Last Updated May 25, 2026

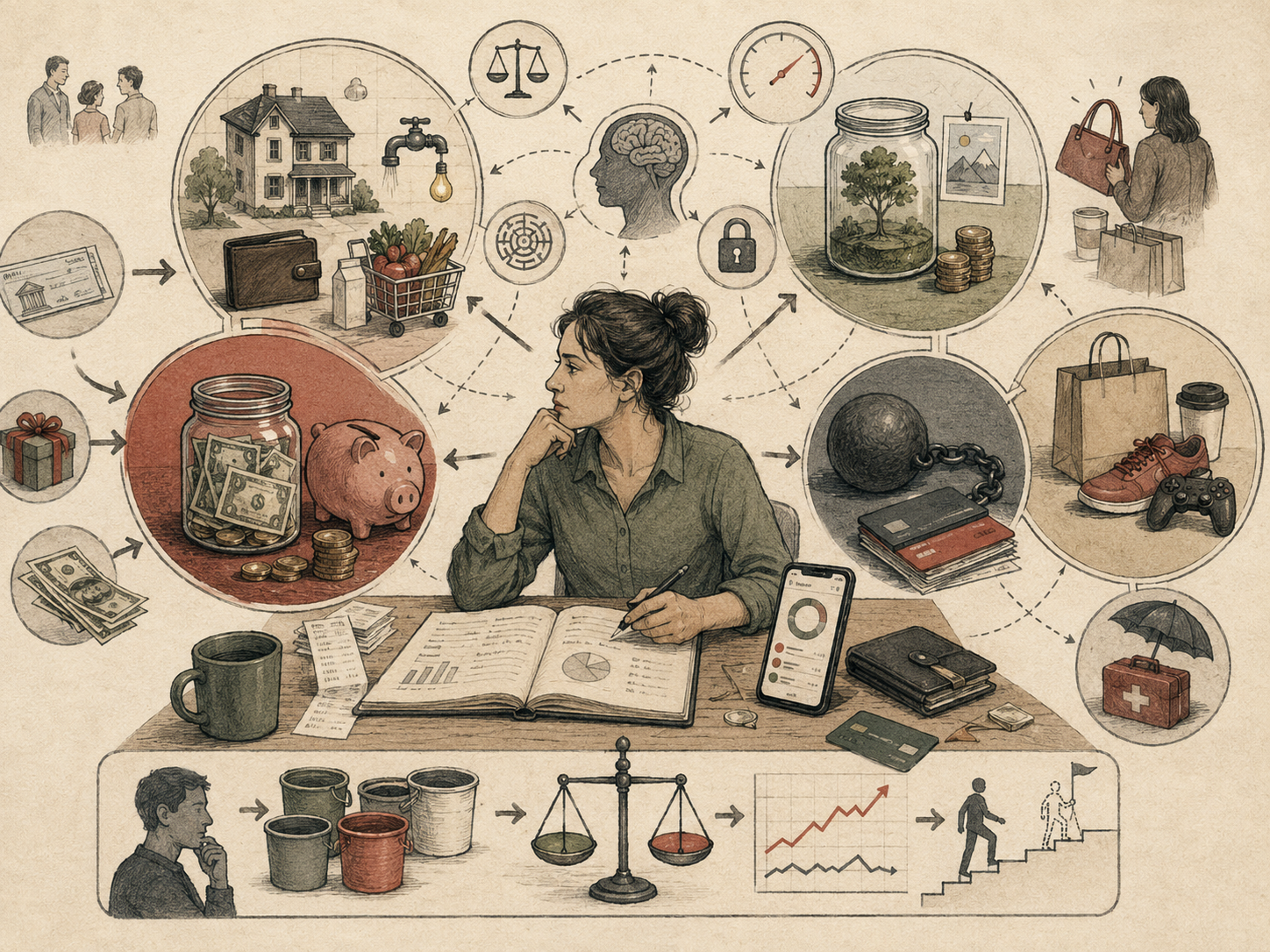

Mental accounting refers to the cognitive process through which individuals categorize, label, and evaluate financial resources in separate psychological accounts rather than treating all money as perfectly interchangeable. In behavioral economics, mental accounting helps explain why people often make different decisions depending on how money is framed, where it comes from, what purpose it has been assigned, or what account it is mentally placed into. It is one of the most influential behavioral explanations for everyday financial decision-making because it shows how budgeting, spending, saving, debt repayment, windfall use, and household planning are shaped as much by cognitive organization as by formal economic optimization.

Classical economic theory assumes that money is fungible. In principle, each dollar should be treated identically regardless of origin, label, or intended use. If one source of funds can reduce costly debt more efficiently than another, or if one account can serve a more urgent purpose, then resources should be reallocated according to the household’s full balance sheet. Behavioral research shows that real people frequently violate this assumption. They divide financial resources into separate mental categories and evaluate decisions within those categories rather than across total wealth, total debt, and long-term welfare.

Main Library

Publications

Article Map

Behavioral Economics

Related Topic

Economic Systems

Related Topic

Institutions & Governance

Related Topic

Stewardship & Ethics

Mental accounting has a dual character. It can help people manage financial complexity by creating practical categories for rent, food, transportation, emergencies, gifts, retirement, education, or discretionary spending. These categories can support discipline, reduce impulsive consumption, and protect long-term goals. Yet the same categories can also produce economically inconsistent outcomes. A household may preserve a vacation fund while carrying expensive credit-card debt, spend a tax refund more freely than regular wages, or refuse to draw from an emergency reserve for a financially optimal reason because the money feels psychologically unavailable.

For this reason, mental accounting sits at the intersection of bounded rationality, framing, self-control, household finance, consumer behavior, and institutional design. It shows that people do not merely hold financial assets and liabilities. They interpret them. The labels attached to money can shape what feels spendable, protected, deserved, risky, responsible, or forbidden. A serious treatment of mental accounting must therefore ask when psychological categories support welfare and when they prevent households from seeing their true financial position.

The Concept of Mental Accounting

Mental accounting was introduced by Richard Thaler as part of the broader development of behavioral economics. The concept describes how individuals organize financial decisions into distinct psychological categories rather than evaluating all resources through a unified economic framework. In practice, people often create separate mental accounts for wages, household necessities, entertainment, gifts, savings, debt repayment, tax refunds, bonuses, retirement funds, emergency reserves, vacations, education, or “extra” money.

These categories help simplify complex financial life. A household budget would be cognitively demanding if every decision required a full recalculation of lifetime income, debt, risk, savings, and expected future needs. Mental accounts reduce complexity by imposing practical rules: this money is for rent; this money is for groceries; this money is for emergencies; this money is for the future; this money is discretionary. In that sense, mental accounting is a form of bounded rationality. It is a cognitive strategy for making financial life manageable under limited attention, limited time, and limited computational capacity.

The problem is that these categories can become too rigid. Once money is assigned to a mental account, it may stop feeling fully interchangeable with money elsewhere. A household may protect a labeled account even when reallocating funds would reduce high-interest debt. A consumer may treat a rebate as permission to spend, even while regular income remains constrained. A person may view a tax refund as a bonus rather than as delayed income that could strengthen the balance sheet.

Mental accounting therefore has both functional and distorting effects. It can support planning and self-control, but it can also fragment household decision-making. The same structure that protects savings can prevent efficient debt repayment. The same label that makes a goal concrete can make money feel unavailable for urgent needs. The same budget category that prevents overspending can produce arbitrary constraints when circumstances change.

The concept is powerful because it explains why real financial behavior can appear simultaneously disciplined and inefficient. People are often not careless. They are using psychological categories that make sense locally but may not optimize globally. Mental accounting reveals how financial decisions are shaped by meaning, not only by arithmetic.

Fungibility and Economic Theory

Traditional economic theory assumes that money is fungible. Receiving $100 in wages should, in principle, produce the same decision possibilities as receiving $100 from a lottery ticket, gift, rebate, bonus, or tax refund. The economically relevant question should be what allocation best serves overall welfare, not what label is attached to the source of the money.

Mental accounting challenges this assumption by showing that source, timing, framing, and labeling frequently matter. Individuals often spend unexpected income more freely than earned income, protect labeled savings more strongly than unlabeled balances, or mentally segregate resources that are formally identical. A dollar in a “vacation fund” may not feel like the same dollar as a dollar in a checking account. A dollar received as a tax refund may not feel like a dollar earned through regular work. A dollar on a gift card may not feel like a dollar in cash.

The departure from fungibility is not always irrational in a practical sense. Labels can help people protect commitments. Separate accounts can reduce temptation. Budget categories can prevent impulsive spending. A household that treats retirement savings as psychologically unavailable may be making a sensible self-control move. The issue is not that all mental accounting is bad. The issue is that money labels can become behaviorally powerful even when they no longer serve the household’s broader welfare.

This pattern is closely related to Framing Effects in Consumer Choice. The same nominal amount may be evaluated differently depending on whether it is framed as income, savings, a reward, a windfall, debt relief, emergency money, or discretionary money. The economic value is identical, but the psychological meaning changes.

Fungibility is therefore best understood as a rational benchmark. It tells us how money would be treated under integrated optimization. Mental accounting tells us how money is often treated under real cognitive, emotional, and institutional conditions. The gap between the two is where much of household finance actually happens.

How Psychological Accounts Work

Mental accounts usually operate through three linked mechanisms: categorization, labeling, and evaluation. Categorization separates resources into distinct groups. Labeling gives those groups meaning. Evaluation determines whether spending from a category feels appropriate, excessive, responsible, or forbidden. Together, these mechanisms create a financial map that may differ sharply from the household’s formal balance sheet.

Categorization can be explicit or implicit. A household may use actual bank subaccounts, budgeting envelopes, spreadsheets, prepaid cards, savings jars, or app categories. But many mental accounts are purely psychological. A person may “know” that certain money is for bills, certain money is for fun, and certain money should not be touched, even if all of it sits in the same bank account.

Labeling shapes the emotional meaning of money. “Emergency fund” creates a norm of protection. “Bonus” creates a sense of reward. “Tax refund” creates the feeling of a lump-sum gain. “Vacation fund” creates a future-oriented goal. “Grocery money” creates a boundary around necessity. These labels are powerful because they attach moral, temporal, and emotional meaning to otherwise interchangeable resources.

Evaluation then occurs inside the account. A $100 dinner may feel extravagant if charged to a grocery budget but acceptable if paid from an entertainment budget. A $500 purchase may feel irresponsible if it comes from checking but permissible if funded by a bonus. A debt payment may feel less satisfying than adding to a labeled savings goal, even when debt repayment would produce a higher financial return through avoided interest.

These account boundaries can be strengthened by institutions. Banks, employers, apps, tax systems, benefit programs, and retirement plans all create labels around money. A payroll deduction makes retirement savings feel separate from take-home pay. A health savings account gives funds a medical identity. A gift card assigns money to a store. A tax refund arrives as a lump sum and may be interpreted as extra money. Institutional design can either support beneficial mental accounting or exploit it.

The key point is that financial categories do not merely organize money. They change behavior. A serious analysis of household finance must therefore study the account architecture through which money is perceived, not only the formal totals on a balance sheet.

Mental Accounting in Consumer Behavior

Mental accounting influences a wide range of consumer decisions. People often maintain separate budgets for housing, groceries, transportation, entertainment, travel, subscriptions, gifts, emergencies, education, or holidays. These categories can support discipline by making spending visible and bounded. A grocery budget may prevent restaurant spending from crowding out household necessities. A rent account may protect essential payments. A gift budget may help households manage social obligations without losing track of total spending.

At the same time, category-based evaluation can produce inconsistencies across the broader financial picture. A consumer may refuse to use savings to pay off high-interest credit-card debt because the savings are earmarked for another purpose. A household may preserve a “vacation fund” while financing everyday consumption through costly borrowing. A shopper may spend a store credit more freely than cash because the store credit is mentally coded as restricted or already-spent money. A person may treat cash differently from card balances because payment mode changes the salience of loss.

Consumer behavior is also affected by transaction framing. A discount may make spending feel like saving. A rebate may feel like a gain even if it follows an unnecessary purchase. A subscription may move spending out of active attention and into a recurring background account. Buy-now-pay-later products may separate consumption from payment, weakening the perceived link between purchase and financial cost. These design features interact with mental accounting by changing which account is activated at the moment of choice.

Mental accounting helps explain why households can be careful in one domain and loose in another. A person may be frugal with groceries but spend freely on travel. A household may aggressively search for discounts while ignoring expensive credit-card interest. Someone may avoid small fees while accepting larger hidden costs. These patterns are not random. They often reflect account-specific rules, norms, and emotional meanings.

For consumer protection, this matters because financial products can be designed to either clarify or obscure account relationships. Good design helps people see total cost, total debt, and total cash flow. Harmful design exploits segmentation by making spending feel painless, debt feel distant, or fees feel detached from the main decision.

Windfall Gains and Spending Behavior

Mental accounting is especially useful for explaining why unexpected income is often treated differently from regular earnings. Tax refunds, bonuses, rebates, lottery winnings, gifts, inheritances, stimulus payments, found money, and cash-back rewards are frequently categorized as “extra” resources. Because they are mentally separated from ordinary income, they may be spent more freely or directed toward discretionary consumption rather than debt reduction, emergency savings, or long-term investment.

This pattern reveals that financial behavior is shaped not only by amount, but by meaning. Money coded as a windfall may feel less constrained by obligation, even though its purchasing power is identical to ordinary income. A $1,000 refund can feel like a gain even if it represents over-withholding from prior wages. A bonus can feel like permission to indulge even if the household carries expensive debt. A rebate can make a purchase feel cheaper after the fact, even when the original expenditure was unnecessary.

Windfalls also interact with self-licensing. People may feel that unexpected money is deserved, lucky, or separate from the responsible household budget. This can temporarily relax spending restraint. The emotional frame is not “What is the best use of this money across my whole financial life?” but “What can I do with this extra money?” That question activates a different mental account.

Not all windfall spending is harmful. A household may rationally use a bonus for rest, social life, repair, celebration, or needed consumption. Behavioral economics should not reduce every discretionary purchase to error. The analytical issue is whether the windfall label prevents the household from considering competing uses with higher long-term value. If the household is carrying high-interest debt, lacks emergency savings, or faces upcoming obligations, the windfall frame may lead to costly under-allocation toward financial resilience.

Policy and institutional design can influence windfall use. Tax systems, benefit programs, employers, and banks can present lump-sum income in ways that encourage splitting across spending, saving, and debt repayment. A system that prompts households to allocate a refund across multiple goals may work with mental accounting rather than against it. The goal is not to eliminate windfall joy, but to make the broader opportunity cost visible.

Debt, Savings, and Balance-Sheet Inefficiency

One of the clearest financial consequences of mental accounting is the coexistence of low-yield savings and high-cost debt. From a unified balance-sheet perspective, a household should compare the return on savings with the interest cost of debt. If liquid savings earn little while credit-card debt accumulates high interest, paying down debt may produce a larger financial benefit than preserving the savings balance.

Mental accounting can block that reallocation. Savings may be labeled as an emergency fund, vacation fund, education fund, home fund, or psychological safety reserve. Debt may be assigned to a separate mental account, where minimum payments are treated as the relevant obligation. The household then evaluates savings and debt separately rather than jointly. This can produce an inefficiency gap: debt remains outstanding while liquid assets remain protected.

This behavior is not necessarily foolish. Liquidity has value. A household with uncertain income, medical risk, unstable employment, or limited credit access may rationally preserve cash even while carrying debt. The problem arises when the account label becomes stronger than the underlying reason for liquidity. If savings are protected because of category meaning rather than real emergency need, the household may pay unnecessary interest.

Mental accounting can also shape debt repayment. Some households prefer the “debt snowball” method, paying off small balances first even when larger balances carry higher interest rates. From a strict cost-minimization view, the highest-interest debt should be prioritized. From a behavioral view, closing small accounts can create motivation, perceived progress, and persistence. This is another example of the dual character of mental accounting. It may be financially suboptimal in narrow arithmetic terms but useful if it increases sustained repayment.

The central question is therefore not whether mental accounting violates fungibility. It often does. The stronger question is whether the violation improves or harms long-term welfare. A household may need account labels to maintain discipline. But the same labels should be periodically reviewed against the full balance sheet, especially when debt costs, income risk, or household obligations change.

Mental Accounting and Time Preferences

Mental accounting is closely related to intertemporal choice because accounts often carry different time horizons. A retirement account is future-oriented. A checking account is present-oriented. An emergency fund is contingent and protective. A vacation fund is goal-oriented. A discretionary spending account is immediate. Each account has a different temporal meaning, even though all accounts are part of the same household economy.

This connects directly to Present Bias and Immediate Reward and Time Discounting and Long-Term Decision-Making. Mental accounting helps explain how temporal preferences are operationalized in daily financial life. Instead of one unified optimization problem, households often face multiple psychologically separated accounts with different rules, temptations, and levels of protection.

Separate future-oriented accounts can be beneficial because they protect long-term goals from present consumption pressure. A person may be less likely to spend retirement savings when the money is institutionally and psychologically separated from regular income. A labeled education fund may survive short-term spending temptation better than unlabeled cash. A sinking fund for insurance or property taxes may prevent future obligations from being crowded out by immediate spending.

But separate accounts can also obscure total intertemporal tradeoffs. A person may save for one future goal while borrowing for present consumption. A household may protect a long-term account while ignoring urgent near-term debt. A consumer may use buy-now-pay-later financing because the purchase feels separate from future repayment. In these cases, account segmentation can weaken the perceived connection between present action and future obligation.

Mental accounting therefore functions as a temporal governance system inside the household. It determines which future claims receive protection, which present temptations are permitted, and which tradeoffs remain visible. The best financial designs use mental accounts to protect long-term welfare while still helping households see the integrated consequences of their choices.

Mental Accounting and Financial Planning

Although mental accounting can produce inefficient decisions, it can also support beneficial habits. Separate categories for rent, emergency funds, retirement, education, insurance, debt repayment, taxes, home repair, or caregiving may help individuals maintain discipline, reduce impulsive spending, and create practical boundaries that approximate self-control. Many financial-planning tools deliberately leverage mental accounting by encouraging separate goals, labeled subaccounts, budget envelopes, and automatic transfers.

This is why mental accounting should not be treated simply as an error. In many households, a fully fungible view of money may be too abstract to guide behavior. People need categories. A household that says “all money is interchangeable” may find it harder to protect funds for future obligations. A household that labels money clearly may be more likely to pay bills, prepare for emergencies, and sustain long-term goals.

Goal-based financial planning often works because it makes future needs concrete. “Save for retirement” is abstract; “contribute $400 per month to retirement before spending begins” is operational. “Build resilience” is abstract; “maintain a three-month emergency fund” is a mental account with a rule. “Avoid overspending” is abstract; “limit dining out to this monthly category” is actionable. Mental accounting translates broad goals into usable constraints.

However, good financial planning must also include periodic integration. Mental accounts should be reviewed against total debt, total assets, interest rates, liquidity needs, insurance coverage, income stability, and future obligations. A goal label should not become immune from revision. If circumstances change, the account structure should change. The same account that once supported discipline may later create rigidity.

Effective financial planning therefore combines segmentation and integration. Segmentation helps households act. Integration helps households evaluate. The practical challenge is to design account systems that provide enough structure to support behavior without fragmenting the balance sheet so severely that households lose sight of overall welfare.

Digital Finance, Budgeting Apps, and Account Design

Digital finance has made mental accounting more visible and more designable. Banking apps, budgeting tools, prepaid cards, savings buckets, robo-advisors, employer benefits platforms, payment apps, subscription dashboards, and buy-now-pay-later products all shape how users categorize and evaluate money. These tools can either clarify financial categories or exploit them.

At their best, digital tools support constructive mental accounting. A budgeting app can make recurring obligations visible. A bank can offer labeled savings buckets for emergencies, taxes, education, or home repair. An employer can split payroll automatically across checking, retirement, savings, and debt repayment. A financial interface can show total debt and total liquid assets together while still preserving useful categories. These designs help people manage complexity without losing the whole picture.

At their worst, digital tools can fragment financial awareness. Subscription systems can move spending out of active attention. One-click purchases can weaken the pain of payment. Buy-now-pay-later tools can separate consumption from repayment. Cash-back rewards can make spending feel like earning. Store cards and platform credits can trap money in narrow accounts that encourage additional purchases. App interfaces can emphasize available balance while hiding upcoming obligations.

The ethical significance is substantial. Digital financial design does not merely present information; it creates the mental accounts through which users experience financial reality. A platform decides which balances are salient, which costs are delayed, which categories are highlighted, which warnings appear, and whether users see total financial exposure. These decisions can support welfare or increase vulnerability.

Responsible digital finance should help users see both categories and totals. It should support goals without hiding opportunity costs. It should make debt, fees, subscriptions, and repayment obligations visible. It should avoid exploiting account labels to encourage unnecessary spending. Mental accounting is powerful enough that interface design becomes part of household financial governance.

Mental Accounting and Behavioral Policy

Public policy and financial institutions increasingly incorporate insights from mental accounting when designing savings products, retirement systems, tax programs, benefit payments, consumer credit rules, and financial interfaces. Labeled savings accounts, automatic transfers, payroll splitting, purpose-specific incentives, matched savings, and tax-preferred accounts all align with the way people naturally categorize money.

These approaches connect closely to Self-Control and Commitment Devices and Nudge Theory and Behavioral Public Policy. Instead of trying to eliminate mental accounting, well-designed institutions may work with it. They can create account structures that protect emergency savings, encourage retirement contributions, separate tax obligations, support education planning, or help households allocate windfalls across debt, saving, and consumption.

Tax refunds offer a clear example. A refund arrives as a lump sum, which often activates a windfall account. Policy design can prompt refund splitting: part to checking, part to savings, part to retirement, part to debt repayment. This approach does not require households to become fully fungible optimizers. It uses mental accounting to make multiple uses salient at the decision point.

Consumer credit policy can also benefit from mental accounting insight. If households separate debt accounts from savings accounts, disclosures should make the full balance-sheet cost visible. Credit-card statements, payment apps, and budgeting tools can show how preserving savings while revolving high-interest debt affects total financial position. The goal is not to shame households, but to clarify tradeoffs that mental accounts may obscure.

Benefit policy must be careful. Purpose-specific accounts can protect funds for food, housing, childcare, education, or health. But overly rigid restrictions can reduce household flexibility and dignity. A household facing real scarcity may need discretion to allocate money across urgent needs. Mental accounting can support welfare, but paternalistic account restrictions can also harm people whose lives do not fit institutional categories.

Behavioral policy should therefore ask whether an account label expands agency or narrows it. The best designs help households protect goals they endorse, understand tradeoffs, and preserve flexibility under hardship.

Ethical Questions: Discipline, Exploitation, and Household Vulnerability

Mental accounting raises ethical questions because account labels can be used to help people or to exploit them. A labeled emergency fund can support resilience. A store credit can encourage additional spending. A retirement default can increase long-term security. A subscription structure can exploit inertia. A savings bucket can protect a goal. A promotional rebate can make unnecessary spending feel justified.

The ethical distinction depends on whose welfare the account structure serves. If a financial institution helps users protect funds for emergencies, see total debt, and allocate windfalls thoughtfully, it is using mental accounting in a user-aligned way. If it uses labels, rewards, credits, or friction to increase spending, obscure costs, or trap users in narrow spending channels, it is exploiting mental accounting.

Household vulnerability matters. Low-income households, households with irregular income, people carrying high-cost debt, and people facing medical, housing, caregiving, or employment instability may experience mental accounting differently from affluent households. A rigid account structure that supports discipline for one household may create hardship for another. A withdrawal penalty that protects savings for one person may punish another person facing emergency need.

This means mental accounting should not be used to moralize household behavior. Preserving savings while carrying debt may look inefficient from a spreadsheet perspective, but liquidity can be a rational response to insecurity. Spending a windfall may look present-biased, but it may meet overdue needs or restore dignity. Behavioral analysis should be paired with structural awareness.

Ethical financial design should make tradeoffs visible without coercion. It should support reflective goals while preserving meaningful flexibility. It should not use behavioral insights to manipulate users into higher fees, unnecessary purchases, or exploitative credit. The most important question is not whether a design changes behavior. It is whether the behavior change improves welfare under the user’s real conditions.

Empirical and Policy-Evaluation Lens

A professional economist-facing treatment of mental accounting should ask what can be measured, identified, estimated, and evaluated. Mental accounting can be studied through household financial records, banking app data, tax refund behavior, credit-card repayment, savings-bucket adoption, budgeting tools, field experiments, survey experiments, and administrative program data.

The empirical challenge is that mental accounts are often unobserved. Researchers may see account balances, transactions, debt, income, and savings, but the psychological meaning attached to each account must be inferred or measured through design. A savings account may be labeled “vacation” in an app, but the household’s emotional meaning may be broader. A checking balance may include money mentally reserved for rent, bills, gifts, or debt. Observed balances do not automatically reveal subjective categories.

Useful research designs include experiments that vary labels, default allocations, refund-splitting prompts, account naming, payment framing, debt-savings dashboards, or spending-category feedback. Researchers can compare behavior under segmented account structures with behavior under integrated balance-sheet views. They can test whether labels increase savings, reduce spending, increase debt repayment, or improve household resilience.

Policy evaluation should distinguish narrow optimization from welfare. Paying down debt may be financially optimal under known interest rates, but preserving liquidity may be welfare-improving under income risk. Spending a windfall may look inefficient but may satisfy urgent needs. A labeled savings account may increase savings but reduce flexibility. Evaluation must consider financial outcomes, stress, liquidity, hardship, autonomy, and distributional effects.

Heterogeneity is central. Mental accounting may help present-biased households protect savings. It may help households with stable income plan future expenses. It may harm households facing volatile income if funds become psychologically or institutionally locked away. It may help people who want budgeting structure and frustrate those whose needs change quickly. Average effects are not enough.

A rigorous evaluation should ask: What label was applied? What alternative uses became more or less salient? Did total wealth improve? Did high-cost debt fall? Did liquidity fall too much? Did households experience less stress or more constraint? Did the design support user-endorsed goals? These questions turn mental accounting from a descriptive concept into a serious policy and institutional design framework.

An Analytical Framework for Mental Accounting

A simple way to formalize mental accounting is to distinguish between integrated wealth evaluation and account-based evaluation. Let total wealth be:

W = \sum_{k=1}^{K} w_k

\]

Interpretation: Total wealth is the sum of resources held across accounts, whether those accounts are formal bank accounts or psychological categories.

Under strict fungibility, utility would depend on total wealth, total consumption, and total liabilities. Under mental accounting, however, the individual evaluates outcomes partly within each account:

U = \sum_{k=1}^{K} u_k(w_k, c_k, \ell_k)

\]

Interpretation: Utility depends on account balance \(w_k\), consumption from account \(c_k\), and the label or meaning \(\ell_k\) attached to that account.

The label term matters because identical dollars may be evaluated differently depending on whether they are coded as wages, savings, emergency reserves, windfalls, gift money, retirement funds, or discretionary spending. This is the core departure from fungibility: the subjective account affects the decision.

A windfall can be represented as an increase in account \(j\) that carries lower subjective restraint than ordinary income. If the marginal propensity to consume from that labeled account is higher than from a core income account, then:

\frac{\partial c_j}{\partial w_j} > \frac{\partial c_i}{\partial w_i}

\]

Interpretation: Consumption rises more from windfall-labeled money than from ordinary income, even when purchasing power is identical.

Mental accounting can also generate inefficient debt behavior. Suppose a person has low-yield savings \(S\) and high-interest debt \(D\). Under a unified balance-sheet view, debt repayment should depend on the comparison between the debt interest rate \(r_D\) and the savings return \(r_S\):

r_D > r_S \Rightarrow \text{repay debt when liquidity needs are adequately protected}

\]

Interpretation: If debt is more costly than savings is rewarding, repayment may improve the household balance sheet, subject to liquidity needs.

Under rigid mental accounting, however, the household may attach a psychological penalty to using labeled savings. Let \(\phi(\ell_S)\) represent the subjective cost of drawing down savings labeled for a protected goal. Debt repayment occurs only when the financial gain exceeds the psychological penalty:

(r_D – r_S)D^{repay} > \phi(\ell_S)

\]

Interpretation: A strong account label can prevent debt repayment even when repayment is financially attractive.

A policy or product intervention can reduce inefficiency by making integrated tradeoffs visible. Let \(I\) represent an integrated balance-sheet prompt or dashboard. If the prompt reduces the psychological segmentation penalty, then:

\phi(\ell_S \mid I) < \phi(\ell_S)

\]

Interpretation: Integrated financial information can weaken rigid account boundaries and improve cross-account decision-making.

For evaluation, the treatment effect of a mental-accounting intervention can be expressed as:

\tau = E[Y_i(1) – Y_i(0)]

\]

Interpretation: The effect of a labeled account, refund prompt, dashboard, or budgeting intervention is measured by comparing outcomes with and without the intervention.

Yet the outcome \(Y_i\) should not be limited to a narrow financial metric. A broader welfare expression may include net worth, liquidity, debt cost, goal progress, stress, and flexibility:

W_i = NW_i + L_i + G_i – C_i – B_i

\]

Interpretation: Household welfare depends on net worth, liquidity, goal progress, financial cost, and behavioral or administrative burden.

This framework helps avoid simplistic conclusions. Mental accounting is not always inefficient, and fungibility is not always psychologically feasible. The strongest designs preserve useful categories while helping households recognize when account boundaries should be revised.

R Workflow: Simulating Mental Accounts, Windfalls, and Debt Decisions

The following R workflow simulates households with separate mental accounts for income, windfalls, savings, emergency reserves, and debt. It estimates how account-label strength affects windfall consumption, debt repayment, liquidity preservation, and an inefficiency gap. The workflow is designed as an economist-facing scaffold for household finance, behavioral public policy, and consumer-finance research.

# Mental Accounting in Personal Finance

# R workflow: mental accounts, windfalls, savings labels, and debt decisions

# Synthetic data only. Economist-facing research scaffold.

set.seed(1515)

n_households <- 2500

households <- data.frame(

household_id = 1:n_households,

monthly_income = runif(n_households, 2500, 6500),

liquid_savings = runif(n_households, 500, 12000),

emergency_reserve = runif(n_households, 0, 8000),

credit_card_debt = runif(n_households, 0, 9000),

windfall = runif(n_households, 0, 3500),

savings_label_strength = runif(n_households, 0.2, 1.3),

emergency_need_risk = runif(n_households, 0.02, 0.25),

present_bias = runif(n_households, 0.55, 1.00)

)

# Windfall money is treated as more spendable than regular income.

households$windfall_spent_share <- pmin(

pmax(rnorm(n_households, mean = 0.55, sd = 0.18), 0),

1

)

households$windfall_consumption <- households$windfall * households$windfall_spent_share

# Some windfall is allocated to debt, but less than under a unified balance-sheet view.

households$windfall_debt_payment <- households$windfall * (1 - households$windfall_spent_share) * 0.60

# Reluctance to use labeled savings for debt repayment rises with label strength.

households$savings_available_for_debt <- pmax(

households$liquid_savings - 3 * households$monthly_income * households$emergency_need_risk,

0

)

households$savings_used_for_debt <- ifelse(

households$credit_card_debt > 0,

households$savings_available_for_debt * pmax(0, 0.35 - 0.22 * households$savings_label_strength),

0

)

households$total_debt_payment <- pmin(

households$credit_card_debt,

households$windfall_debt_payment + households$savings_used_for_debt

)

households$remaining_debt <- pmax(

households$credit_card_debt - households$total_debt_payment,

0

)

households$remaining_liquid_savings <- pmax(

households$liquid_savings - households$savings_used_for_debt,

0

)

# Inefficiency gap: high-cost debt remains while liquid savings remain available.

households$inefficiency_gap <- ifelse(

households$remaining_debt > 0,

pmin(households$remaining_liquid_savings, households$remaining_debt),

0

)

# Approximate annual interest burden from remaining debt.

households$annual_interest_cost <- households$remaining_debt * 0.22

# Household financial-resilience index combines debt reduction and liquidity.

households$resilience_index <- households$remaining_liquid_savings +

households$emergency_reserve -

households$remaining_debt -

households$annual_interest_cost

households$label_quartile <- cut(

households$savings_label_strength,

breaks = quantile(households$savings_label_strength, probs = seq(0, 1, 0.25)),

include.lowest = TRUE,

labels = paste0("Q", 1:4)

)

group_summary <- aggregate(

cbind(

windfall_consumption,

total_debt_payment,

remaining_debt,

inefficiency_gap,

annual_interest_cost,

resilience_index

) ~ label_quartile,

data = households,

FUN = mean

)

overall_summary <- data.frame(

mean_windfall = mean(households$windfall),

mean_windfall_consumption = mean(households$windfall_consumption),

mean_debt_payment = mean(households$total_debt_payment),

mean_remaining_debt = mean(households$remaining_debt),

mean_inefficiency_gap = mean(households$inefficiency_gap),

mean_interest_cost = mean(households$annual_interest_cost),

mean_resilience_index = mean(households$resilience_index)

)

print(overall_summary)

print(group_summary)

dir.create("outputs/tables", recursive = TRUE, showWarnings = FALSE)

write.csv(households, "outputs/tables/r_mental_accounting_households.csv", row.names = FALSE)

write.csv(overall_summary, "outputs/tables/r_mental_accounting_overall_summary.csv", row.names = FALSE)

write.csv(group_summary, "outputs/tables/r_mental_accounting_label_quartile_summary.csv", row.names = FALSE)This simulation shows how psychological labels can simultaneously support savings discipline and generate inefficient debt persistence. Stronger savings labels preserve liquidity, but they can also increase the amount of high-cost debt left unpaid. The policy question is not whether labels matter; it is whether account design helps households balance discipline, liquidity, and debt reduction.

Python Workflow: Comparing Segmented and Unified Money Views

The following Python workflow compares stylized household outcomes under three regimes: segmented mental accounts, integrated balance-sheet prompts, and a unified fungible-money view. It produces synthetic household data, regime-level summaries, and treatment-effect estimates. The workflow can be extended for tax refunds, labeled savings products, budgeting apps, debt-repayment nudges, or financial-wellness programs.

# Mental Accounting in Personal Finance

# Python workflow: segmented accounts, integrated prompts, and unified money views

# Synthetic data only. Economist-facing research scaffold.

from __future__ import annotations

from pathlib import Path

import numpy as np

import pandas as pd

rng = np.random.default_rng(1515)

n_households = 3000

base = pd.DataFrame({

"household_id": np.arange(1, n_households + 1),

"monthly_income": rng.uniform(2500, 6500, n_households),

"liquid_savings": rng.uniform(500, 12000, n_households),

"emergency_reserve": rng.uniform(0, 8000, n_households),

"credit_card_debt": rng.uniform(0, 9000, n_households),

"windfall": rng.uniform(0, 3500, n_households),

"savings_label_strength": rng.uniform(0.2, 1.3, n_households),

"emergency_need_risk": rng.uniform(0.02, 0.25, n_households),

"present_bias": rng.uniform(0.55, 1.00, n_households),

})

def simulate_regime(df: pd.DataFrame, regime: str) -> pd.DataFrame:

out = df.copy()

out["regime"] = regime

if regime == "segmented_mental_accounts":

windfall_spent_share = np.clip(rng.normal(0.58, 0.18, len(out)), 0, 1)

label_penalty = out["savings_label_strength"].to_numpy()

integrated_prompt = 0.0

savings_reallocation_base = 0.32

elif regime == "integrated_balance_sheet_prompt":

windfall_spent_share = np.clip(rng.normal(0.42, 0.16, len(out)), 0, 1)

label_penalty = out["savings_label_strength"].to_numpy() * 0.65

integrated_prompt = 1.0

savings_reallocation_base = 0.46

elif regime == "unified_fungible_money":

windfall_spent_share = np.clip(rng.normal(0.25, 0.12, len(out)), 0, 1)

label_penalty = out["savings_label_strength"].to_numpy() * 0.30

integrated_prompt = 1.0

savings_reallocation_base = 0.62

else:

raise ValueError(f"Unknown regime: {regime}")

out["windfall_consumption"] = out["windfall"] * windfall_spent_share

out["windfall_debt_payment"] = out["windfall"] * (1 - windfall_spent_share) * 0.75

protected_liquidity = (

3

* out["monthly_income"].to_numpy()

* out["emergency_need_risk"].to_numpy()

)

out["savings_available_for_debt"] = np.maximum(

out["liquid_savings"].to_numpy() - protected_liquidity,

0

)

savings_use_rate = np.maximum(

0,

savings_reallocation_base - 0.22 * label_penalty + 0.05 * integrated_prompt

)

out["savings_used_for_debt"] = np.where(

out["credit_card_debt"].to_numpy() > 0,

out["savings_available_for_debt"].to_numpy() * savings_use_rate,

0

)

out["total_debt_payment"] = np.minimum(

out["credit_card_debt"].to_numpy(),

out["windfall_debt_payment"].to_numpy() + out["savings_used_for_debt"].to_numpy()

)

out["remaining_debt"] = np.maximum(

out["credit_card_debt"].to_numpy() - out["total_debt_payment"].to_numpy(),

0

)

out["remaining_liquid_savings"] = np.maximum(

out["liquid_savings"].to_numpy() - out["savings_used_for_debt"].to_numpy(),

0

)

out["inefficiency_gap"] = np.where(

out["remaining_debt"].to_numpy() > 0,

np.minimum(out["remaining_liquid_savings"].to_numpy(), out["remaining_debt"].to_numpy()),

0

)

out["annual_interest_cost"] = out["remaining_debt"] * 0.22

out["resilience_index"] = (

out["remaining_liquid_savings"]

+ out["emergency_reserve"]

- out["remaining_debt"]

- out["annual_interest_cost"]

)

out["integrated_prompt_treat"] = int(regime == "integrated_balance_sheet_prompt")

out["unified_money_treat"] = int(regime == "unified_fungible_money")

return out

frames = [

simulate_regime(base, "segmented_mental_accounts"),

simulate_regime(base, "integrated_balance_sheet_prompt"),

simulate_regime(base, "unified_fungible_money"),

]

panel = pd.concat(frames, ignore_index=True)

summary = panel.groupby("regime").agg(

households=("household_id", "count"),

mean_windfall_consumption=("windfall_consumption", "mean"),

mean_total_debt_payment=("total_debt_payment", "mean"),

mean_remaining_debt=("remaining_debt", "mean"),

mean_remaining_liquid_savings=("remaining_liquid_savings", "mean"),

mean_inefficiency_gap=("inefficiency_gap", "mean"),

mean_annual_interest_cost=("annual_interest_cost", "mean"),

mean_resilience_index=("resilience_index", "mean"),

).reset_index()

print(summary.sort_values("mean_resilience_index", ascending=False))

try:

import statsmodels.api as sm

outcomes = [

"windfall_consumption",

"total_debt_payment",

"remaining_debt",

"inefficiency_gap",

"annual_interest_cost",

"resilience_index"

]

for outcome in outcomes:

X = panel[[

"integrated_prompt_treat",

"unified_money_treat",

"monthly_income",

"liquid_savings",

"credit_card_debt",

"windfall",

"savings_label_strength",

"emergency_need_risk",

"present_bias"

]]

X = sm.add_constant(X)

model = sm.OLS(panel[outcome], X).fit(cov_type="HC1")

print(f"\nOutcome: {outcome}")

print(model.summary().tables[1])

except ImportError:

print("statsmodels is not installed; skipping regression output.")

output_dir = Path("outputs/tables")

output_dir.mkdir(parents=True, exist_ok=True)

panel.to_csv(output_dir / "synthetic_mental_accounting_household_panel.csv", index=False)

summary.to_csv(output_dir / "mental_accounting_regime_summary.csv", index=False)For analysts and policymakers, the key lesson is that people often do not behave as though money were fully fungible. Financial outcomes can differ materially depending on whether institutions reinforce segmented accounts, provide integrated balance-sheet prompts, or encourage a more unified view of money. The policy task is to improve cross-account awareness without destroying useful budgeting discipline.

Stata Replication Note: Mental Accounting and Household Financial Outcomes

For an economist-facing repository, the companion code should support Stata as well as R and Python. The article-level GitHub folder should include a Stata workflow that imports the synthetic household-regime dataset, estimates treatment effects, reports robust standard errors, and exports regression tables. A compact Stata pattern for this article would look like this:

clear all

set more off

* Mental Accounting in Personal Finance

* Stata household-finance evaluation workflow using synthetic data.

global ROOT "`c(pwd)'"

global TABLES "$ROOT/outputs/tables"

global REG "$ROOT/outputs/regression_tables"

capture mkdir "$REG"

import delimited "$TABLES/synthetic_mental_accounting_household_panel.csv", clear varnames(1)

label variable integrated_prompt_treat "Integrated balance-sheet prompt treatment"

label variable unified_money_treat "Unified fungible-money treatment"

label variable windfall_consumption "Windfall consumption"

label variable total_debt_payment "Total debt payment"

label variable remaining_debt "Remaining credit-card debt"

label variable inefficiency_gap "Debt-savings inefficiency gap"

label variable annual_interest_cost "Annual interest cost"

label variable resilience_index "Financial resilience index"

local controls monthly_income liquid_savings credit_card_debt windfall savings_label_strength emergency_need_risk present_bias

local outcomes windfall_consumption total_debt_payment remaining_debt inefficiency_gap annual_interest_cost resilience_index

tempname handle

postfile `handle' str55 outcome str55 term double estimate double std_error double p_value double n using "$REG/stata_mental_accounting_estimates.dta", replace

foreach y of local outcomes {

regress `y' integrated_prompt_treat unified_money_treat `controls', vce(robust)

foreach x in integrated_prompt_treat unified_money_treat {

local b = _b[`x']

local se = _se[`x']

local p = 2 * ttail(e(df_r), abs(_b[`x'] / _se[`x']))

local n = e(N)

post `handle' ("`y'") ("`x'") (`b') (`se') (`p') (`n')

}

}

postclose `handle'

use "$REG/stata_mental_accounting_estimates.dta", clear

export delimited using "$REG/stata_mental_accounting_estimates.csv", replace

* Heterogeneity by savings-label strength.

import delimited "$TABLES/synthetic_mental_accounting_household_panel.csv", clear varnames(1)

xtile label_quartile = savings_label_strength, nq(4)

tempname h

postfile `h' str30 group str55 term double estimate double std_error double p_value double n using "$REG/stata_mental_accounting_label_heterogeneity.dta", replace

forvalues q = 1/4 {

regress inefficiency_gap integrated_prompt_treat unified_money_treat `controls' if label_quartile == `q', vce(robust)

foreach x in integrated_prompt_treat unified_money_treat {

local b = _b[`x']

local se = _se[`x']

local p = 2 * ttail(e(df_r), abs(_b[`x'] / _se[`x']))

local n = e(N)

post `h' ("label_q`q'") ("`x'") (`b') (`se') (`p') (`n')

}

}

postclose `h'

use "$REG/stata_mental_accounting_label_heterogeneity.dta", clear

export delimited using "$REG/stata_mental_accounting_label_heterogeneity.csv", replace

display "Stata mental-accounting household-finance workflow complete."The purpose of including Stata is to make the repository useful to economists, household-finance researchers, consumer-protection analysts, public-policy researchers, and graduate-level applied researchers who commonly work across Stata, R, and Python. The full repository scaffold should include identification notes, robustness plans, replication instructions, synthetic household panels, treatment-effect estimation, savings-label heterogeneity, debt-savings inefficiency diagnostics, windfall-use analysis, and welfare/resilience summaries.

GitHub Repository

The companion repository provides reproducible scaffolding for the computational side of this article, including synthetic household-finance datasets, mental-accounting simulations, windfall-use models, debt-savings inefficiency diagnostics, integrated balance-sheet prompt workflows, treatment-effect estimation, robustness checks, Stata/R/Python workflows, SQL metadata structures, and scientific-computing examples for behavioral economics research.

Complete Code Repository

This article is supported by an article-level folder in the Behavioral Economics computational repository, with synthetic household-finance and mental-accounting datasets, causal-inference workflows, windfall-spending simulations, debt-savings inefficiency diagnostics, integrated balance-sheet prompts, econometric identification notes, policy-evaluation scripts, robustness and sensitivity checks, Stata/R/Python workflows, SQL metadata structures, and scientific-computing examples for studying mental accounting, money fungibility, household budgeting, windfalls, labeled savings, consumer debt, emergency reserves, behavioral public policy, financial planning, and institutional design.

Interpretive Limits and Cautions

Mental accounting is a powerful concept, but it should not be used carelessly. Not every departure from fungibility is a mistake. Households may preserve cash while carrying debt because they face income volatility, medical risk, unstable housing, limited credit access, or fear of future hardship. Liquidity has value, especially for households living under uncertainty. A spreadsheet calculation that ignores liquidity risk may misread prudent behavior as irrational behavior.

There is also a risk of moralizing household finance. Mental accounting should not become a way to blame people for financial stress while ignoring wages, housing costs, healthcare costs, debt structures, predatory credit, income instability, or inadequate social protection. Behavioral explanations are strongest when paired with structural analysis. Household choices occur within constraints.

Mental accounting can also be beneficial. Budget categories, savings envelopes, labeled accounts, and automatic transfers may help people act on long-term goals. A fully fungible view of money may be economically elegant but psychologically unusable for many households. The goal is not to eliminate mental accounts. The goal is to design them intelligently.

Financial institutions and digital platforms should also be evaluated critically. A budgeting tool that helps users protect emergency savings may improve welfare. A payment platform that fragments costs, hides debt, or encourages spending from store-specific credits may exploit mental accounting. The same behavioral mechanism can support agency or undermine it.

Finally, policy evaluation must distinguish financial optimization from welfare. Paying down debt may reduce interest costs, but preserving liquidity may reduce anxiety and hardship. Spending a windfall may look inefficient, but it may meet urgent household needs. A behavioral intervention should improve real welfare, not merely make households conform to a narrow model of optimization.

Conclusion

Mental accounting shows that financial behavior is shaped not only by prices, balances, and interest rates, but by the psychological categories through which people interpret money. Individuals often divide resources into distinct mental accounts, treat windfalls differently from wages, protect labeled funds, and evaluate spending within categories rather than across the full balance sheet. These patterns reveal a powerful departure from the classical assumption that money is fully fungible.

The broader significance of mental accounting lies in showing that behavioral inconsistencies are not always random mistakes. They are often structured by the cognitive strategies people use to manage complex financial lives. Mental accounts can generate inefficiency when they block sensible reallocation, but they can also support discipline when they protect valued goals. The same account boundary can be helpful in one context and harmful in another.

The mature lesson is not that households should abandon categories. Categories are often necessary for planning, self-control, and resilience. The lesson is that categories should remain accountable to the household’s full financial position. Good financial design should preserve useful mental accounts while making cross-account tradeoffs visible, especially when high-cost debt, liquidity risk, windfalls, and long-term savings are involved.

In that sense, mental accounting offers one of the clearest bridges between behavioral economics, household finance, consumer protection, digital financial design, and public policy. It reminds us that money is not experienced only as an abstract unit of exchange. It is experienced through purpose, identity, obligation, security, reward, fear, and hope.

Related Articles

- Behavioral Economics

- Bounded Rationality in Economic Decision-Making

- Framing Effects in Consumer Choice

- Present Bias and Immediate Reward

- Time Discounting and Long-Term Decision-Making

- Self-Control and Commitment Devices

- Behavioral Finance and Investor Psychology

- Nudge Theory and Behavioral Public Policy

- Choice Architecture and Decision Environments

- Behavioral Design in Technology Systems

Further Reading

- Heath, C. and Soll, J.B. (1996) ‘Mental budgeting and consumer decisions’, Journal of Consumer Research, 23(1), pp. 40–52. Available at: https://academic.oup.com/jcr/article-abstract/23/1/40/1817321.

- Kahneman, D. (2011) Thinking, Fast and Slow. New York: Farrar, Straus and Giroux. Available at: https://us.macmillan.com/books/9780374533557/thinkingfastandslow.

- Prelec, D. and Loewenstein, G. (1998) ‘The red and the black: Mental accounting of savings and debt’, Marketing Science, 17(1), pp. 4–28. Available at: https://pubsonline.informs.org/doi/10.1287/mksc.17.1.4.

- Shefrin, H.M. and Thaler, R.H. (1988) ‘The behavioral life-cycle hypothesis’, Economic Inquiry, 26(4), pp. 609–643. Available at: https://onlinelibrary.wiley.com/doi/10.1111/j.1465-7295.1988.tb01520.x.

- Thaler, R.H. (1985) ‘Mental accounting and consumer choice’, Marketing Science, 4(3), pp. 199–214. Available at: https://pubsonline.informs.org/doi/10.1287/mksc.4.3.199.

- Thaler, R.H. (1990) ‘Anomalies: Saving, fungibility, and mental accounts’, Journal of Economic Perspectives, 4(1), pp. 193–205. Available at: https://www.aeaweb.org/articles?id=10.1257/jep.4.1.193.

- Thaler, R.H. (1999) ‘Mental accounting matters’, Journal of Behavioral Decision Making, 12(3), pp. 183–206. Available at: https://onlinelibrary.wiley.com/doi/10.1002/%28SICI%291099-0771%28199909%2912%3A3%3C183%3A%3AAID-BDM318%3E3.0.CO%3B2-F.

- Thaler, R.H. (2015) Misbehaving: The Making of Behavioral Economics. New York: W.W. Norton. Available at: https://wwnorton.com/books/misbehaving/.

- Thaler, R.H. (n.d.) ‘Mental accounting’, Encyclopaedia Britannica. Available at: https://www.britannica.com/topic/mental-accounting.

References

- Heath, C. and Soll, J.B. (1996) ‘Mental budgeting and consumer decisions’, Journal of Consumer Research, 23(1), pp. 40–52. Available at: https://academic.oup.com/jcr/article-abstract/23/1/40/1817321.

- Kahneman, D. (2011) Thinking, Fast and Slow. New York: Farrar, Straus and Giroux. Available at: https://us.macmillan.com/books/9780374533557/thinkingfastandslow.

- Prelec, D. and Loewenstein, G. (1998) ‘The red and the black: Mental accounting of savings and debt’, Marketing Science, 17(1), pp. 4–28. Available at: https://pubsonline.informs.org/doi/10.1287/mksc.17.1.4.

- Shefrin, H.M. and Thaler, R.H. (1988) ‘The behavioral life-cycle hypothesis’, Economic Inquiry, 26(4), pp. 609–643. Available at: https://onlinelibrary.wiley.com/doi/10.1111/j.1465-7295.1988.tb01520.x.

- Thaler, R.H. (1985) ‘Mental accounting and consumer choice’, Marketing Science, 4(3), pp. 199–214. Available at: https://pubsonline.informs.org/doi/10.1287/mksc.4.3.199.

- Thaler, R.H. (1990) ‘Anomalies: Saving, fungibility, and mental accounts’, Journal of Economic Perspectives, 4(1), pp. 193–205. Available at: https://www.aeaweb.org/articles?id=10.1257/jep.4.1.193.

- Thaler, R.H. (1999) ‘Mental accounting matters’, Journal of Behavioral Decision Making, 12(3), pp. 183–206. Available at: https://onlinelibrary.wiley.com/doi/10.1002/%28SICI%291099-0771%28199909%2912%3A3%3C183%3A%3AAID-BDM318%3E3.0.CO%3B2-F.

- Thaler, R.H. (2015) Misbehaving: The Making of Behavioral Economics. New York: W.W. Norton. Available at: https://wwnorton.com/books/misbehaving/.

- Thaler, R.H. (n.d.) ‘Mental accounting’, Encyclopaedia Britannica. Available at: https://www.britannica.com/topic/mental-accounting.