Last Updated May 9, 2026

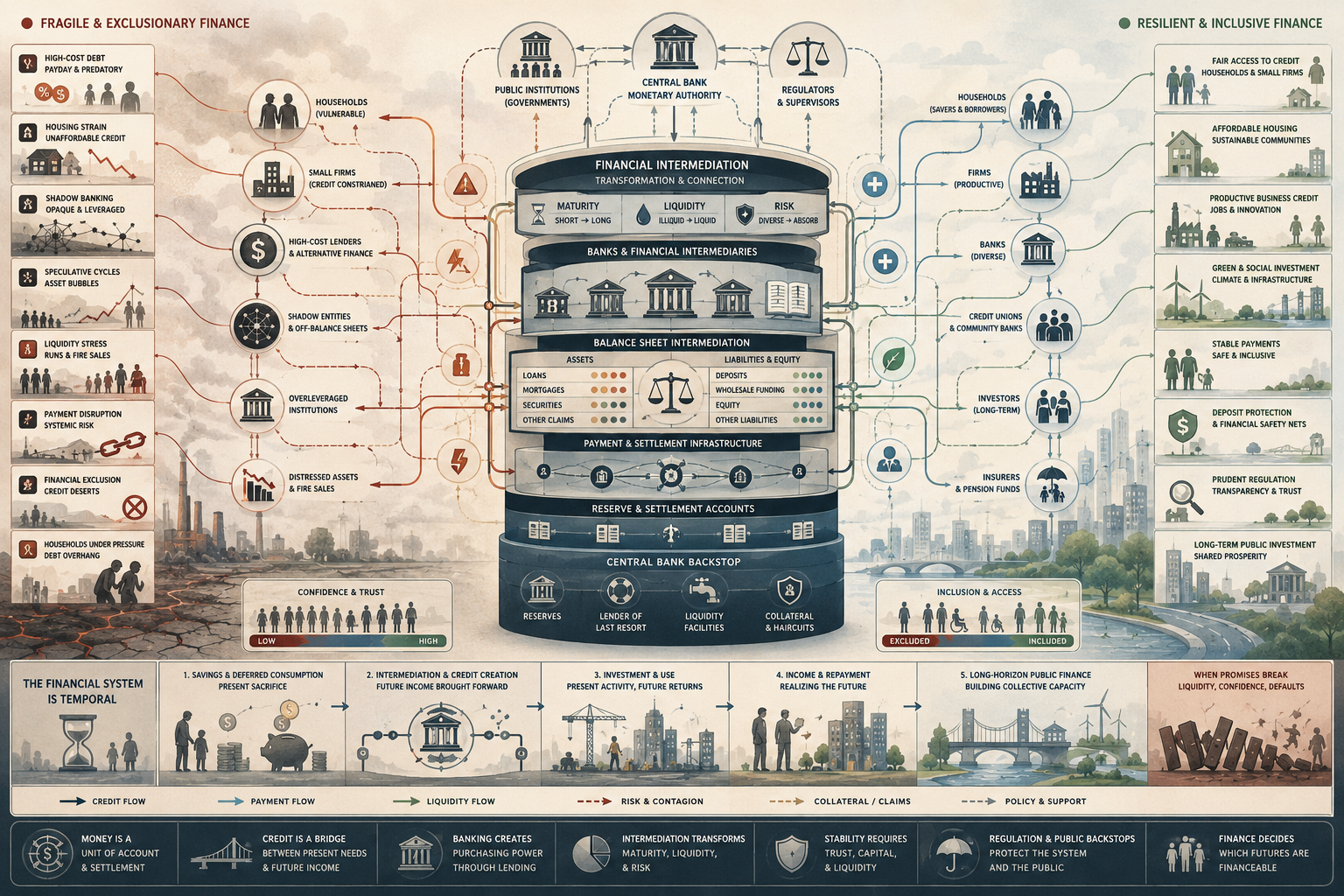

Money, banking, credit, and financial intermediation are central to economic analysis because they shape how modern economies organize promises across time, uncertainty, and scale. Money allows prices, wages, taxes, debts, contracts, and public obligations to be denominated in a common unit. Banking organizes deposits, payments, liquidity, and the creation of credit. Credit permits present spending, investment, housing, survival, and public stabilization to be linked to future income. Financial intermediation channels funds and claims among households, firms, savers, borrowers, investors, governments, and financial institutions while transforming maturity, liquidity, and risk.

Taken together, these institutions make large-scale economic coordination possible. They allow firms to hire before revenue arrives, households to purchase homes before lifetime income has been earned, governments to stabilize crises before taxes are fully collected, and societies to finance long-horizon infrastructure before all benefits are realized. But they also introduce fragility, hierarchy, opacity, leverage, crisis risk, and unequal access to future possibility. A financial system can support development, resilience, and public investment; it can also amplify speculation, debt stress, asset inflation, exclusion, and systemic instability.

Money is never just a neutral technical device. It is a social institution backed by law, trust, state authority, banking systems, payment infrastructure, and expectations about value and settlement. Banking is never merely passive storage of savings. In modern systems, banks help create purchasing power through lending, structure access to liquidity, and stand at the center of payments, maturity transformation, and credit allocation. Credit is not only a convenience. It is one of the principal mechanisms through which households smooth consumption, firms finance investment, governments manage shocks, and financial systems expand claims on the future.

Main Library

Publications

Article Map

Economic Systems

Related Topic

Sustainable Development

Related Topic

Institutions & Governance

Related Topic

Risk & Resilience

Within a sustainable systems framework, money, banking, credit, and intermediation must be evaluated not only in relation to growth and efficiency, but also in relation to resilience, inclusion, long-horizon investment, ecological transition, public capacity, and the governance of systemic risk. A financial system may appear deep and sophisticated while underfunding maintenance, excluding vulnerable households, amplifying speculation, and directing credit away from socially necessary transformation. The serious study of finance must therefore ask not only whether credit expands, but what kinds of futures it finances, whose risks it protects, and whether the monetary architecture of the economy supports durable collective life.

Why This Topic Matters

Money, banking, credit, and financial intermediation matter because modern economies run on promises. Firms hire before revenue arrives. Households consume before all income is received. Governments spend before taxes are fully collected. Investment requires resources now in exchange for uncertain returns later. These temporal gaps are bridged through monetary and financial institutions that make claims transferable, payments reliable, and future income usable in the present.

This matters analytically because a barter-like view of exchange cannot explain modern capitalism, modern public finance, modern crisis management, or modern household life. Economies do not merely swap finished goods. They operate through layered balance sheets, debt contracts, deposit systems, collateral structures, public guarantees, central-bank facilities, liquidity backstops, and payment infrastructures. The financial system is therefore not an external wrapper around the “real” economy. It is one of the main infrastructures through which production, investment, distribution, and public authority are organized.

These issues also matter politically. Access to money and credit is structured unequally. Some actors can borrow at low cost against valuable collateral, while others face punitive terms, exclusion, overdraft fees, predatory products, or unstable access to basic banking. Some institutions receive public support in crisis because their liabilities are systemically important, while households may be left to bear financial stress privately. Monetary and financial systems therefore help determine whose promises are credible, whose risks are socialized, and whose futures are regarded as financeable.

At a deeper level, the study of finance reveals how confidence and coercion coexist in economic order. Monetary systems depend on trust, but they are also backed by law, taxation, enforcement, deposit protection, central banking, and institutional hierarchy. The durability of money and banking is inseparable from the governance structures that make financial claims believable, enforceable, and acceptable in settlement.

Finance also reorganizes social time. Borrowing brings the future into the present. Saving defers present use into later security. Insurance pools uncertainty across populations and time. Public debt allows collective capacity to be mobilized before all fiscal resources are collected. Monetary and banking systems are therefore not merely transactional devices. They are temporal architectures through which societies distribute risk, obligation, liquidity, and access to possibility.

What Money Is

Money is best understood not simply as coins, paper notes, or digits in an account, but as a socially accepted means of denominating, settling, and storing claims. It is the unit in which prices, wages, taxes, debts, profits, budgets, and contracts are expressed. It is what allows different goods, services, obligations, and rights to be made comparable within a shared monetary language.

This matters because money is not valuable only for its material form. In modern economies, much money is not commodity money, and much of it exists as bank deposits rather than cash. What matters is not physical substance but institutional credibility: whether a claim will be accepted in payment, whether it can settle debt, whether the legal system recognizes it, and whether the banking and payment infrastructure will honor it as reliable.

Money is therefore a legal and institutional fact as much as an economic one. States define units of account, impose tax obligations in their currency, regulate banking systems, authorize central-bank liabilities, and support payment architectures that stabilize money’s acceptability. A serious account of money must therefore begin with institutions rather than with the illusion that money is simply a neutral object circulating independently of law and power.

Money also has a temporal meaning. It stores command over future purchase and future settlement, though imperfectly. Inflation, instability, currency hierarchy, capital flight, financial crisis, and sovereign stress all remind us that the value of money depends on continued trust in the institutions and expectations that sustain it.

Money is relational. It exists because a community, a state, and a network of institutions recognize some claims as final enough for settlement. The monetary question is not only “what object circulates?” but “what claim is accepted, by whom, under what authority, and within what hierarchy of safety?”

Functions of Money

Money is commonly described as serving three core functions: medium of exchange, unit of account, and store of value. As a medium of exchange, it avoids the coordination limits of barter by providing a generally accepted means of payment. As a unit of account, it provides the common measure through which prices, wages, debts, taxes, and contracts can be compared. As a store of value, it allows purchasing power to be carried across time, though never perfectly.

These functions matter because they show why money is foundational to complex economies. Without a shared unit of account, long supply chains, tax systems, wage contracts, credit arrangements, public budgets, and financial statements become far harder to coordinate. Without a reliable means of payment, exchange becomes fragile. Without some capacity to store value, intertemporal planning becomes more difficult and uncertain.

But these functions are not always equally secure. In high inflation, money may remain a unit of account while weakening as a store of value. In crisis, assets that seemed liquid may cease to function smoothly as means of payment. In unstable financial systems, trust in money-like claims can fragment. Monetary stability is therefore not a natural equilibrium. It is an institutional achievement.

The unit-of-account function is especially important because it often receives less attention than exchange. Prices, taxes, debts, profits, balance sheets, and public budgets all depend on a stable monetary language. The social coordination enabled by money begins not only in payment, but in calculability itself.

Money also functions as a standard of deferred payment. Long-term contracts, mortgages, bonds, leases, pensions, insurance policies, and public debt all depend on the ability to write present obligations against a future monetary standard. This makes monetary stability central not only to exchange, but to the durability of intertemporal obligation.

Banking as a Monetary Institution

Banks are often described as intermediaries that take deposits from savers and lend them to borrowers. That description captures part of what they do, but it is incomplete. In modern monetary systems, banks are also monetary institutions that create deposit money through lending, operate the payments system, manage liquidity, and connect private balance sheets to central-bank backstops, deposit insurance, and public guarantees.

This matters because banks do not simply move preexisting funds around. When banks extend loans, they typically create matching deposits, expanding money-like purchasing power inside the economy. This makes banking central not only to allocation, but to monetary creation itself. Credit is therefore not a secondary addition to money. It is one of the primary channels through which money is generated in modern systems.

Banking is also structurally fragile because banks borrow short and lend long. Depositors may want access to funds on demand, while loans and investments are often long-duration and illiquid. This maturity mismatch makes banks useful, but also vulnerable to runs, confidence shocks, and liquidity crises. The banking system is a crucial site where monetary convenience and financial fragility are joined together.

For this reason, banks cannot be understood as ordinary firms alone. They are hybrid institutions: privately managed in many cases, publicly supported in crisis, systemically connected through payments, and deeply dependent on regulation, lender-of-last-resort capacity, deposit protection, and trust.

Banking is therefore a governance problem as much as a business model. Who is allowed to issue deposit-like claims, under what supervision, against what assets, with what capital, with what liquidity, and with what access to public support are among the defining questions of the monetary order.

Credit and the Creation of Purchasing Power

Credit is the promise of future payment made usable in the present. It allows actors to spend, invest, smooth income, or survive temporary shortfalls before corresponding revenues are realized. This makes credit essential to modern life. Housing, education, business expansion, infrastructure, working capital, public crisis management, and everyday household survival all depend heavily on credit.

Credit expands demand and productive possibility, but it also creates future obligation. Borrowing can support investment, but it can also burden households, firms, or public institutions with rigid commitments that become dangerous under stress. Credit therefore creates both capability and vulnerability. It brings future income into the present while binding present actors to future payment schedules that may or may not remain manageable.

Credit creation has macroeconomic importance. When lending expands, purchasing power rises, asset prices may increase, and investment can accelerate. When lending contracts, spending can fall sharply and distress can spread even if productive capacity still exists physically. Credit cycles are central to understanding booms, slowdowns, recessions, financial crises, and recoveries.

A serious analysis must therefore ask not only how much credit exists, but what it finances, on what terms, through which institutions, against what collateral, and with what implications for stability, inequality, and long-run development.

Credit also reveals a hierarchy of social confidence. Some borrowers can transform expected future income into cheap present financing with little difficulty. Others face rationing, punitive pricing, or total exclusion. The social meaning of credit lies not only in aggregate volume, but in the structure of whose future counts as bankable.

Financial Intermediation and Maturity Transformation

Financial intermediation refers to the process through which specialized institutions channel funds and claims among actors with different time horizons, risk tolerances, liquidity needs, and balance-sheet positions. Banks, funds, insurers, pension systems, development banks, bond markets, securitization structures, and other intermediaries link savers, investors, households, firms, and governments in ways that would be difficult to organize through direct matching alone.

Intermediation does more than transfer money. It transforms claims. Short-term liabilities may fund long-term assets. Illiquid projects may be financed by instruments that appear liquid to their holders. Risk may be pooled, priced, sliced, insured, shifted, or obscured. Financial systems are therefore transformation systems, not simple pipelines.

Maturity transformation sits at the heart of this process. Depositors or investors often want short-term access and safety, while borrowers often need long-term commitments. Intermediaries bridge that gap, but in doing so they create structural fragility if too many short-term claimants demand liquidity at once. Much of modern financial instability begins in the tension between liquidity promised and illiquidity held.

Financial intermediation is socially valuable precisely because it solves temporal coordination problems that households, firms, and public institutions cannot solve alone. But it is also one of the main ways risk becomes opaque, layered, and systemically amplified.

The crucial issue is not whether intermediation exists, but under what forms of oversight, capitalization, collateral practice, liquidity support, and public backstop it operates. Transformation without governance can turn coordination gains into systemic vulnerability.

Liquidity, Trust, and Payment Systems

Liquidity is the capacity to meet obligations as they fall due without intolerable loss. In practice, liquidity means access to money or money-like instruments that others will accept immediately in settlement. Payment systems operationalize this by allowing transfers among accounts, firms, households, governments, banks, and financial institutions to clear reliably.

Liquidity is the daily reality of monetary order. A balance-sheet position that appears solvent over time may still fail if near-term obligations cannot be met. Households, firms, governments, and banks can all face crisis when payment timing breaks down. Financial order therefore depends not only on long-run asset values, but on whether claims are liquid enough to function in time-sensitive networks of obligation.

Trust is central here. Deposits work as money because people believe they can access them. Interbank markets function because institutions believe settlement will occur. Payment systems clear because participants trust the legal, operational, and central-bank architecture around them. When trust breaks, liquidity can evaporate quickly. Claims that looked safe can become suspect, and the demand for the safest instruments can intensify into panic.

This is why payment infrastructure is fundamental public-economic infrastructure. It is easy to overlook when it functions smoothly, but it is one of the principal reasons monetary economies can coordinate enormous volumes of exchange without constant disruption.

Liquidity is therefore political as well as technical. Who receives emergency liquidity, which instruments are treated as near-money, which payment obligations are prioritized in stress, and which institutions stand close to the lender of last resort all reveal the underlying hierarchy of the financial system.

Central Banks, State Money, and Monetary Governance

Central banks occupy a distinctive role because they stand near the center of the monetary hierarchy. They issue reserves, support settlement among banks, act as lenders of last resort under certain conditions, and help shape liquidity and credit conditions through monetary policy and supervisory frameworks. They do not mechanically control all money, but they are crucial to the governance of the monetary system.

Modern money is deeply entangled with state authority. Tax systems, legal tender regimes, banking regulation, sovereign debt markets, deposit guarantees, central-bank liabilities, and payment architectures all help determine what counts as money-like, what will be accepted in settlement, and which liabilities are most credible. The monetary system is therefore not a purely private spontaneous order. It is a layered public-private architecture with the state near its core.

Central banks also reveal the difference between solvency and liquidity. Institutions that are solvent in the long run may still collapse without timely liquidity support. Lender-of-last-resort action exists because the payments and credit system can fail catastrophically even when not all underlying assets are worthless. Monetary governance is partly about preventing panic from becoming system breakdown.

At the same time, central banks are not neutral technicians outside politics. Their mandates, tools, priorities, and crisis interventions have distributive effects. They influence employment, asset prices, borrowing costs, bank stability, credit conditions, and the boundary between public support and private risk-taking. The governance of money is inseparable from political economy.

Central banks mediate between the short horizon of market stress and the longer horizon of systemic continuity. Their importance lies not only in rate-setting, but in preserving the conditions under which the monetary system can continue to function as a credible architecture of settlement and liquidity.

Interest Rates, Credit Allocation, and Macroeconomic Conditions

Interest rates are often treated as the “price of money,” but they are better understood as prices for time, liquidity, and risk under institutional conditions. They influence borrowing, saving, asset valuation, investment planning, bank profitability, debt-service burdens, exchange rates, and macroeconomic conditions throughout the economy.

The effect of interest rates is not uniform. Lower rates may stimulate borrowing and asset demand, but the distribution of that effect depends on who has access to credit and what assets are financed. Higher rates may restrain inflationary pressure, but they can also suppress productive investment, worsen debt burdens, and strengthen financial claims over wage claims. The macroeconomic meaning of rates depends on the structure of the economy they act upon.

Credit allocation matters just as much as the aggregate level of credit. An economy can have abundant liquidity while directing it toward property speculation, leveraged finance, or asset trading rather than housing affordability, industrial upgrading, public infrastructure, or ecological transition. Monetary conditions alone do not determine developmental outcome; allocation institutions do.

For this reason, serious analysis of finance must move beyond the simple question of whether credit is expanding or contracting. It must ask where the credit goes, on what terms, for whose benefit, against what collateral, and with what long-run systemic consequences.

Interest-rate policy operates inside a wider institutional ecology. It can influence financial conditions broadly, but it cannot by itself guarantee that funding reaches socially productive rather than merely financially profitable uses. Credit governance, banking structure, public investment, development finance, prudential regulation, and fiscal policy all shape the real effect of monetary conditions.

Households, Firms, and Governments in Credit Systems

Households, firms, and governments inhabit credit systems differently. Households borrow for housing, education, consumption smoothing, emergencies, vehicles, medical costs, and sometimes survival. Firms borrow for investment, working capital, merger activity, liquidity management, shareholder payouts, and expansion. Governments issue debt to finance public spending, stabilize downturns, build infrastructure, and manage shocks that would overwhelm private balance sheets.

Debt has different meanings across sectors. Household debt can support stability or deepen vulnerability depending on wages, rates, asset prices, labor security, and legal protections. Firm debt can fund productivity-enhancing investment or leverage-driven extraction. Public debt can underwrite long-horizon public value or become politically constrained by institutional rules and financial-market expectations. Treating all debt as morally or economically identical obscures these differences.

The sectors are also interconnected. Household mortgage booms affect bank balance sheets and property markets. Corporate leverage affects employment and investment. Sovereign debt conditions shape public capacity and central-bank room for maneuver. Finance is a network of linked balance sheets rather than a set of isolated borrowers acting independently.

A research-grade analysis must therefore interpret debt contextually: by sector, maturity, currency, collateral structure, income stream, systemic role, and public purpose. Only then does it become possible to distinguish productive leverage from destabilizing fragility.

Debt should be judged less by abstract moral language than by institutional function. The relevant question is not simply whether borrowing occurs, but whether the resulting obligations are structured in ways compatible with dignity, resilience, developmental purpose, and democratic capacity.

Financial Instability, Leverage, and Crisis

Financial systems are inherently vulnerable to instability because they build present commitments on expectations about future payment under conditions of uncertainty. Leverage magnifies this vulnerability. When actors borrow heavily against asset values or future cash flows, small shifts in rates, prices, collateral quality, funding conditions, or confidence can trigger forced sales, refinancing stress, and cascade effects across institutions.

Crises often arise endogenously rather than from purely external shocks. Long periods of apparent calm can encourage more leverage, looser standards, risk compression, and complacency. The system becomes fragile precisely because it appears stable. When confidence finally breaks, what had seemed liquid and safe can become hard to price or impossible to roll over.

Banking crises, credit crunches, sovereign stress, market panics, and liquidity freezes all reveal that finance is not merely a passive reflection of the underlying economy. It can amplify cycles, redistribute losses violently, and reshape the macroeconomic path of production and employment. The costs of instability are social as well as financial.

For this reason, resilience in finance requires more than efficiency in normal times. It requires capital buffers, liquidity rules, supervisory capacity, credible backstops, resolution frameworks, simple products where possible, and institutional awareness that the search for yield can quietly accumulate systemic danger.

Financial crisis is not only a failure of private judgment. It is often a failure of governance, measurement, and political willingness to constrain unstable forms of leverage before the social cost of collapse becomes intolerable.

Inequality, Financial Access, and Structured Exclusion

Access to money and credit is structured by income, wealth, legal status, collateral, geography, race, gender, documentation, disability, digital access, and institutional trust. Some actors are welcomed into finance as low-risk clients with favorable terms. Others encounter exclusion, high fees, predatory products, thin safety margins, or the absence of formal financial access. This makes finance a powerful mechanism of inclusion for some and extraction for others.

Unequal financial access shapes life chances. Affordable credit can help households buy housing, smooth shocks, build enterprise, or invest in education. High-cost debt can trap households in chronic instability. Unequal access to payments infrastructure, savings vehicles, insurance, and formal banking also affects resilience during crisis. Financial inclusion, however, should not be confused with mere entry into debt markets; the quality and fairness of access matter enormously.

Financial systems can reproduce inequality even while appearing universal. Fees, minimum balances, underwriting models, credit scoring, collateral rules, geographic branch patterns, and digital barriers may all sort populations into sharply different monetary realities. The system is unified formally, but stratified in practice.

A serious account of money and banking must therefore ask whose balance sheets are protected, whose payment problems become emergencies, and whose futures are made expensive because credible financial inclusion remains institutionally uneven.

Structured exclusion also changes the macroeconomy. When large parts of the population face unstable, costly, or extractive financial conditions, consumption smoothing weakens, entrepreneurial possibility narrows, and resilience to shock deteriorates. Financial inequality is therefore also a developmental constraint.

Shadow Banking, Market-Based Finance, and Opacity

Not all money-like and credit-like activity occurs inside traditional banks. Modern financial systems include money-market funds, securitization chains, repo markets, structured investment vehicles, asset managers, private credit, hedge funds, nonbank mortgage lenders, and other forms of market-based finance that perform bank-like functions without always being regulated like banks. These arrangements are often grouped under the broad label of shadow banking.

Shadow banking extends maturity transformation, liquidity creation, and leverage into institutions and instruments that may look safer or more diversified than they actually are. In good times, these structures can appear efficient and innovative. In stress, they can reveal hidden dependencies on collateral quality, market liquidity, short-term funding, and public backstops.

Opacity is central here. Risk can be sliced, repackaged, and relocated in ways that make local positions look manageable while worsening system-wide uncertainty. Financial intermediation then becomes harder to monitor and harder to govern, even as it remains deeply connected to the banking core through funding markets, guarantees, and crisis contagion.

For this reason, the study of money and finance must move beyond chartered banks alone. The monetary system includes a wider hierarchy of near-money claims, liquidity promises, collateral practices, and contingent public support that often become visible only under stress.

Shadow banking illustrates a broader principle: finance often migrates toward forms that preserve profitability or flexibility while escaping the full discipline of prudential oversight. The system remains interconnected even when the legal labels change.

Monetary Hierarchy, Collateral, and the Structure of Safety

Not all money-like claims are equally safe. At the top of the hierarchy sit the highest-quality settlement instruments, such as central-bank money and the most trusted sovereign liabilities. Below them are commercial-bank deposits, then a wider range of short-term private claims, asset-backed liabilities, repo claims, money-market instruments, and other near-money instruments whose acceptability depends more heavily on market conditions, collateral quality, and confidence.

This matters because monetary systems are stratified. What appears as “money” from one vantage point may be a contingent claim from another. Some actors operate close to the safest layers of the hierarchy, with access to reserves, central-bank facilities, deposit insurance, and high-quality collateral. Others depend on weaker instruments, less secure funding, or payment channels that become fragile under stress.

Collateral is central to this structure of safety. Assets used to secure borrowing or liquidity access determine who can obtain funding cheaply and who cannot. In this sense, the monetary order is also an order of recognized asset quality. The distribution of collateralizable wealth shapes who has privileged access to credible liquidity and whose obligations remain expensive or insecure.

A research-grade treatment of finance must therefore see monetary hierarchy as a form of institutional ranking. It orders claims by safety, liquidity, legal recognition, collateral acceptance, and public support. In doing so, it also orders economic actors by proximity to protected forms of money.

Monetary hierarchy is not only a technical feature of finance. It is one of the ways social and institutional power becomes embedded in the architecture of payment and credit.

Credit, Time, and the Politics of Obligation

Credit reorganizes time by pulling expected future income into present action. But it also reorganizes authority. Borrowers commit future labor, revenue, or tax capacity to repayment schedules that can become disciplinary structures in everyday life. Household debt shapes consumption and life planning. Corporate debt shapes employment strategy and payout decisions. Public debt shapes fiscal space and political conflict over austerity, taxation, and investment.

Obligation is not evenly experienced. The ability to delay payment, refinance, restructure, obtain relief, or receive public support is distributed unequally. Some debtors are treated as systemically important and rescued. Others are disciplined through penalties, default, extraction, or social stigma. Credit is therefore not only an economic instrument. It is one of the main ways future time is socially governed.

From this perspective, finance is also about who is allowed to remain liquid, who must absorb shock personally, and whose obligations are treated as negotiable versus inviolable. The politics of credit lies partly in these asymmetries of forgiveness, enforcement, and rollover.

A serious analysis of financial intermediation must therefore include the moral and political dimensions of debt. Obligation is not merely priced; it is institutionalized through regimes of enforcement, relief, priority, restructuring, bankruptcy, austerity, and public support that help define the social meaning of economic citizenship.

Credit can support freedom when it expands capability under fair terms. It can become domination when it converts vulnerability into permanent extraction. The difference is institutional.

Money, Banking, and Sustainable Systems

Within sustainable systems, monetary and financial institutions must be evaluated in relation to resilience, social need, and ecological transition rather than credit expansion alone. A financial system can be liquid, profitable, and sophisticated while directing resources toward speculative property cycles, fossil-intensive infrastructure, fragile supply chains, and asset-price inflation that leaves housing, care, public health, maintenance, and public goods underfunded.

This changes the meaning of good finance. The question is not only whether finance supports growth, but whether it supports the kinds of investment that preserve long-term collective capability. Grid resilience, ecological restoration, public transit, health systems, maintenance, affordable housing, water infrastructure, education, and adaptation all require financing structures that are patient, coordinated, and publicly accountable in ways narrow private return metrics may not sustain.

Sustainable systems require monetary and credit architectures that can absorb uncertainty, direct capital toward long-horizon public value, and prevent systemic risk from overwhelming social capacity. This often implies a greater role for public development finance, prudential governance, stress testing, green and resilience-oriented credit allocation, and institutional designs that distinguish socially useful leverage from destabilizing financial expansion.

Banking is not merely about moving money. It is about deciding which futures become financeable, which forms of resilience are treated as worthy of investment, and whether the monetary system reinforces extraction or supports durable collective life.

Transition policy is inseparable from financial architecture. A society cannot decarbonize, adapt, maintain infrastructure, and widen resilience at scale unless its monetary and banking institutions can sustain the required commitments across long horizons, uncertain returns, and uneven private incentives.

Accounting, Balance Sheets, and the Visibility of Finance

Money and finance are also problems of accounting. Balance sheets record assets, liabilities, equity, liquidity positions, and contingent claims through which financial reality becomes legible to institutions, regulators, investors, and markets. Yet what is visible in accounting is not identical to what is socially important. Some risks remain off-balance-sheet, some interdependencies are hidden in structure, and some vulnerabilities only appear once market conditions change.

Accounting is one of the main ways financial systems know themselves. Banking is built on double-entry logic, payment settlement, reserve management, and the reconciliation of claims. But measurement systems can stabilize appearance while concealing fragility. A well-capitalized institution on paper may still be liquidity-vulnerable. A solvent portfolio under one pricing regime may become unstable under another. A narrow focus on private accounting values may also ignore ecological and social exposures that matter for long-run viability.

A research-grade treatment must therefore connect accounting to governance. What gets measured, disclosed, provisioned, and stress-tested shapes how financial institutions behave. The visibility of finance is itself an institutional achievement, and its blind spots are often where crisis incubates.

Accounting categories also help define what counts as prudence. Provisioning rules, capital treatment, impairment recognition, valuation methods, and liquidity classification all influence whether institutions appear healthy enough to continue expanding claims. Financial stability therefore depends partly on how reality is rendered legible before breakdown makes hidden weakness undeniable.

Balance sheets are not merely records. They are maps of promise, obligation, safety, hierarchy, and vulnerability. A society that cannot read its balance sheets clearly cannot govern its financial future responsibly.

How Financial Systems Should Be Judged

Money, banking, credit, and financial intermediation should not be judged only by liquidity, profitability, financial depth, or credit expansion. A broader economic systems framework asks whether financial architecture supports resilience, inclusion, public capacity, productive investment, fair access, and long-run social and ecological stability.

| Dimension | Narrow Question | Systems Question |

|---|---|---|

| Money | Is money accepted in exchange? | Is the monetary system trustworthy, inclusive, stable, and capable of settling obligations fairly? |

| Banking | Do banks make loans? | Are banks creating credit under conditions that preserve liquidity, solvency, public trust, and productive purpose? |

| Credit | Is credit expanding? | What does credit finance, who receives it, on what terms, and with what future burden? |

| Liquidity | Can claims be converted to cash? | Can institutions meet obligations under stress without triggering systemic harm? |

| Leverage | Does leverage raise returns? | Does leverage magnify fragility, socialized losses, and crisis risk? |

| Access | Can households enter the financial system? | Is financial access fair, affordable, non-extractive, and stabilizing for vulnerable communities? |

| Intermediation | Are funds channeled efficiently? | Does intermediation direct resources toward productive capacity, resilience, public goods, and ecological transition? |

| Sustainability | Does finance support growth? | Does finance support long-horizon investment, maintenance, decarbonization, adaptation, and durable collective life? |

This framework prevents a common mistake: treating financial sophistication as evidence of financial adequacy. A system can be liquid, complex, and profitable while remaining exclusionary, speculative, fragile, or misaligned with long-run social need. The central question is therefore not simply whether finance expands. The deeper question is whether financial expansion serves durable public purpose.

A good financial system should make productive and socially necessary futures financeable while limiting the forms of leverage, opacity, and extraction that convert private gain into public vulnerability.

Mathematical Lens

Mathematics can clarify money, banking, credit, and financial intermediation by making balance-sheet relationships, liquidity constraints, leverage, and debt-service capacity explicit. These equations do not determine how finance should be governed, but they help reveal the structure of monetary and financial fragility.

1. Money Supply Identity

M = C + D

\]

Interpretation: A simple money measure \(M\) includes currency in circulation \(C\) and deposit money \(D\). This helps make clear that modern money is not only cash. Deposit liabilities of banks are central to the monetary system.

2. Bank Balance-Sheet Expansion Through Lending

\Delta Assets = +Loan

\]

Interpretation: When a bank makes a loan, it records a new asset: the borrower’s obligation to repay.

\Delta Liabilities = +Deposit

\]

Interpretation: The loan also creates a matching deposit liability. This stylized balance-sheet logic captures the basic point that bank lending can create deposit money and expand purchasing power inside the economy.

3. Leverage Ratio

Leverage = \frac{A}{E}

\]

Interpretation: Leverage equals total assets \(A\) divided by equity \(E\). Higher leverage can magnify returns in good times, but it also increases fragility under adverse asset-price, credit-loss, or liquidity shocks.

4. Loan-to-Deposit Ratio

LDR = \frac{Loans}{Deposits}

\]

Interpretation: The loan-to-deposit ratio \(LDR\) gives a rough sense of how far lending is funded by deposit liabilities, though it does not by itself capture broader funding structure, wholesale funding dependence, or market-based finance exposure.

5. Interest Coverage for Debt Service

ICR = \frac{EBIT}{Interest}

\]

Interpretation: The interest coverage ratio \(ICR\) compares earnings before interest and taxes \(EBIT\) with interest payments. It helps show whether an income stream can support debt obligations, though real analysis would also consider maturity, refinancing risk, currency exposure, and cash-flow volatility.

6. Credit-Money Link

\Delta Y = f(\Delta Credit, Confidence, Rates, Balance\ Sheets)

\]

Interpretation: Changes in output \(\Delta Y\) may depend significantly on the expansion or contraction of credit, mediated by confidence, interest rates, balance-sheet health, and institutional conditions.

7. Liquidity Coverage Idea

LCR = \frac{HQLA}{NCO}

\]

Interpretation: Liquidity coverage \(LCR\) compares high-quality liquid assets \(HQLA\) with net cash outflows \(NCO\) over a stress horizon. This formalizes the principle that institutions promising short-term liquidity need sufficient genuinely safe and usable assets to survive funding stress.

8. Practical Interpretation

The mathematical lens clarifies several structural points. Modern money includes both currency and deposit claims. Bank lending can expand purchasing power through deposit creation. Leverage magnifies both gains and fragility. Funding structure affects banking stability. Debt sustainability depends on income relative to servicing burden. Credit dynamics strongly influence macroeconomic conditions. Liquidity resilience depends on access to genuinely safe and usable assets.

Formalization helps reveal balance-sheet logic, but it does not settle how credit should be allocated, which liabilities deserve public support, or what forms of finance are socially desirable. Those remain institutional, ethical, and political questions.

Python Workflow: Money, Banking, and Credit

Python is useful for turning monetary and banking concepts into reproducible balance-sheet analysis. The following compact workflow models a simple money aggregate, bank leverage, loan-to-deposit ratios, debt-service capacity, deposit creation, and liquidity coverage.

# Money, Banking, Credit, and Financial Intermediation

# Simple Python workflow

import numpy as np

import pandas as pd

# Simple money aggregate

currency = 200

deposits = 800

money_supply = currency + deposits

print("Money supply:", money_supply)

# Stylized bank balance sheet

assets = 1000

equity = 100

deposits_bank = 750

loans = 700

leverage = assets / equity

ldr = loans / deposits_bank

print("Leverage ratio:", round(leverage, 2))

print("Loan-to-deposit ratio:", round(ldr, 2))

# Debt-service capacity

ebit = np.array([120, 110, 95, 130])

interest_payment = np.array([30, 30, 30, 30])

icr = ebit / interest_payment

print("Interest coverage ratios:", np.round(icr, 2))

# Stylized loan creation

loan_new = 50

assets_after = assets + loan_new

deposits_after = deposits_bank + loan_new

print("Assets after loan:", assets_after)

print("Deposits after loan:", deposits_after)

# Simple liquidity coverage

hqla = 180

net_cash_outflows = 140

lcr = hqla / net_cash_outflows

print("Liquidity coverage ratio:", round(lcr, 2))

df = pd.DataFrame({

"Metric": [

"Money Supply",

"Leverage",

"Loan-to-Deposit",

"Assets After Loan",

"Deposits After Loan",

"Liquidity Coverage"

],

"Value": [

money_supply,

leverage,

ldr,

assets_after,

deposits_after,

lcr

]

})

print(df)

This workflow makes visible the balance-sheet structure underlying monetary creation, banking stability, debt burden, and short-horizon liquidity resilience. It also shows why banking cannot be treated as simple storage: lending changes both asset and liability structures.

The full GitHub repository expands this example into money-aggregate scenarios, bank balance-sheet indicators, deposit-creation simulations, leverage and capital-ratio analysis, debt-service stress, liquidity-coverage scenarios, credit-allocation scoring, monetary-hierarchy indicators, sustainable-finance scoring, SQL queries, R and Stata replication workflows, Julia simulations, and article-ready figures.

R Workflow: Money, Banking, and Credit

R is useful for banking summaries, liquidity analysis, debt-service indicators, and publication-ready graphics. The following compact workflow performs the same money, banking, leverage, debt-service, and liquidity-coverage calculations in R.

# Money, Banking, Credit, and Financial Intermediation

# Simple R workflow

# Simple money aggregate

currency <- 200

deposits <- 800

money_supply <- currency + deposits

cat("Money supply:", money_supply, "\n")

# Stylized bank balance sheet

assets <- 1000

equity <- 100

deposits_bank <- 750

loans <- 700

leverage <- assets / equity

ldr <- loans / deposits_bank

cat("Leverage ratio:", round(leverage, 2), "\n")

cat("Loan-to-deposit ratio:", round(ldr, 2), "\n")

# Debt-service capacity

EBIT <- c(120, 110, 95, 130)

interest_payment <- c(30, 30, 30, 30)

ICR <- EBIT / interest_payment

cat("Interest coverage ratios:", round(ICR, 2), "\n")

# Stylized loan creation

loan_new <- 50

assets_after <- assets + loan_new

deposits_after <- deposits_bank + loan_new

cat("Assets after loan:", assets_after, "\n")

cat("Deposits after loan:", deposits_after, "\n")

# Simple liquidity coverage

hqla <- 180

net_cash_outflows <- 140

lcr <- hqla / net_cash_outflows

cat("Liquidity coverage ratio:", round(lcr, 2), "\n")

summary_df <- data.frame(

Metric = c(

"Money Supply",

"Leverage",

"Loan-to-Deposit",

"Assets After Loan",

"Deposits After Loan",

"Liquidity Coverage"

),

Value = c(

money_supply,

leverage,

ldr,

assets_after,

deposits_after,

lcr

)

)

print(summary_df)

This R workflow is deliberately compact for article readability. In the full repository, R reads structured money, banking, debt-service, liquidity, credit-allocation, monetary-hierarchy, and sustainable-finance scenarios; calculates money supply, leverage, loan-to-deposit ratios, debt-service stress, liquidity coverage, developmental credit scores, and sustainable-finance scores; and visualizes how financial systems differ across institutional conditions.

Future Economic Systems articles can extend this foundation with central-bank data, bank-call-report data, payment-system data, household debt records, firm financial statements, credit-allocation datasets, regulatory stress-test scenarios, shadow-banking funding structures, and climate-finance indicators.

GitHub Repository

The article body includes selected computational examples so the conceptual, institutional, and mathematical argument remains readable. The full repository contains the expanded research infrastructure: Python money and balance-sheet simulations, R banking indicator summaries, Stata applied financial-economics replication workflows, SQL money and credit tables, Julia liquidity and credit simulations, deposit-creation examples, leverage metrics, debt-service stress, liquidity-coverage indicators, credit-allocation scoring, monetary-hierarchy analysis, sustainable-finance assessment, documentation, reproducible sample data, and article-ready figures and tables.

Complete Code Repository

The full code distribution for this article, including selected article examples and advanced research-style computational scaffolding for money aggregates, bank balance sheets, deposit creation, leverage, loan-to-deposit ratios, interest coverage, liquidity coverage, credit allocation, monetary hierarchy, financial inclusion, sustainable finance, reproducibility documentation, and cross-language economic analysis, is available on GitHub.

Conclusion

Money, banking, credit, and financial intermediation are central to economic analysis because they show how modern economies organize promises across time. Money provides the common unit and settlement medium through which obligations become comparable. Banking creates and manages deposit money while structuring access to liquidity and credit. Financial intermediation transforms risk, maturity, and claims so that present resources can be linked to future production and payment.

These institutions make complex economies possible, but they also create fragility, hierarchy, opacity, leverage, and unequal access to financial possibility. To understand an economic system seriously, one must therefore ask not only how goods are produced and exchanged, but how monetary claims are created, how balance sheets are linked, who can borrow on favorable terms, which risks are publicly backstopped, and whether finance directs credit toward resilient and socially useful futures.

Financial systems are not neutral pipes carrying funds from savers to borrowers. They are institutional architectures that decide whose promises count, whose liquidity is protected, whose obligations are enforced, and which futures become financeable. They can support productive investment, public goods, and ecological transition; they can also amplify speculation, debt stress, exclusion, and crisis.

In a sustainable economic system, finance must be judged by the world it enables. A monetary and banking architecture worthy of public trust should support durable collective life, fair access, resilient payment systems, productive investment, ecological transition, and protection against the forms of leverage and opacity that convert private financial gain into public harm.

Related Reading

- Economic Systems

- Information, Uncertainty, and Imperfect Markets

- Capital, Investment, and the Dynamics of Accumulation

- Labor, Wages, Productivity, and the Social Organization of Work

- Externalities, Public Goods, and Collective Provision

- Public Finance, State Capacity, and Collective Goods

- Risk & Resilience

- Sustainable Development

Further Reading

- Bank for International Settlements (BIS) (n.d.). Banking and financial stability. Available at: https://www.bis.org/

- Bank of England (n.d.). Money and credit. Available at: https://www.bankofengland.co.uk/monetary-policy

- International Monetary Fund (IMF) (n.d.). Monetary Policy. Available at: https://www.imf.org/en/Topics/monetary-policy

- International Monetary Fund (IMF) (n.d.). Financial Sector Assessment Program. Available at: https://www.imf.org/en/Publications/fssa

- Organisation for Economic Co-operation and Development (OECD) (n.d.). Financial markets. Available at: https://www.oecd.org/en/topics/financial-markets.html

- World Bank (n.d.). Financial Sector. Available at: https://www.worldbank.org/en/topic/financialsector

- World Bank (n.d.). Global Financial Development Database. Available at: https://www.worldbank.org/en/publication/gfdr/data/global-financial-development-database

References

- Bank for International Settlements (BIS) (n.d.). Banking and financial stability. Available at: https://www.bis.org/

- Bank of England (n.d.). Money and credit. Available at: https://www.bankofengland.co.uk/monetary-policy

- International Monetary Fund (IMF) (n.d.). Monetary Policy. Available at: https://www.imf.org/en/Topics/monetary-policy

- International Monetary Fund (IMF) (n.d.). Financial Sector Assessment Program. Available at: https://www.imf.org/en/Publications/fssa

- Organisation for Economic Co-operation and Development (OECD) (n.d.). Financial markets. Available at: https://www.oecd.org/en/topics/financial-markets.html

- World Bank (n.d.). Financial Sector. Available at: https://www.worldbank.org/en/topic/financialsector