Last Updated May 25, 2026

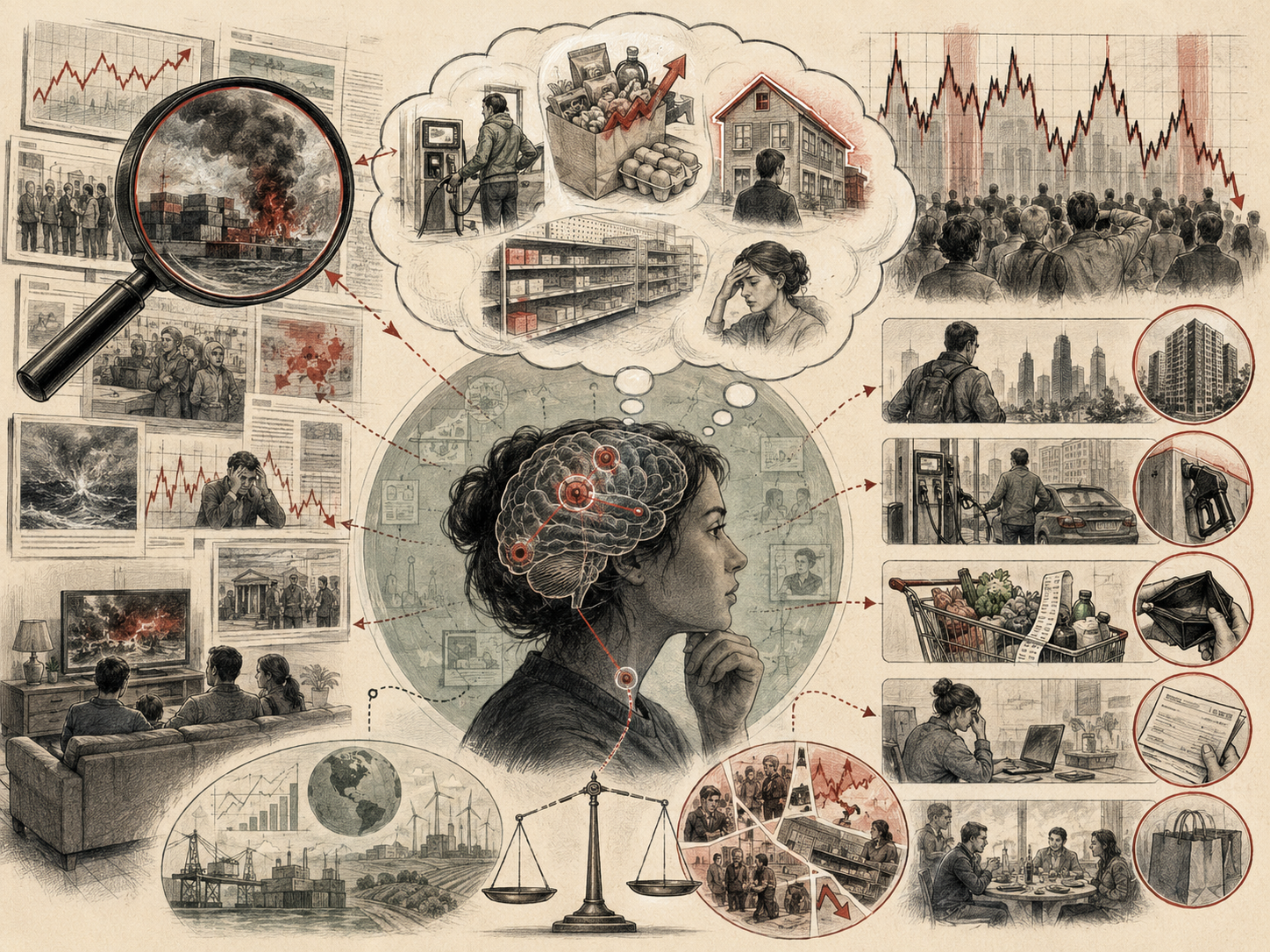

Availability bias refers to the tendency for people to estimate the likelihood, importance, or urgency of events based on how easily examples come to mind. Events that are vivid, recent, emotionally charged, repeatedly discussed, or widely circulated through media often feel more probable than they actually are. Events that are statistically common but less memorable may receive too little attention. In behavioral economics, availability bias helps explain why economic risk perception often diverges from formal probability, long-run evidence, actuarial frequency, or structural analysis.

Availability bias matters because economic judgment is often made under uncertainty. Investors assess market downturns. Households estimate the likelihood of unemployment, inflation, fraud, illness, debt stress, or housing instability. Consumers judge whether a product is risky or trustworthy. Policymakers assess recession risk, technological disruption, public-health threats, climate shocks, financial contagion, and institutional instability. Classical economic models often assume that decision-makers evaluate available information objectively. Behavioral economics shows that people frequently substitute cognitive accessibility for statistical reasoning. What is easiest to remember can become what seems most likely.

Main Library

Publications

Article Map

Behavioral Economics

Related Topic

Economic Systems

Related Topic

Institutions & Governance

Related Topic

Stewardship & Ethics

Availability bias is one of the central heuristics in the behavioral study of judgment under uncertainty. The foundational work of Amos Tversky and Daniel Kahneman showed that people often estimate frequency or probability by the ease with which examples are retrieved from memory. The shortcut can be useful because full probabilistic reasoning is costly, difficult, and often impossible in daily life. But memory accessibility is not the same as statistical frequency. A rare event can seem common if it is dramatic. A common risk can seem negligible if it is ordinary, gradual, or hard to visualize.

This makes availability bias central to Heuristics and Biases in Economic Decision-Making, Bounded Rationality in Economic Decision-Making, Behavioral Finance and Investor Psychology, Framing Effects in Consumer Choice, Anchoring Bias in Economic Judgment, Choice Architecture and Decision Environments, and Behavioral Insights in Environmental Policy. It shows that economic perception is shaped not only by data, but by memory, media, salience, repetition, narrative, and the public architecture of attention.

The Concept of Availability Bias

Availability bias occurs when people treat ease of recall as evidence of frequency, probability, importance, or urgency. If examples of an event come quickly to mind, the event feels more likely. If examples are hard to retrieve, the event feels less likely. The mind substitutes a question that is easier to answer—“Can I think of examples?”—for a question that is harder to answer—“What is the actual probability or base rate?”

This substitution is efficient. In many situations, people lack complete data, formal models, or time for careful analysis. Memory provides a fast signal. A person who recently heard about a bank failure may become more concerned about banking stability. A worker who knows someone recently laid off may become more worried about unemployment. An investor who remembers a market crash may overweight downside risk. A household that sees repeated stories about fraud may overestimate the likelihood of being defrauded while underestimating routine, less dramatic losses such as fees, interest charges, inflation erosion, or underinsurance.

The problem is that memory is not a neutral sample. Events become memorable for many reasons other than frequency: emotional intensity, novelty, repetition, media coverage, personal experience, visual vividness, social discussion, identity relevance, and narrative simplicity. A dramatic event can dominate judgment because it is vivid, while a slow-moving structural risk remains cognitively faint. Availability bias therefore distorts the probability layer of decision-making.

Economic perception is especially vulnerable because many economic risks are abstract. Inflation, compounding debt, retirement insecurity, systemic financial risk, infrastructure fragility, biodiversity loss, and climate risk are difficult to observe directly. They unfold through systems, time, and aggregation. A vivid example—a market crash, a viral fraud story, a wildfire, a bank run, a supply shortage—may therefore become the mental shorthand for an entire category of risk.

Availability bias is not simply ignorance. It is a predictable cognitive response to limited attention and uneven information environments. People often use what is available because broader evidence is difficult to access, difficult to interpret, or less emotionally compelling. This makes availability bias both a psychological concept and an institutional problem.

The Availability Heuristic

The availability heuristic is the mental shortcut underlying availability bias. Rather than calculating probability from base rates or statistical evidence, people estimate likelihood based on the ease with which examples, images, narratives, or experiences come to mind. The heuristic can be useful when memory roughly tracks frequency. If someone has repeatedly experienced delays on a transit route, remembering those delays may be relevant to future planning. If many neighbors report a local hazard, recall may contain useful information.

But the heuristic becomes biased when memory accessibility is driven by factors that do not correspond to statistical probability. A rare risk may be overestimated if it is shocking, visually memorable, or repeatedly reported. A common risk may be underestimated if it is mundane, gradual, or socially normalized. The availability heuristic therefore works best in environments where memory is a reasonably representative sample of reality. It fails in environments where attention is systematically skewed.

Economic life contains many skewed attention environments. News media tend to focus on crises, scandals, sudden losses, unusual events, and conflict. Digital platforms amplify emotionally charged content. Political communication often highlights vivid cases. Financial narratives emphasize winners, crashes, bubbles, collapses, and extraordinary success. Advertising selects memorable images rather than representative evidence. These environments make some risks and opportunities cognitively available while leaving others in the background.

The availability heuristic also interacts with bounded rationality. People cannot track every probability relevant to economic life. They simplify. They rely on memory, experience, social signals, and salient stories. Availability bias is therefore not a failure of intelligence. It is a consequence of human cognition operating under constraints.

The serious question is how institutions should respond. If risk perception is shaped by availability, then better public understanding requires more than data publication. It requires risk communication, evidence design, salience calibration, statistical literacy, trusted institutions, and decision environments that help people compare vivid examples with broader patterns.

Psychological Mechanisms Behind Availability Bias

Availability bias arises through several overlapping mechanisms: recency, vividness, emotional salience, repetition, personal experience, narrative coherence, social transmission, media amplification, and retrieval fluency. These mechanisms determine which examples come to mind most easily and therefore which risks feel most important.

Recency matters because recent events are easier to remember. After a market downturn, investors may become more pessimistic. After a period of rising prices, households may become more sensitive to inflation. After a bank failure, depositors may become more attentive to bank stability. Recency can be informative, but it can also produce overreaction when recent events are treated as more representative than they are.

Vividness matters because concrete images are more memorable than abstract statistics. A single dramatic story about fraud may affect perception more than a table showing the larger financial impact of routine fees. A filmed flood may affect climate concern more than a long-term temperature trend. A visible queue outside a bank may influence perception more than capital-ratio data. Vividness gives examples emotional and cognitive force.

Emotional salience strengthens recall. Fear, anger, shock, grief, hope, pride, and outrage make events easier to retrieve. A frightening loss feels more important because it is emotionally available. A spectacular success story can make opportunity feel more common than it is. Emotional intensity can therefore distort both risk perception and opportunity perception.

Repetition creates familiarity. When an event or narrative is repeated across news, social media, advertising, political speech, and conversation, it becomes easier to recall. Repetition can make a risk feel widespread even when the underlying incidence is limited. It can also make a claim feel plausible because the mind confuses familiarity with evidence.

Personal experience is especially influential. People often weight their own experience more heavily than population-level data. A household that experienced a job loss may overestimate future unemployment risk. An investor who suffered losses in one sector may avoid that sector for years. Personal experience is meaningful, but it is usually a small sample.

Narrative coherence helps events become memorable. A story with a clear villain, victim, cause, and consequence is easier to recall than a diffuse system-level explanation. Economic risks often become publicly powerful when they can be narrated simply. Complex structural risks are harder to make available because they lack a single memorable event.

These mechanisms explain why availability bias is so durable. It is not caused by one error. It arises from the way memory, emotion, media, social communication, and institutional attention shape what the mind can easily retrieve.

Availability Bias in Economic Decision-Making

Availability bias influences economic decision-making whenever people must estimate uncertain outcomes. In financial markets, investors may overestimate the probability of a crash after a recent downturn and underestimate risk during long periods of stability. In consumer finance, households may overreact to vivid fraud stories while underreacting to persistent interest charges, overdraft fees, under-saving, or inadequate insurance. In labor markets, recent layoffs may make unemployment risk feel more widespread than current data suggest.

Availability bias can shape saving and investment behavior. A person who vividly remembers market losses may hold too much cash and miss long-term returns. A person who repeatedly hears stories of speculative success may overinvest in risky assets. A person whose social network is experiencing economic stress may become more pessimistic than broader labor-market indicators justify. These judgments may be understandable, but they can still distort portfolio allocation, retirement planning, and financial resilience.

Insurance demand can move in the same way. After a disaster, people may become more willing to purchase coverage for that specific risk. As time passes and the event becomes less available, demand may fall even if objective risk remains. This creates a problem for disaster preparedness, flood insurance, health risk, cyber risk, and long-term resilience planning. People often insure against what they can imagine rather than what base rates indicate.

Availability bias also affects consumer choice. A product associated with a memorable failure may be avoided even if its objective safety record is strong. A brand associated with a vivid positive story may seem more trustworthy than competitors. A single memorable review may outweigh aggregate evidence. Consumers often use examples as proxies for quality, reliability, or risk.

At the institutional level, availability bias can shape strategic decisions. Organizations may overprepare for the last crisis while underpreparing for less visible risks. Governments may react strongly to dramatic failures while neglecting slow deterioration. Firms may chase highly visible market opportunities while ignoring less glamorous but more durable sources of value. Economic decision-making is therefore affected by what institutions remember, not only by what they know.

Media, Salience, and Economic Risk

One of the most powerful drivers of availability bias is the information environment. Events that receive repeated media coverage become easier to recall and therefore more behaviorally influential. This is especially important for economic risks because most individuals do not observe macroeconomic systems directly. They encounter them through headlines, charts, social media posts, workplace conversation, political messaging, institutional statements, and personal anecdotes.

Media attention does not simply inform risk perception. It structures it. A widely covered bank failure can make financial instability feel immediate. A viral story about fraud can make fraud risk feel pervasive. A dramatic market decline can make recession feel inevitable. A supply shortage can make scarcity feel more general. A visible price spike in a familiar category can shape inflation perception more strongly than broader price-index data.

The problem is not that media coverage is irrelevant. Dramatic events may reveal real risks. The problem is that coverage intensity does not necessarily match statistical frequency, systemic importance, or long-term probability. Media systems tend to reward novelty, conflict, emotion, and urgency. Slow-moving risks receive less attention because they are harder to dramatize. This creates a gap between attention and evidence.

Digital platforms intensify this dynamic. Recommendation systems often reward content that generates engagement. Fear, outrage, novelty, and vivid imagery are highly available in such environments. A person may encounter repeated examples of a rare event and begin to feel surrounded by it. Meanwhile, structural risks that require context and longitudinal evidence may remain less available.

Availability bias therefore links individual cognition to public communication systems. Economic perception is not formed only inside the mind. It is produced through the interaction of memory and media. Institutions that care about informed public judgment must treat attention architecture as part of economic governance.

Availability Bias and Market Dynamics

Availability bias can shape market dynamics when investors, consumers, analysts, or firms collectively overweight salient examples. Financial markets are especially vulnerable because prices depend not only on fundamentals, but on beliefs about future earnings, risk, liquidity, policy, technology, and other participants’ expectations. When salient narratives dominate belief formation, markets can move more sharply than fundamentals alone would predict.

During optimistic periods, vivid stories of rapid growth, technological disruption, extraordinary returns, or market winners can become highly available. Investors may extrapolate from memorable success cases and underweight base rates. This can contribute to speculative enthusiasm, overvaluation, and crowding into popular assets. The availability of success stories makes exceptional outcomes feel more typical than they are.

During downturns, the opposite can occur. Highly memorable losses, bankruptcies, scandals, bank failures, or market crashes may dominate perception. Investors may overestimate downside risk and underweight long-term recovery evidence. Availability bias can therefore contribute to panic, withdrawal, contagion, and excess pessimism. The market becomes governed not only by information, but by which examples are most cognitively accessible.

Availability bias also interacts with herd behavior. When many participants focus on the same salient story, their behavior can reinforce the story’s importance. Rising prices make success narratives more available. Falling prices make crisis narratives more available. Attention, price movement, and social transmission can form feedback loops.

Market professionals are not immune. Analysts, fund managers, executives, and policymakers can also overreact to recent vivid events. Professional training may reduce some errors, but institutional incentives can amplify salience. A recent failure may become the risk everyone must discuss. A successful trend may become the opportunity everyone must justify participating in. Availability bias can therefore operate through both individual judgment and institutional career incentives.

The policy implication is not that vivid examples should be ignored. Case evidence can be valuable. The problem is substituting memorable cases for representative evidence. Serious market analysis requires base rates, distributions, historical comparisons, stress tests, and scenario analysis that counterbalance the pull of available narratives.

Household Finance, Insurance, and Everyday Risk

Availability bias plays an important role in household financial behavior because households must make many decisions under uncertainty with limited time and incomplete information. They must judge whether to save, borrow, insure, invest, switch providers, buy warranties, prepare for emergencies, or avoid certain financial products. These choices often depend on perceived risk rather than objective probability.

Some risks are vivid and therefore overestimated. Fraud, theft, sudden market losses, visible disasters, and dramatic failures may receive high attention. Other risks are less vivid and therefore underestimated. These include compound interest on debt, gradual retirement shortfalls, recurring fees, underinsurance, medical debt exposure, inflation erosion, income volatility, and failure to maintain emergency savings. The less dramatic risks may be more common or more financially damaging over time.

Insurance demand often reflects this imbalance. Households may seek coverage after a vivid event but allow coverage to lapse when memory fades. They may buy extended warranties for memorable product failures while neglecting emergency savings or health coverage. They may underestimate low-salience risks such as disability, long-term care, or inadequate liability protection because these risks are hard to imagine until they occur.

Availability bias also shapes debt behavior. A household may focus on a visible one-time expense while underestimating the cumulative cost of high-interest credit. A promotional offer may feel safe because examples of harm are not available at the moment of purchase. Conversely, a dramatic debt story may produce excessive fear of all borrowing, even when some debt is productive or necessary. Availability can distort both overconfidence and avoidance.

Financial education should therefore include probability, base rates, cumulative cost, and scenario thinking. It should help people compare vivid risks with quiet risks. The goal is not to remove emotion from household finance, but to prevent memory salience from becoming the only risk model.

Digital Platforms and the Architecture of Attention

Digital platforms have made availability bias more powerful because they shape what people repeatedly see, remember, and discuss. Search results, trending topics, recommendation feeds, push notifications, viral videos, influencer commentary, market dashboards, ratings, reviews, and algorithmic rankings all structure cognitive accessibility. The digital environment does not merely provide information. It decides which examples become available.

In consumer markets, review platforms can make a few vivid experiences highly influential. A dramatic negative review may outweigh thousands of ordinary satisfactory transactions. A viral positive example may make a product feel more reliable than aggregate evidence supports. Ratings help consumers, but the most memorable review is not always the most representative one.

In financial markets, digital platforms can amplify salient narratives. A trading app may surface trending assets, dramatic price movements, social commentary, and recent gains. These cues make certain opportunities more available. A risk warning buried in small text may be less cognitively available than a chart showing recent growth. The interface frames what matters.

In public discourse, social media can make rare events feel common through repeated exposure. People may encounter the same incident through multiple accounts, clips, reposts, and commentary. Repetition creates the impression of frequency. This can intensify fear, outrage, speculation, or urgency. It can also make slow structural trends less visible because they lack shareable event form.

Digital platforms can also counter availability bias. They can show base rates, contextual denominators, historical comparisons, absolute risk, long-term trends, source quality, and uncertainty. They can reduce overexposure to sensational examples and improve visibility for slower but important risks. However, this requires design choices that prioritize public understanding over engagement maximization.

Availability bias is therefore a digital-governance issue. Whoever controls attention helps control perceived probability. Ethical platform design should recognize that making something visible repeatedly can change what people believe is likely, normal, or urgent.

Availability Bias, Framing, and Reference Effects

Availability bias often interacts with framing, anchoring, and reference effects. Events that are highly available are frequently also strongly framed. A crisis described with emotionally vivid language becomes easier to recall. A statistic paired with a memorable image becomes more salient. A risk framed as a threat to family, livelihood, community, or identity becomes more available than the same risk presented abstractly.

Anchoring can also work with availability. A recent price, loss, crisis, or success story may become the reference point for future judgment. An investor who remembers a sharp market decline may anchor on that loss when judging current risk. A consumer who remembers a high price may interpret a lower price as a bargain. A policymaker who remembers a recent institutional failure may overcorrect toward that type of risk while neglecting others.

Framing determines what is encoded into memory. A public-health risk framed through a vivid case may become more available than a risk described through population-level statistics. A climate risk framed through a recent disaster may be more available than a long-term emissions graph. A financial risk framed through personal catastrophe may be more memorable than one framed through expected value. The frame shapes recall.

These interactions matter because economic perception is cumulative. People build expectations from salient examples, repeated frames, and remembered anchors. Once a narrative becomes available, it can structure future interpretation. New evidence is then filtered through what already feels memorable and plausible.

This is why availability bias should not be treated as an isolated cognitive shortcut. It is part of a broader system of attention, framing, reference dependence, and narrative formation. Behavioral economics helps reveal how probability perception is socially and institutionally constructed.

Implications for Policy and Governance

Availability bias matters for policy because democratic and administrative systems depend on public risk perception. Citizens, voters, regulators, legislators, agencies, and institutions often respond to risks that are visible, recent, and emotionally salient. Less visible risks may receive inadequate attention even when evidence shows they are severe. This can distort public budgets, regulatory priorities, crisis response, and long-term planning.

Highly salient events can produce rapid policy action. A financial collapse may trigger new regulation. A visible public-health failure may generate institutional reform. A disaster may increase preparedness funding. Such responses can be necessary. But availability bias can also produce overreaction to recent events and underinvestment in risks that are less visible but more likely or more damaging over time.

Policy systems are vulnerable to “fighting the last war.” Institutions may prepare for the crisis that just happened while neglecting the next one. Public agencies may allocate resources toward visible threats rather than statistically significant risks. Political leaders may prioritize issues that dominate media attention. Regulatory systems may respond to scandal rather than structural vulnerability.

Effective governance must therefore build mechanisms that counterbalance availability. These include risk registers, independent statistical agencies, scenario planning, stress testing, cost-benefit analysis, public dashboards, base-rate communication, structured expert judgment, long-term budgeting, and institutional memory. The aim is not to ignore vivid events, but to place them in evidence-based context.

Communication also matters. Public institutions should help people understand the difference between salience and probability. This requires clear denominators, absolute risks, historical comparisons, uncertainty ranges, and explanations of slow-moving risks. A public that sees only crisis images may misjudge risk. A public that sees only abstract data may underreact. Responsible governance must connect evidence to attention without manipulating fear.

Availability Bias and Sustainability Decisions

Availability bias is central to sustainability because many environmental risks are difficult to perceive directly. Climate change, biodiversity loss, soil degradation, groundwater depletion, ocean acidification, pollution accumulation, and infrastructure vulnerability often unfold slowly, unevenly, and systemically. Because they are not always vivid in daily life, they can remain cognitively unavailable until a dramatic event occurs.

Environmental disasters can suddenly make long-term risks available. Wildfires, floods, heatwaves, hurricanes, crop failures, water shortages, and air-quality crises can produce sharp increases in public concern. These events may reveal real structural risk, but they also illustrate the availability dynamic: attention rises when risk becomes visible, personal, and emotionally salient. The underlying scientific evidence may have existed long before the event became memorable.

This creates a governance problem. Sustainability policy often requires action before disaster makes risk vivid. Waiting for availability means waiting too long. Climate mitigation, ecosystem protection, resilient infrastructure, and public-health preparation require institutions capable of acting on evidence even when risk is not yet emotionally available to the public.

At the same time, disaster-based communication must be handled carefully. Catastrophe framing can increase attention, but repeated fear without agency can produce fatigue, denial, or helplessness. Effective sustainability communication should connect vivid examples to broader evidence, show causal context, explain uncertainty honestly, identify practical pathways, and foreground justice. Communities already experiencing environmental harm should not be treated merely as examples for others’ attention.

Availability bias also affects sustainable consumption. People may respond to visible waste, dramatic pollution images, or extreme weather while underestimating less visible supply-chain impacts. Labels, dashboards, and public reporting can help make hidden impacts more available. But they must be evidence-based to avoid greenwashing. The goal is to make structural risk visible without turning sustainability into spectacle.

Ethical Questions: Attention, Fear, and Institutional Power

Availability bias raises ethical questions because institutions can shape what people remember. Firms, platforms, media organizations, political actors, public agencies, and advocacy groups can make some risks, benefits, identities, and narratives more available than others. This power can be used to educate, warn, and protect. It can also be used to manipulate fear, inflate urgency, distract from structural problems, or manufacture consent.

Fear-based communication is especially delicate. A vivid example can help people understand a serious risk. But repeated emotionally charged examples can also distort probability, stigmatize groups, or drive punitive policy. Public communication should distinguish between making risk visible and exploiting anxiety. The more vulnerable the audience, the higher the ethical burden.

Commercial uses of availability bias are also important. Advertising often relies on memorable images, testimonials, rare success stories, and emotionally vivid examples. These can make products feel safer, more effective, more common, or more desirable than evidence supports. Financial products, health products, insurance products, and digital platforms require particular scrutiny because the costs of distorted risk perception can be high.

Digital platforms carry special responsibility because they control repeated exposure at scale. Recommendation systems can amplify extreme, vivid, or emotionally charged examples because such content increases engagement. This can distort public risk perception even without explicit misinformation. Ethical platform governance should ask whether attention systems are making representative evidence more visible or merely maximizing cognitive availability for engagement.

Public institutions also need ethical discipline. They may use salience to improve public understanding, but they should not manipulate citizens into compliance by selectively presenting risk. Democratic legitimacy requires communication that is truthful, proportional, transparent, and open to contestation. Availability should be used to clarify evidence, not bypass judgment.

The ethical standard should be accountable salience: make important risks visible, connect vivid examples to broader evidence, avoid exaggeration, protect vulnerable groups, and disclose uncertainty honestly.

Empirical and Policy-Evaluation Lens

A professional economist-facing treatment of availability bias should ask what can be measured, identified, estimated, and evaluated. Availability bias can be studied through laboratory experiments, survey experiments, field experiments, administrative data, media-exposure measures, investor behavior, insurance demand, disaster preparedness, health-risk perception, consumer finance, climate communication, and digital-platform experiments.

The core empirical challenge is separating availability from information. A salient event may change beliefs because it makes examples easier to recall, but it may also convey real new information. A bank failure may increase perceived financial risk because it is vivid, but also because it reveals genuine institutional weakness. A flood may increase climate concern because it is emotionally salient, but also because it provides local evidence of vulnerability. Researchers must distinguish salience effects from Bayesian updating.

Useful research designs include random assignment to vivid versus statistical information, variation in media exposure, comparison of recent-event and no-recent-event populations, before-after analysis around salient events, investor trading responses to news shocks, insurance take-up after disasters, and experiments that present base rates alongside vivid examples. Outcome measures may include perceived probability, willingness to pay for insurance, portfolio allocation, policy support, preparedness behavior, risk recall, and comprehension of base rates.

Evaluation should not stop at belief change. A communication intervention that raises concern may not improve welfare if it causes panic, misallocation, or distrust. A vivid message may be useful if it improves comprehension of underappreciated risk. It may be harmful if it exaggerates rare dangers or crowds out more important risks. Policy evaluation should assess calibration: are beliefs closer to evidence after the intervention?

Heterogeneity is central. Availability effects may differ by prior experience, trust, education, numeracy, media habits, income security, geography, age, political identity, and exposure to risk. People who have personally experienced a disaster may interpret risk differently from those who encounter it only through media. Low-trust audiences may reject institutional base rates even when accurate. High-stress households may respond more strongly to vivid economic threats.

A rigorous availability-bias evaluation should ask: What became more available? Was the event representative? Did the intervention provide base rates? Did perceived risk become more accurate? Did behavior improve? Were some groups unduly alarmed or neglected? Did the communication increase understanding or only emotional intensity? These questions turn availability bias from a cognitive label into a serious empirical and institutional research agenda.

An Analytical Framework for Availability Bias

A simple way to formalize availability bias is to distinguish objective probability from perceived probability. Let the true probability of an event \(E\) be \(p(E)\). Under unbiased judgment, subjective probability equals objective probability:

\hat{p}(E) = p(E)

\]

Interpretation: In an unbiased probability judgment, perceived risk equals the true or evidence-based probability.

Under availability bias, perceived probability depends partly on cognitive accessibility \(A(E)\):

\hat{p}(E) = p(E) + \alpha A(E)

\]

Interpretation: The parameter \(\alpha\) measures how strongly availability shifts perceived probability above or below the evidence-based baseline.

Accessibility can be modeled as a function of recency, vividness, media exposure, personal experience, and emotional salience:

A(E) = \beta R(E) + \gamma V(E) + \delta M(E) + \theta X(E) + \omega S(E)

\]

Interpretation: Availability rises when events are recent, vivid, repeatedly covered, personally experienced, or emotionally salient.

In economic decision-making, biased probability can directly affect choice. Suppose an individual chooses a protective action \(Y_i = 1\), such as buying insurance, reducing portfolio risk, preparing for disaster, or supporting regulation. A stylized choice probability can be written as:

P(Y_i = 1) = f(\hat{p}_i(E), C_i, B_i, T_i)

\]

Interpretation: Action depends on perceived probability, cost, expected benefit, and trust in the information or institution.

If availability inflates perceived risk, protective action may rise even when objective risk is unchanged. If availability is low, protective action may remain weak even when objective risk is high. This is especially important for slow-moving risks such as climate change, retirement insecurity, infrastructure failure, and chronic health exposure.

In market settings, perceived probability can affect allocation. If an investor allocates risky assets according to perceived downside risk \(\hat{p}(L)\), then:

w_i = w_0 – \rho \hat{p}_i(L)

\]

Interpretation: The risky-asset share \(w_i\) falls as perceived loss probability rises, with \(\rho\) measuring risk sensitivity.

For policy evaluation, the effect of a salience or base-rate communication intervention can be represented as:

\tau = E[Y_i(1) – Y_i(0)]

\]

Interpretation: The treatment effect compares outcomes under an availability-related intervention with outcomes under a comparison condition.

A welfare-oriented communication model should include calibration, comprehension, autonomy, and emotional burden:

W_i = Q_i + C_i + A_i – D_i – B_i

\]

Interpretation: Welfare depends on decision quality, comprehension, autonomy, distortion, and emotional or administrative burden.

This broader framework prevents a simplistic conclusion that making a risk more salient is always beneficial. The goal is calibrated attention: risks should be visible in proportion to evidence, severity, uncertainty, and justice.

R Workflow: Simulating Salience, Recall, and Distorted Risk Perception

The following R workflow simulates agents who estimate risk based on both objective probability and availability-driven salience. It compares low, medium, and high availability environments and reports heterogeneity by availability sensitivity and numeracy. The workflow is designed as an economist-facing scaffold for investor sentiment, insurance demand, crisis communication, public-health risk, climate-risk salience, and policy evaluation.

# Availability Bias and Economic Perception

# R workflow: salience, recall, distorted probability, and risk behavior

# Synthetic data only. Economist-facing research scaffold.

set.seed(2020)

n_agents <- 2500

true_probability <- 0.12

agents <- data.frame(

agent_id = 1:n_agents,

availability_sensitivity = runif(n_agents, 0.10, 0.90),

numeracy = runif(n_agents, 0.20, 1.00),

trust_in_statistics = runif(n_agents, 0.20, 1.00),

risk_tolerance = runif(n_agents, 0.10, 0.90),

prior_experience = rbinom(n_agents, 1, 0.25)

)

simulate_availability_environment <- function(regime_name, salience_scale, base_rate_disclosure, emotional_intensity) {

recency_signal <- runif(n_agents, 0, 1) * salience_scale

vividness_signal <- runif(n_agents, 0, 1) * salience_scale

media_signal <- runif(n_agents, 0, 1) * salience_scale

social_repetition_signal <- runif(n_agents, 0, 1) * salience_scale

availability_score <- 0.25 * recency_signal +

0.25 * vividness_signal +

0.25 * media_signal +

0.25 * social_repetition_signal +

0.20 * agents$prior_experience * emotional_intensity

base_rate_correction <- base_rate_disclosure *

agents$numeracy *

agents$trust_in_statistics *

0.18

subjective_probability <- pmin(

pmax(

true_probability +

agents$availability_sensitivity * availability_score * 0.25 -

base_rate_correction,

0

),

1

)

calibration_error <- subjective_probability - true_probability

participate_in_risky_asset <- as.integer(

subjective_probability < (0.18 + agents$risk_tolerance * 0.12)

)

insurance_demand <- as.integer(

subjective_probability > (0.16 - agents$prior_experience * 0.03)

)

policy_support <- as.integer(

subjective_probability +

0.10 * emotional_intensity +

0.05 * agents$trust_in_statistics > 0.25

)

welfare_proxy <- 1 -

abs(calibration_error) -

0.08 * emotional_intensity * availability_score +

0.05 * base_rate_disclosure * agents$numeracy

data.frame(

agent_id = agents$agent_id,

regime = regime_name,

true_probability = true_probability,

availability_sensitivity = agents$availability_sensitivity,

numeracy = agents$numeracy,

trust_in_statistics = agents$trust_in_statistics,

risk_tolerance = agents$risk_tolerance,

prior_experience = agents$prior_experience,

recency_signal = recency_signal,

vividness_signal = vividness_signal,

media_signal = media_signal,

social_repetition_signal = social_repetition_signal,

availability_score = availability_score,

base_rate_disclosure = base_rate_disclosure,

emotional_intensity = emotional_intensity,

subjective_probability = subjective_probability,

calibration_error = calibration_error,

participate_in_risky_asset = participate_in_risky_asset,

insurance_demand = insurance_demand,

policy_support = policy_support,

welfare_proxy = welfare_proxy

)

}

low_availability <- simulate_availability_environment(

regime_name = "low_availability_with_base_rates",

salience_scale = 0.60,

base_rate_disclosure = 0.80,

emotional_intensity = 0.25

)

medium_availability <- simulate_availability_environment(

regime_name = "medium_availability_environment",

salience_scale = 1.00,

base_rate_disclosure = 0.45,

emotional_intensity = 0.55

)

high_availability <- simulate_availability_environment(

regime_name = "high_availability_no_base_rates",

salience_scale = 1.50,

base_rate_disclosure = 0.10,

emotional_intensity = 0.85

)

panel <- rbind(low_availability, medium_availability, high_availability)

regime_summary <- aggregate(

cbind(subjective_probability, calibration_error, participate_in_risky_asset, insurance_demand, policy_support, welfare_proxy) ~ regime,

data = panel,

FUN = mean

)

panel$availability_sensitivity_quartile <- cut(

panel$availability_sensitivity,

breaks = quantile(panel$availability_sensitivity, probs = seq(0, 1, 0.25)),

include.lowest = TRUE,

labels = paste0("Q", 1:4)

)

heterogeneity <- aggregate(

cbind(subjective_probability, calibration_error, insurance_demand, policy_support) ~ regime + availability_sensitivity_quartile,

data = panel,

FUN = mean

)

print(regime_summary)

print(heterogeneity)

dir.create("outputs/tables", recursive = TRUE, showWarnings = FALSE)

write.csv(panel, "outputs/tables/r_availability_bias_panel.csv", row.names = FALSE)

write.csv(regime_summary, "outputs/tables/r_availability_bias_regime_summary.csv", row.names = FALSE)

write.csv(heterogeneity, "outputs/tables/r_availability_bias_heterogeneity.csv", row.names = FALSE)This workflow shows how perceived probability can rise sharply when salience, recency, vividness, and media exposure increase, even when objective risk is unchanged. It also shows why base-rate communication can reduce calibration error, especially among agents with higher numeracy and trust in statistical information.

Python Workflow: Comparing Risk Judgments Under Availability Conditions

The following Python workflow compares risk perception under low, medium, and high availability environments. It produces synthetic agent-level data, regime summaries, treatment-effect estimates, and heterogeneity tables by availability sensitivity, numeracy, and prior experience. The workflow can be extended to investor sentiment, insurance choice, public-health communication, disaster preparedness, consumer risk perception, and climate-risk messaging.

# Availability Bias and Economic Perception

# Python workflow: availability, perceived probability, risk behavior, and welfare

# Synthetic data only. Economist-facing research scaffold.

from __future__ import annotations

from pathlib import Path

import numpy as np

import pandas as pd

rng = np.random.default_rng(2020)

n_agents = 3000

true_probability = 0.12

agents = pd.DataFrame({

"agent_id": np.arange(1, n_agents + 1),

"availability_sensitivity": rng.uniform(0.10, 0.90, n_agents),

"numeracy": rng.uniform(0.20, 1.00, n_agents),

"trust_in_statistics": rng.uniform(0.20, 1.00, n_agents),

"risk_tolerance": rng.uniform(0.10, 0.90, n_agents),

"prior_experience": rng.binomial(1, 0.25, n_agents),

})

def simulate_availability_environment(

regime_name: str,

salience_scale: float,

base_rate_disclosure: float,

emotional_intensity: float

) -> pd.DataFrame:

"""Simulate subjective risk perception under an availability environment."""

recency_signal = rng.uniform(0, 1, n_agents) * salience_scale

vividness_signal = rng.uniform(0, 1, n_agents) * salience_scale

media_signal = rng.uniform(0, 1, n_agents) * salience_scale

social_repetition_signal = rng.uniform(0, 1, n_agents) * salience_scale

availability_score = (

0.25 * recency_signal

+ 0.25 * vividness_signal

+ 0.25 * media_signal

+ 0.25 * social_repetition_signal

+ 0.20 * agents["prior_experience"].to_numpy() * emotional_intensity

)

base_rate_correction = (

base_rate_disclosure

* agents["numeracy"].to_numpy()

* agents["trust_in_statistics"].to_numpy()

* 0.18

)

subjective_probability = np.clip(

true_probability

+ agents["availability_sensitivity"].to_numpy() * availability_score * 0.25

- base_rate_correction,

0,

1

)

calibration_error = subjective_probability - true_probability

participate_in_risky_asset = (

subjective_probability < (0.18 + agents["risk_tolerance"].to_numpy() * 0.12)

).astype(int)

insurance_demand = (

subjective_probability > (0.16 - agents["prior_experience"].to_numpy() * 0.03)

).astype(int)

policy_support = (

subjective_probability

+ 0.10 * emotional_intensity

+ 0.05 * agents["trust_in_statistics"].to_numpy()

> 0.25

).astype(int)

welfare_proxy = (

1

- np.abs(calibration_error)

- 0.08 * emotional_intensity * availability_score

+ 0.05 * base_rate_disclosure * agents["numeracy"].to_numpy()

)

return pd.DataFrame({

"agent_id": agents["agent_id"],

"regime": regime_name,

"true_probability": true_probability,

"availability_sensitivity": agents["availability_sensitivity"],

"numeracy": agents["numeracy"],

"trust_in_statistics": agents["trust_in_statistics"],

"risk_tolerance": agents["risk_tolerance"],

"prior_experience": agents["prior_experience"],

"recency_signal": recency_signal,

"vividness_signal": vividness_signal,

"media_signal": media_signal,

"social_repetition_signal": social_repetition_signal,

"availability_score": availability_score,

"base_rate_disclosure": base_rate_disclosure,

"emotional_intensity": emotional_intensity,

"subjective_probability": subjective_probability,

"calibration_error": calibration_error,

"participate_in_risky_asset": participate_in_risky_asset,

"insurance_demand": insurance_demand,

"policy_support": policy_support,

"welfare_proxy": welfare_proxy,

"medium_availability_treat": int(regime_name == "medium_availability_environment"),

"high_availability_treat": int(regime_name == "high_availability_no_base_rates"),

})

panel = pd.concat([

simulate_availability_environment(

regime_name="low_availability_with_base_rates",

salience_scale=0.60,

base_rate_disclosure=0.80,

emotional_intensity=0.25

),

simulate_availability_environment(

regime_name="medium_availability_environment",

salience_scale=1.00,

base_rate_disclosure=0.45,

emotional_intensity=0.55

),

simulate_availability_environment(

regime_name="high_availability_no_base_rates",

salience_scale=1.50,

base_rate_disclosure=0.10,

emotional_intensity=0.85

),

], ignore_index=True)

summary = panel.groupby("regime").agg(

agents=("agent_id", "count"),

mean_availability_score=("availability_score", "mean"),

mean_subjective_probability=("subjective_probability", "mean"),

mean_calibration_error=("calibration_error", "mean"),

share_participating_risky_asset=("participate_in_risky_asset", "mean"),

insurance_demand_rate=("insurance_demand", "mean"),

policy_support_rate=("policy_support", "mean"),

mean_welfare_proxy=("welfare_proxy", "mean"),

).reset_index()

print(summary.sort_values("mean_subjective_probability", ascending=False))

try:

import statsmodels.api as sm

outcomes = [

"subjective_probability",

"calibration_error",

"participate_in_risky_asset",

"insurance_demand",

"policy_support",

"welfare_proxy"

]

controls = [

"medium_availability_treat",

"high_availability_treat",

"availability_sensitivity",

"numeracy",

"trust_in_statistics",

"risk_tolerance",

"prior_experience",

"availability_score",

"base_rate_disclosure",

"emotional_intensity"

]

for outcome in outcomes:

X = sm.add_constant(panel[controls])

model = sm.OLS(panel[outcome], X).fit(cov_type="HC1")

print(f"\nOutcome: {outcome}")

print(model.summary().tables[1])

except ImportError:

print("statsmodels is not installed; skipping regression table.")

panel["availability_sensitivity_quartile"] = pd.qcut(

panel["availability_sensitivity"],

4,

labels=["Q1", "Q2", "Q3", "Q4"]

)

panel["numeracy_quartile"] = pd.qcut(

panel["numeracy"],

4,

labels=["Q1", "Q2", "Q3", "Q4"]

)

availability_heterogeneity = panel.groupby(

["regime", "availability_sensitivity_quartile"],

observed=False

).agg(

mean_subjective_probability=("subjective_probability", "mean"),

mean_calibration_error=("calibration_error", "mean"),

insurance_demand_rate=("insurance_demand", "mean"),

policy_support_rate=("policy_support", "mean"),

).reset_index()

numeracy_heterogeneity = panel.groupby(

["regime", "numeracy_quartile"],

observed=False

).agg(

mean_subjective_probability=("subjective_probability", "mean"),

mean_calibration_error=("calibration_error", "mean"),

mean_welfare_proxy=("welfare_proxy", "mean"),

).reset_index()

output_dir = Path("outputs/tables")

output_dir.mkdir(parents=True, exist_ok=True)

panel.to_csv(output_dir / "synthetic_availability_bias_panel.csv", index=False)

summary.to_csv(output_dir / "availability_bias_regime_summary.csv", index=False)

availability_heterogeneity.to_csv(output_dir / "availability_bias_sensitivity_heterogeneity.csv", index=False)

numeracy_heterogeneity.to_csv(output_dir / "availability_bias_numeracy_heterogeneity.csv", index=False)For analysts and policymakers, the core lesson is that perceived probability can shift dramatically with salience and recall even when objective risk remains unchanged. Base-rate communication, statistical context, and trusted evidence can reduce distortion, but only when they are made cognitively available at the point of judgment.

Stata Replication Note: Availability Bias and Risk Perception

For an economist-facing repository, the companion code should support Stata as well as R and Python. The article-level GitHub folder should include a Stata workflow that imports the synthetic availability-bias dataset, estimates treatment effects, reports robust standard errors, and exports regression tables. A compact Stata pattern for this article would look like this:

clear all

set more off

* Availability Bias and Economic Perception

* Stata risk-perception evaluation workflow using synthetic data.

global ROOT "`c(pwd)'"

global TABLES "$ROOT/outputs/tables"

global REG "$ROOT/outputs/regression_tables"

capture mkdir "$REG"

import delimited "$TABLES/synthetic_availability_bias_panel.csv", clear varnames(1)

label variable medium_availability_treat "Medium availability environment"

label variable high_availability_treat "High availability / low base-rate environment"

label variable subjective_probability "Subjective probability"

label variable calibration_error "Subjective minus true probability"

label variable insurance_demand "Insurance demand indicator"

label variable policy_support "Policy support indicator"

label variable welfare_proxy "Synthetic welfare proxy"

local controls availability_sensitivity numeracy trust_in_statistics risk_tolerance prior_experience availability_score base_rate_disclosure emotional_intensity

local outcomes subjective_probability calibration_error participate_in_risky_asset insurance_demand policy_support welfare_proxy

tempname handle

postfile `handle' str55 outcome str55 term double estimate double std_error double p_value double n using "$REG/stata_availability_bias_estimates.dta", replace

foreach y of local outcomes {

regress `y' medium_availability_treat high_availability_treat `controls', vce(robust)

foreach x in medium_availability_treat high_availability_treat {

local b = _b[`x']

local se = _se[`x']

local p = 2 * ttail(e(df_r), abs(_b[`x'] / _se[`x']))

local n = e(N)

post `handle' ("`y'") ("`x'") (`b') (`se') (`p') (`n')

}

}

postclose `handle'

use "$REG/stata_availability_bias_estimates.dta", clear

export delimited using "$REG/stata_availability_bias_estimates.csv", replace

* Heterogeneity by availability-sensitivity quartile.

import delimited "$TABLES/synthetic_availability_bias_panel.csv", clear varnames(1)

xtile availability_sensitivity_quartile = availability_sensitivity, nq(4)

tempname h

postfile `h' str30 group str55 term double estimate double std_error double p_value double n using "$REG/stata_availability_bias_sensitivity_heterogeneity.dta", replace

forvalues q = 1/4 {

regress subjective_probability medium_availability_treat high_availability_treat `controls' if availability_sensitivity_quartile == `q', vce(robust)

foreach x in medium_availability_treat high_availability_treat {

local b = _b[`x']

local se = _se[`x']

local p = 2 * ttail(e(df_r), abs(_b[`x'] / _se[`x']))

local n = e(N)

post `h' ("availability_q`q'") ("`x'") (`b') (`se') (`p') (`n')

}

}

postclose `h'

use "$REG/stata_availability_bias_sensitivity_heterogeneity.dta", clear

export delimited using "$REG/stata_availability_bias_sensitivity_heterogeneity.csv", replace

display "Stata availability-bias evaluation workflow complete."The purpose of including Stata is to make the repository useful to economists, behavioral public policy researchers, household-finance analysts, consumer-protection researchers, climate-risk researchers, health economists, digital-platform researchers, and graduate-level applied researchers who commonly work across Stata, R, and Python. The full repository scaffold should include identification notes, robustness plans, replication instructions, synthetic availability-regime panels, treatment-effect estimation, heterogeneity analysis, calibration diagnostics, welfare proxies, media-salience notes, and policy-design notes.

GitHub Repository

The companion repository provides reproducible scaffolding for the computational side of this article, including synthetic availability-bias datasets, salience and recall simulations, perceived-probability distortion models, base-rate correction workflows, risk-calibration diagnostics, investor-sentiment examples, insurance-demand models, policy-support simulations, robustness checks, Stata/R/Python workflows, SQL metadata structures, and scientific-computing examples for behavioral economics research.

Complete Code Repository

This article is supported by an article-level folder in the Behavioral Economics computational repository, with synthetic availability-bias and economic-perception datasets, causal-inference workflows, salience and recall simulations, perceived-probability distortion models, base-rate correction diagnostics, investor-sentiment examples, insurance-demand workflows, media-salience analysis, climate-risk communication scaffolds, policy-support simulations, econometric identification notes, robustness and sensitivity checks, Stata/R/Python workflows, SQL metadata structures, and scientific-computing examples for studying availability bias, economic perception, risk judgment, market narratives, public communication, digital platforms, sustainability governance, and institutional design.

Interpretive Limits and Cautions

Availability bias is powerful, but it should not be used to dismiss all salient concern as irrational. Sometimes a vivid event is genuinely informative. A bank failure may reveal systemic weakness. A wildfire may reveal local climate vulnerability. A public-health incident may expose institutional failure. A personal experience of job loss may correctly change household risk assessment. The question is not whether salient events matter. The question is whether perception remains calibrated to broader evidence.

There is also a risk of treating statistical base rates as automatically neutral. Data are collected through institutions, categories, definitions, and power. Some risks affecting marginalized communities may be statistically undercounted or publicly ignored precisely because they are not made available to dominant audiences. In such cases, making hidden harms visible is not a bias; it is a corrective.

Availability bias should also not be used to criticize emotional response in a simplistic way. Emotion can carry moral knowledge. Public outrage after disaster, fraud, abuse, or institutional failure may be appropriate. The problem arises when emotional availability substitutes for proportional assessment, long-term evidence, or attention to less visible harms.

Base-rate communication must be designed carefully. Simply telling people that a risk is statistically rare may not be persuasive if they lack trust, have direct experience, or face unequal vulnerability. A risk can be rare on average and still severe for a specific community. Calibration requires both statistical evidence and contextual respect.

Finally, availability bias should be analyzed alongside media power, digital-platform incentives, political communication, and institutional credibility. The most available risks are not always naturally available. They are often made available by systems that decide what to repeat, emphasize, monetize, or ignore. Behavioral economics should make that attention power visible.

Conclusion

Availability bias shows that economic judgment is shaped not only by probability and payoff, but by memory, salience, vividness, media exposure, personal experience, and social repetition. People often judge risks and opportunities by what comes most easily to mind. This shortcut can be useful, but it can also distort economic perception when the most memorable examples are not representative.

The significance of availability bias lies in its breadth. It affects investors, consumers, households, policymakers, institutions, markets, digital platforms, public communication, and sustainability governance. It helps explain why societies can overreact to dramatic events while underreacting to slow-moving structural risks. It also explains why risk communication must do more than publish information. It must make evidence understandable, proportionate, memorable, and trustworthy.

The mature lesson is not that vivid examples should be ignored. Examples matter. Stories matter. Lived experience matters. But they must be connected to base rates, distributions, history, uncertainty, and structural analysis. A single memorable case should open inquiry, not replace evidence.

In that sense, availability bias is one of the most important bridges between behavioral economics, media systems, risk governance, consumer protection, financial judgment, and environmental policy. It reminds us that what a society remembers easily can shape what it fears, funds, regulates, buys, insures, and prepares for.

Related Articles

- Behavioral Economics

- Heuristics and Biases in Economic Decision-Making

- Bounded Rationality in Economic Decision-Making

- Behavioral Finance and Investor Psychology

- Herd Behavior in Financial Markets

- Overconfidence Bias in Financial Markets

- Anchoring Bias in Economic Judgment

- Framing Effects in Consumer Choice

- Choice Architecture and Decision Environments

- Nudge Theory and Behavioral Public Policy

- Behavioral Insights in Environmental Policy

- Behavioral Economics and Sustainable Consumption

Further Reading

- Kahneman, D. (2011) Thinking, Fast and Slow. New York: Farrar, Straus and Giroux. Available at: https://us.macmillan.com/books/9780374533557/thinkingfastandslow.

- Kuran, T. and Sunstein, C.R. (1999) ‘Availability cascades and risk regulation’, Stanford Law Review, 51(4), pp. 683–768. Available at: https://www.jstor.org/stable/1229439.

- Shiller, R.J. (2019) Narrative Economics: How Stories Go Viral and Drive Major Economic Events. Princeton, NJ: Princeton University Press. Available at: https://press.princeton.edu/books/hardcover/9780691182292/narrative-economics.

- Slovic, P. (1987) ‘Perception of risk’, Science, 236(4799), pp. 280–285. Available at: https://www.science.org/doi/10.1126/science.3563507.

- Steele, K. (2015) ‘Decision theory’, The Stanford Encyclopedia of Philosophy. Available at: https://plato.stanford.edu/entries/decision-theory/.

- Thaler, R.H. (2015) Misbehaving: The Making of Behavioral Economics. New York: W.W. Norton. Available at: https://wwnorton.com/books/misbehaving/.

- Tversky, A. and Kahneman, D. (1973) ‘Availability: A heuristic for judging frequency and probability’, Cognitive Psychology, 5(2), pp. 207–232. Available at: https://doi.org/10.1016/0010-0285(73)90033-9.

- Tversky, A. and Kahneman, D. (1974) ‘Judgment under uncertainty: Heuristics and biases’, Science, 185(4157), pp. 1124–1131. Available at: https://www.science.org/doi/10.1126/science.185.4157.1124.

References

- Kahneman, D. (2011) Thinking, Fast and Slow. New York: Farrar, Straus and Giroux. Available at: https://us.macmillan.com/books/9780374533557/thinkingfastandslow.

- Kuran, T. and Sunstein, C.R. (1999) ‘Availability cascades and risk regulation’, Stanford Law Review, 51(4), pp. 683–768. Available at: https://www.jstor.org/stable/1229439.

- Shiller, R.J. (2019) Narrative Economics: How Stories Go Viral and Drive Major Economic Events. Princeton, NJ: Princeton University Press. Available at: https://press.princeton.edu/books/hardcover/9780691182292/narrative-economics.

- Slovic, P. (1987) ‘Perception of risk’, Science, 236(4799), pp. 280–285. Available at: https://www.science.org/doi/10.1126/science.3563507.

- Steele, K. (2015) ‘Decision theory’, The Stanford Encyclopedia of Philosophy. Available at: https://plato.stanford.edu/entries/decision-theory/.

- Thaler, R.H. (2015) Misbehaving: The Making of Behavioral Economics. New York: W.W. Norton. Available at: https://wwnorton.com/books/misbehaving/.

- Tversky, A. and Kahneman, D. (1973) ‘Availability: A heuristic for judging frequency and probability’, Cognitive Psychology, 5(2), pp. 207–232. Available at: https://doi.org/10.1016/0010-0285(73)90033-9.

- Tversky, A. and Kahneman, D. (1974) ‘Judgment under uncertainty: Heuristics and biases’, Science, 185(4157), pp. 1124–1131. Available at: https://www.science.org/doi/10.1126/science.185.4157.1124.