion during calm and require collective rescue when private risk becomes public danger.

Public Backstops, Moral Hazard, and Financial Power

Modern financial systems depend heavily on public backstops even when much risk-taking is privately initiated. Deposit insurance, lender-of-last-resort facilities, emergency liquidity support, asset purchases, guarantees, resolution regimes, swap lines, and ad hoc crisis interventions all exist because the collapse of leveraged financial systems imposes costs too large to leave entirely to private adjustment.

Backstops are double-edged. They reduce panic and protect the wider economy, but they can also create moral hazard if institutions expect that sufficiently important liabilities will be protected in crisis. Gains remain private in the upswing, while catastrophic losses are partially transferred to the public balance sheet in the downswing.

This dynamic has major political consequences. It raises questions about legitimacy, accountability, compensation, regulation, and the terms on which support is extended. A society may tolerate public rescue when payment systems, pensions, public finance, or employment are at stake, but it does not follow that private leverage should remain lightly governed in normal times.

The existence of public backstops means that finance is never fully private. Systemic importance confers a kind of political power because institutions that can threaten broad damage acquire implicit bargaining leverage over the state.

Public support therefore needs conditions, not merely availability. Without ex ante discipline and ex post accountability, rescue can become a standing subsidy to fragility rather than a temporary defense of the wider social order.

Households, Housing, and Everyday Systemic Risk

Systemic risk is often discussed in terms of large institutions, but it also operates through household finance. Housing systems are a major example. Mortgage leverage links household balance sheets, bank assets, property markets, construction activity, local public revenues, insurance systems, and macroeconomic confidence. When house prices rise alongside easy credit, households may feel wealthier and lenders safer. When the cycle reverses, distress spreads through defaults, falling collateral, reduced consumption, and damaged banking balance sheets.

Housing is both a basic social need and a major financial asset class. The more housing systems are organized through leverage and speculative price appreciation, the more everyday life becomes entangled with systemic financial dynamics. Household shelter becomes dependent on credit conditions, refinancing capacity, interest rates, and asset valuation.

Household leverage also matters because it distributes systemic fragility downward. Wage stagnation, rising rents, emergency borrowing, variable-rate debt, thin savings cushions, medical debt, student debt, and consumer credit make ordinary households part of the wider architecture of financial vulnerability. What looks like private choice may in fact reflect institutional dependence on debt for basic stability.

A serious account of systemic risk must therefore include the household sector. Financial fragility is not only a problem of investment banks and trading desks. It is also a problem of how basic life conditions become organized through leverage.

This is where finance meets social reproduction directly. A system that relies on expanding household indebtedness to sustain consumption, housing access, education, or health care may appear functional while quietly shifting systemic pressure into everyday life.

Macroprudential Governance and Resilience

Macroprudential governance refers to regulatory and supervisory approaches aimed at the stability of the financial system as a whole rather than at the solvency of individual institutions alone. This includes capital requirements, liquidity requirements, leverage caps, stress testing, countercyclical buffers, loan-to-value limits, debt-service limits, funding rules, resolution regimes, and systemic oversight of interconnected markets and nonbank institutions.

Systemic stability cannot be secured through micro-level prudence alone. Even well-managed institutions can become collectively dangerous if they are similarly exposed, similarly leveraged, or similarly reliant on fragile funding. Macroprudential policy exists because the system has properties that are not visible from the viewpoint of the single firm.

Resilience also depends on governance beyond formal regulation. Market structure, simplicity of instruments, accounting clarity, resolution regimes, public transparency, institutional memory, and political willingness to restrain unstable financial expansion all matter. A resilient system is not merely one that survives stress, but one that is less likely to generate socially intolerable stress in the first place.

Macroprudential governance therefore represents a shift in perspective: from finance as isolated contract to finance as system, from prudence as firm discipline to prudence as collective architecture, and from crisis response to preemptive resilience-building.

True resilience also requires institutional memory. Financial systems repeatedly reinvent fragility in new forms. Governance must therefore be historically informed enough to recognize familiar dynamics beneath new instruments, new platforms, and new vocabularies of innovation.

Finance, Leverage, and Sustainable Systems

Within sustainable systems, leverage must be judged not only by private return, but by whether it finances resilience or fragility. Credit can help build energy transition, public transit, water systems, health infrastructure, housing, adaptation, maintenance, and productive capacity. But leverage can also fund speculative extraction, fragile housing bubbles, fossil lock-in, land inflation, and highly interconnected systems that fail under stress. The quantity of leverage tells us little unless we know its direction and purpose.

Sustainable development requires patient, durable, and publicly accountable forms of finance. Many of the most important long-horizon investments generate diffuse benefits, uncertain timing, or returns not easily captured by private balance sheets alone. Systems organized around high leverage and short-term yield may systematically underfinance such needs.

Systemic risk also has an ecological dimension. If climate shocks, energy disruption, insurance withdrawal, infrastructure failure, or stranded-asset dynamics are underpriced in leveraged systems, financial fragility can intensify precisely where resilience investment is most needed. Sustainable systems therefore require financial architectures that can recognize deep uncertainty rather than merely extrapolate from stable recent history.

In this sense, the governance of leverage is inseparable from the governance of the future. The question is whether finance multiplies claims on unstable foundations or helps build the infrastructures and institutions capable of carrying collective life through uncertainty.

Sustainable finance cannot be reduced to labeling. What matters is whether leverage, maturity structure, collateral practice, risk governance, and public support are aligned with long-run resilience rather than merely wrapped in a green vocabulary while short-horizon fragility remains unchanged.

Systemic Time Horizons and Long-Tail Risk

Leverage tends to compress time. It rewards near-term return on equity and often assumes that refinancing, liquidity, and collateral conditions will remain favorable long enough for positions to be managed gradually. Long-tail risks do not fit comfortably inside this logic because they may appear remote, nonlinear, difficult to price, or difficult to hedge until they arrive abruptly.

Many of the most consequential risks in contemporary systems are long-horizon and slow-building: climate exposure, infrastructure deterioration, insurance retreat, demographic pressure, ecological stress, cyber vulnerability, geopolitical fragmentation, and political distrust. A leveraged system focused on short-duration metrics may underprice these risks precisely because they fall outside the normal decision horizon of competitive finance.

A research-grade treatment of systemic risk must therefore consider temporal mismatch not only in funding, but in perception. Short-term balance-sheet optimization can coexist with long-term systemic weakening. This is one of the deepest reasons why resilient finance requires institutions able to see beyond the horizon of immediate market reward.

The problem is not merely that some risks are unknown. It is that the structure of leveraged finance often creates incentives not to look too closely at distant fragility while current spreads, valuations, and performance remain favorable.

A sustainable financial system must therefore lengthen the horizon of prudence. It must ask not only whether obligations can be rolled over next quarter, but whether the underlying system being financed will remain socially, ecologically, and institutionally viable over time.

How Systemic Finance Should Be Judged

Finance, leverage, and systemic risk should not be judged only by profitability, liquidity, asset growth, or credit expansion during normal times. A broader economic systems framework asks whether financial architecture remains resilient under stress, limits harmful amplification, allocates risk fairly, and supports long-horizon public value.

| Dimension | Narrow Question | Systems Question |

|---|---|---|

| Finance | Does finance allocate funds? | Does finance support productive, resilient, inclusive, and long-horizon investment? |

| Leverage | Does leverage raise return on equity? | Does leverage create loss amplification, fragility, or dependence on public rescue? |

| Collateral | Is borrowing secured? | Can collateral rules trigger procyclical margin calls, funding gaps, and fire sales? |

| Liquidity | Can assets be sold or funded? | Can institutions meet obligations under stress without destabilizing the system? |

| Interconnection | Are firms diversified? | Do shared exposures, funding links, and network hubs transmit distress across the system? |

| Households | Can households borrow? | Does household leverage support stability or make basic life dependent on fragile credit cycles? |

| Public Backstops | Can the state stop panic? | Are public guarantees paired with accountability, restraint, and ex ante risk governance? |

| Sustainability | Does finance expand? | Does leverage build resilience, decarbonization, maintenance, and public capacity, or multiply claims on fragile foundations? |

This framework prevents a common mistake: treating private financial success during expansion as evidence of systemic health. A leveraged system may look efficient precisely when it is accumulating fragility. The central question is therefore not whether finance is profitable under normal conditions, but whether it remains socially tolerable under stress.

A good financial system should make socially necessary investment financeable while limiting the forms of leverage, opacity, and procyclicality that convert private risk-taking into public crisis.

Mathematical Lens

Mathematics can clarify finance, leverage, and systemic risk by making amplification, collateral constraints, funding gaps, and network dependence explicit. These equations do not determine what level of leverage is socially acceptable, but they reveal why apparently small shocks can become systemically dangerous.

1. Basic Leverage Ratio

Leverage = \frac{A}{E}

\]

Interpretation: Leverage equals total assets \(A\) divided by equity \(E\). The higher this ratio, the thinner the equity cushion relative to the asset position.

2. Debt-to-Equity Ratio

\frac{D}{E} = \frac{Debt}{Equity}

\]

Interpretation: The debt-to-equity ratio compares fixed obligations \(D\) with the equity buffer \(E\). It highlights how much borrowed funding is supported by the capital base.

3. Equity Loss Amplification

\frac{\Delta E}{E} \approx -Leverage \times x

\]

Interpretation: If assets fall in value by a fraction \(x\), the effect on equity is amplified by leverage. This illustrates why small percentage declines in asset value can produce very large percentage declines in equity when leverage is high.

4. Margin and Collateral Constraint

Borrowing \leq (1 – h) \times Collateral\ Value

\]

Interpretation: Borrowing is constrained by collateral value and haircut \(h\). When collateral values fall or haircuts rise, available borrowing shrinks, potentially forcing deleveraging.

5. Fire-Sale Spiral Logic

P_{t+1} = P_t – f(Sales_t)

\]

Interpretation: Forced sales can reduce asset prices. Lower prices then weaken balance sheets and can trigger further sales.

Sales_t = g(Leverage_t, Margin\ Calls_t, Funding\ Stress_t)

\]

Interpretation: Sales are driven by leverage, margin calls, and funding stress. Together these equations describe the feedback loop through which deleveraging becomes self-reinforcing.

6. Systemic Exposure as Network Dependence

Risk_{system} = f(Leverage, Correlation, Interconnectedness, Liquidity\ Fragility)

\]

Interpretation: Systemic risk depends not only on individual positions, but on shared exposures, correlation, network structure, and liquidity fragility.

7. Simple Funding Gap Condition

FG = ST_{liab} – LQ_{assets}

\]

Interpretation: The funding gap \(FG\) equals short-term liabilities \(ST_{liab}\) minus liquid assets \(LQ_{assets}\). When the gap is positive and rollover fails, institutions must sell assets, obtain emergency support, or default.

8. Practical Interpretation

The mathematical lens clarifies several structural points. Leverage magnifies both gains and losses. Thin equity buffers make small shocks dangerous. Collateral rules can force deleveraging under stress. Fire sales are self-reinforcing rather than one-off events. Systemic risk depends on correlation and network structure, not only on individual prudence. Short-term funding dependence can make apparently solvent institutions unstable.

Formalization helps reveal the mechanics of amplification, but it does not determine what level of leverage is socially acceptable, which risks should be publicly backstopped, or what should count as resilient finance. Those remain institutional, ethical, and political questions.

Python Workflow: Finance, Leverage, and Systemic Risk

Python is useful for turning leverage and systemic-risk concepts into reproducible stress scenarios. The following compact workflow models leverage, asset-price shocks, equity loss amplification, collateral haircuts, funding gaps, and short-term liquidity stress.

# Finance, Leverage, and Systemic Risk

# Simple Python workflow

import numpy as np

import pandas as pd

# Initial balance sheet

assets = 1000

debt = 900

equity = assets - debt

leverage = assets / equity

de_ratio = debt / equity

print("Initial leverage:", round(leverage, 2))

print("Initial debt-to-equity:", round(de_ratio, 2))

# Asset-price shock scenarios

shock = np.array([0.02, 0.05, 0.08, 0.10])

assets_after = assets * (1 - shock)

equity_after = assets_after - debt

equity_change_pct = (equity_after - equity) / equity

shock_df = pd.DataFrame({

"Shock": shock,

"Assets After": np.round(assets_after, 2),

"Equity After": np.round(equity_after, 2),

"Equity Change Pct": np.round(equity_change_pct, 2)

})

print(shock_df)

# Simple collateral / deleveraging scenario

collateral_value = 800

haircut_before = 0.10

haircut_after = 0.20

borrowing_before = (1 - haircut_before) * collateral_value

borrowing_after = (1 - haircut_after) * collateral_value

funding_gap_from_haircut = borrowing_before - borrowing_after

print("Borrowing before stress:", borrowing_before)

print("Borrowing after stress:", borrowing_after)

print("Funding gap from haircut shock:", funding_gap_from_haircut)

# Short-term funding gap

short_term_liabilities = 250

liquid_assets = 180

funding_gap = short_term_liabilities - liquid_assets

print("Short-term funding gap:", funding_gap)

summary_df = pd.DataFrame({

"Metric": [

"Leverage",

"Debt-to-Equity",

"Borrowing Before Stress",

"Borrowing After Stress",

"Haircut Funding Gap",

"Short-Term Funding Gap"

],

"Value": [

leverage,

de_ratio,

borrowing_before,

borrowing_after,

funding_gap_from_haircut,

funding_gap

]

})

print(summary_df)

This workflow shows how modest asset shocks, tighter collateral conditions, and short-term funding dependence can quickly impair equity and liquidity in leveraged structures. It also demonstrates why leverage is not only a return-enhancing device, but a system-level amplifier.

The full GitHub repository expands this example into institution-level leverage analysis, equity loss amplification, collateral haircut stress, fire-sale spirals, funding-gap analysis, network contagion, household mortgage leverage, macroprudential buffer scoring, sustainability-linked financial shocks, SQL queries, R and Stata replication workflows, Julia simulations, and article-ready figures.

R Workflow: Finance, Leverage, and Systemic Risk

R is useful for systemic-risk summaries, leverage analysis, funding-gap indicators, and publication-ready graphics. The following compact workflow performs the same leverage, asset-shock, collateral, and funding-gap calculations in R.

# Finance, Leverage, and Systemic Risk

# Simple R workflow

# Initial balance sheet

assets <- 1000

debt <- 900

equity <- assets - debt

leverage <- assets / equity

de_ratio <- debt / equity

cat("Initial leverage:", round(leverage, 2), "\n")

cat("Initial debt-to-equity:", round(de_ratio, 2), "\n")

# Asset-price shock scenarios

shock <- c(0.02, 0.05, 0.08, 0.10)

assets_after <- assets * (1 - shock)

equity_after <- assets_after - debt

equity_change_pct <- (equity_after - equity) / equity

shock_df <- data.frame(

Shock = shock,

Assets_After = round(assets_after, 2),

Equity_After = round(equity_after, 2),

Equity_Change_Pct = round(equity_change_pct, 2)

)

print(shock_df)

# Simple collateral / deleveraging scenario

collateral_value <- 800

haircut_before <- 0.10

haircut_after <- 0.20

borrowing_before <- (1 - haircut_before) * collateral_value

borrowing_after <- (1 - haircut_after) * collateral_value

funding_gap_from_haircut <- borrowing_before - borrowing_after

cat("Borrowing before stress:", borrowing_before, "\n")

cat("Borrowing after stress:", borrowing_after, "\n")

cat("Funding gap from haircut shock:", funding_gap_from_haircut, "\n")

# Short-term funding gap

short_term_liabilities <- 250

liquid_assets <- 180

funding_gap <- short_term_liabilities - liquid_assets

cat("Short-term funding gap:", funding_gap, "\n")

summary_df <- data.frame(

Metric = c(

"Leverage",

"Debt-to-Equity",

"Borrowing Before Stress",

"Borrowing After Stress",

"Haircut Funding Gap",

"Short-Term Funding Gap"

),

Value = c(

leverage,

de_ratio,

borrowing_before,

borrowing_after,

funding_gap_from_haircut,

funding_gap

)

)

print(summary_df)

This R workflow is deliberately compact for article readability. In the full repository, R reads structured institution, funding, household, collateral, macroprudential, and sustainability-shock scenarios; calculates leverage, debt-to-equity, capital ratios, funding gaps, household loan-to-value ratios, and macroprudential resilience scores; and visualizes how systemic fragility differs across financial structures.

Future Economic Systems articles can extend this foundation with bank regulatory filings, household mortgage datasets, repo and collateral data, derivatives exposure data, interbank exposure matrices, climate stress-test scenarios, insurance-withdrawal data, and macroprudential policy datasets.

GitHub Repository

The article body includes selected computational examples so the conceptual, institutional, and mathematical argument remains readable. The full repository contains the expanded research infrastructure: Python leverage-amplification simulations, R systemic-risk summaries, Stata applied financial-stability replication workflows, SQL balance-sheet and funding tables, Julia fire-sale and buffer simulations, collateral haircut stress, short-term funding gaps, network contagion, household mortgage leverage, macroprudential buffer scoring, sustainability-linked shock scenarios, documentation, reproducible sample data, and article-ready figures and tables.

Complete Code Repository

The full code distribution for this article, including selected article examples and advanced research-style computational scaffolding for leverage amplification, debt-to-equity ratios, asset-price shocks, collateral haircuts, margin calls, funding gaps, fire-sale spirals, liquidity risk, network contagion, household leverage, macroprudential governance, climate and stranded-asset shocks, systemic resilience, reproducibility documentation, and cross-language economic analysis, is available on GitHub.

Conclusion

Finance, leverage, and systemic risk are central to economic analysis because they show how modern economies convert confidence, collateral, and future expectation into present financial capacity. Leverage makes larger positions possible from smaller equity bases. Financial interconnection allows liquidity and credit to circulate at scale. But these same features also create fragility, because small losses, funding stress, or confidence shocks can be amplified through balance sheets, collateral chains, and network effects.

To understand an economic system seriously, one must therefore ask not only whether finance is supporting investment and exchange, but how risk is layered, who benefits from leverage in expansion, who absorbs losses in contraction, and whether the financial system is organized for resilience or merely for return maximization under the expectation of public rescue.

Systemic risk reveals that finance is never purely private when failure becomes collective. Balance sheets that seem independent in calm conditions may be tied together through funding markets, collateral chains, asset correlations, public backstops, and household vulnerabilities. The social cost of crisis makes financial governance a matter of public responsibility, not merely private technique.

In a sustainable economic system, leverage must be governed by the future it helps build. Finance should support durable productive capacity, ecological transition, public infrastructure, household stability, and resilience under uncertainty. When it instead multiplies claims on fragile foundations, it does not merely increase risk. It reorganizes the economy around the possibility of crisis.

Related Reading

- Economic Systems

- Money, Banking, Credit, and Financial Intermediation

- Information, Uncertainty, and Imperfect Markets

- Capital, Investment, and the Dynamics of Accumulation

- Externalities, Public Goods, and Collective Provision

- Public Finance, State Capacity, and Collective Goods

- Risk & Resilience

- Sustainable Development

Further Reading

- Bank for International Settlements (BIS) (n.d.). Financial Stability. Available at: https://www.bis.org/

- Bank of England (n.d.). Financial Stability. Available at: https://www.bankofengland.co.uk/financial-stability

- European Systemic Risk Board (ESRB) (n.d.). Macroprudential Policy and Systemic Risk. Available at: https://www.esrb.europa.eu/home/html/index.en.html

- Financial Stability Board (FSB) (n.d.). Financial Stability Board. Available at: https://www.fsb.org/

- International Monetary Fund (IMF) (n.d.). Financial Stability. Available at: https://www.imf.org/en/Topics/financial-stability

- International Monetary Fund (IMF) (n.d.). Global Financial Stability Report. Available at: https://www.imf.org/en/Publications/GFSR

- World Bank (n.d.). Financial Sector. Available at: https://www.worldbank.org/en/topic/financialsector

References

- Bank for International Settlements (BIS) (n.d.). Financial Stability. Available at: https://www.bis.org/

- Bank of England (n.d.). Financial Stability. Available at: https://www.bankofengland.co.uk/financial-stability

- European Systemic Risk Board (ESRB) (n.d.). Macroprudential Policy and Systemic Risk. Available at: https://www.esrb.europa.eu/home/html/index.en.html

- Financial Stability Board (FSB) (n.d.). Financial Stability Board. Available at: https://www.fsb.org/

- International Monetary Fund (IMF) (n.d.). Financial Stability. Available at: https://www.imf.org/en/Topics/financial-stability

- World Bank (n.d.). Financial Sector. Available at: https://www.worldbank.org/en/topic/financialsector