Last Updated May 20, 2026

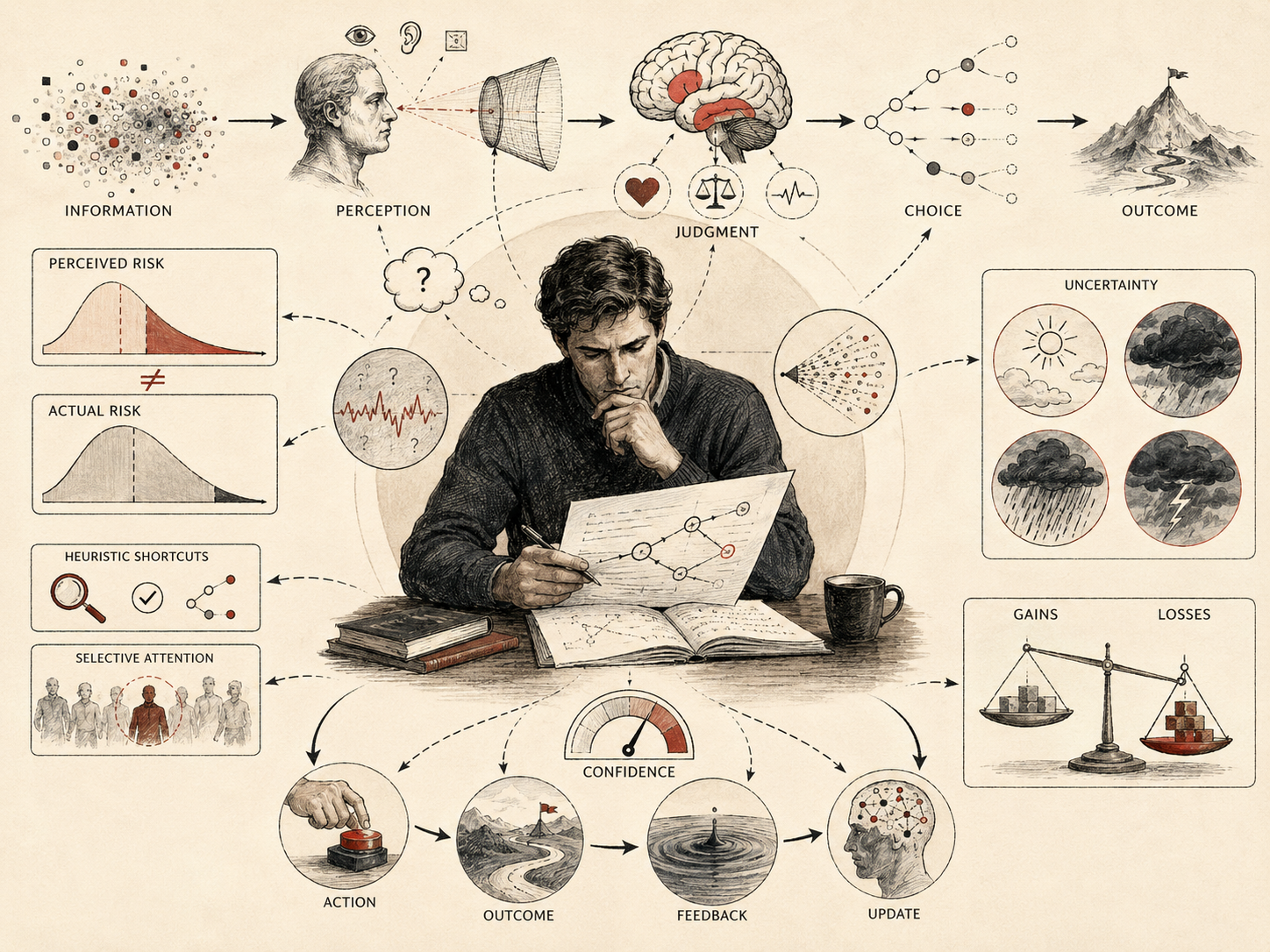

Risk perception refers to the cognitive, emotional, social, and contextual processes through which individuals interpret, evaluate, and respond to uncertain outcomes. Rather than calculating probability and consequence in a purely objective way, human beings translate uncertainty into subjective judgments about danger, opportunity, loss, control, trust, responsibility, and acceptable action. These judgments shape decisions in domains ranging from health, finance, technology, climate, public safety, infrastructure, artificial intelligence, and environmental policy to everyday personal choice.

In cognitive psychology, risk perception sits at the intersection of judgment, uncertainty, attention, affect, memory, trust, framing, and decision making. Classical economic models often assumed that people evaluate risk through formal probability calculations or expected value, but decades of psychological research have shown that actual risk judgments are shaped by heuristics, affective response, reference points, framing, prior experience, institutional trust, social amplification, and context. Risk is therefore not simply read off the environment. It is cognitively constructed.

Understanding how individuals perceive risk provides insight into why real-world decision behavior often diverges from idealized rational models. It helps explain why statistically rare events can feel overwhelmingly threatening, why familiar dangers are often discounted, why losses weigh so heavily, why trust can change risk response, and why communication about climate, disease, technology, finance, infrastructure, or public safety can succeed or fail depending on how uncertainty is presented. These themes connect directly to decision making, heuristics, cognitive bias, mental models, and behavioral economics.

Main Library

Publications

Article Map

Cognitive Psychology

Related Topic

Behavioral Economics

Related Topic

Artificial Intelligence Systems

Related Topic

Data Systems & Analytics

Risk perception matters because uncertain situations rarely arrive as clean numerical problems. They arrive as warnings, stories, forecasts, losses, memories, images, institutional messages, expert claims, conflicting sources, and lived vulnerabilities. Cognitive psychology helps explain how the mind turns those signals into judgments that feel urgent, distant, controllable, inevitable, tolerable, unfair, or unacceptable.

The cognitive nature of risk perception

Risk perception arises from the interaction of several cognitive processes that interpret uncertain outcomes. People do not directly perceive risk in the environment the way they perceive color, sound, or motion. Instead, they construct risk judgments through mental representations of probability, consequence, uncertainty, controllability, familiarity, dread, benefit, trust, and personal relevance.

These judgments often involve at least five interrelated components:

- Probability estimation — how likely an outcome appears to be.

- Consequence evaluation — how severe, costly, irreversible, or morally significant the outcome appears.

- Affective interpretation — how threatening, alarming, acceptable, or emotionally charged the outcome feels.

- Control appraisal — whether the risk seems avoidable, manageable, voluntary, or imposed.

- Trust appraisal — whether the source, system, institution, or expert managing the risk appears credible.

These components are not processed independently. Emotional reactions, prior experiences, media exposure, social cues, institutional history, and cognitive shortcuts can reshape probability judgments themselves. This helps explain why people may fear a highly publicized but statistically rare event while underestimating a more common and consequential danger.

Risk perception is therefore not simply about numeric probability. It is about how uncertainty is represented within a mind that must act despite incomplete knowledge. A probability may be understood mathematically, but perceived risk depends on whether the possible outcome feels catastrophic, unjust, unfamiliar, imposed, uncontrollable, or institutionally mishandled.

This is why risk perception cannot be reduced to individual irrationality. Some people perceive higher risk because they have lived through harm, distrust institutions for historically justified reasons, face unequal exposure, lack protective resources, or understand consequences that formal models fail to capture. Cognitive psychology must therefore distinguish biased judgment from situated judgment under unequal vulnerability.

Heuristics and risk judgments

Human beings rarely evaluate risk through explicit statistical reasoning alone. More often, they rely on cognitive shortcuts, or heuristics, that simplify judgment under uncertainty. These shortcuts are not inherently irrational. They are adaptive in many everyday situations because they allow people to act when time, information, numeracy, and attention are limited.

Several heuristics are especially important for risk perception:

- Availability heuristic — events that come easily to mind are judged as more probable or more threatening.

- Representativeness heuristic — probability judgments are shaped by similarity to familiar patterns, categories, or stereotypes.

- Affect heuristic — positive or negative feelings influence judgments of both risk and benefit.

- Anchoring — initial numbers, examples, or comparisons influence later estimates.

- Framing — the same information can produce different judgments depending on whether it is presented as a gain, loss, survival rate, failure rate, safety improvement, or harm reduction.

These shortcuts often reduce the cost of decision making under uncertainty. But they can also generate systematic distortions. A vivid example, dramatic story, recent disaster, emotionally charged image, or high-status source can shift perceived risk even when objective probabilities remain unchanged.

For that reason, heuristics are central to understanding why risk judgments are often fast, intuitive, and compelling while still departing from formal probabilistic reasoning. They show how risk is made psychologically available, not only statistically measurable.

Heuristics also interact with social conditions. A person repeatedly exposed to hazardous work, unsafe housing, medical neglect, environmental contamination, or institutional failure may not be “overreacting” when risk feels highly available. Their availability heuristic may be built from real exposure. A responsible account of risk perception must therefore ask what experiences made a risk cognitively vivid.

Risk perception and cognitive bias

Risk perception is shaped by recurring cognitive biases. These biases influence how uncertainty is interpreted and often produce structured deviations from more formally rational judgment.

Common biases affecting risk perception include:

- Loss aversion — losses are experienced as more significant than equivalent gains.

- Overconfidence — people overestimate their knowledge, predictive accuracy, or control.

- Probability neglect — attention is drawn more strongly to outcome severity than to likelihood.

- Optimism bias — individuals may believe that bad outcomes are less likely to happen to them than to others.

- Normalcy bias — people may underreact to warnings because they expect ordinary conditions to continue.

- Confirmation bias — people interpret risk information in ways that preserve existing beliefs or identities.

- Framing effects — judgments shift depending on whether outcomes are presented as gains or losses.

These patterns matter because they show that misjudgments of risk are often not random mistakes. They are regular consequences of how cognition simplifies uncertainty, evaluates threat, encodes value, and protects coherent belief systems.

Bias does not mean that emotion is always wrong or calculation is always right. Formal models may omit lived vulnerability, structural inequality, long-term uncertainty, or low-probability catastrophic outcomes. Conversely, intuitive risk judgment may overreact to vividness, salience, or immediate fear. The problem is not emotion versus reason. The problem is calibration: whether perceived risk is appropriately aligned with probability, consequence, uncertainty, exposure, vulnerability, and moral significance.

This is why risk perception has become a major area of research in judgment, behavioral economics, communication, public policy, and systems governance.

Formalizing risk perception: probability, value, and subjective weighting

Risk perception can be clarified through formal models that distinguish objective uncertainty from subjective judgment. In a simple expected-value formulation, an option with possible outcomes \(x_i\) and probabilities \(p_i\) can be represented as:

EV=\sum_{i=1}^{n}p_i x_i

\]

Interpretation: Expected value combines outcomes and probabilities into a formal benchmark for choice under risk.

But perceived risk rarely follows expected value alone. Individuals may psychologically overweight or underweight probabilities, respond asymmetrically to losses, and treat consequences differently depending on affect, control, trust, and framing. A simplified subjective-risk formulation can be written as:

R_s=\sum_{i=1}^{n}w(p_i)v(x_i)

\]

Interpretation: Subjective risk \(R_s\) depends on psychologically weighted probability \(w(p_i)\) and subjective value or cost \(v(x_i)\), not only raw probability and objective outcome.

Loss aversion can be represented with a value function of the form:

v(x)=

\begin{cases}

x^{\alpha}, & x\geq 0\\

-\lambda(-x)^{\beta}, & x<0

\end{cases}

\]

Interpretation: When \(\lambda>1\), losses loom larger than equivalent gains, helping explain why risk framed as potential loss can feel especially urgent.

One can also model perceived risk as a combination of judged likelihood, perceived consequence, affect, dread, controllability, and trust:

\hat{R}=\gamma_1P+\gamma_2C+\gamma_3A+\gamma_4D-\gamma_5K-\gamma_6T

\]

Interpretation: Perceived risk \(\hat{R}\) may rise with subjective probability \(P\), consequence \(C\), affective intensity \(A\), and dread \(D\), while falling when controllability \(K\) and trust \(T\) are high.

Probability distortion can be represented as:

\Delta_p=\hat{p}-p

\]

Interpretation: Probability distortion \(\Delta_p\) measures the gap between subjective probability \(\hat{p}\) and stated or modeled probability \(p\).

Protective action can be modeled as a probabilistic response to perceived risk and communication conditions:

Pr(A=1)=\frac{1}{1+e^{-(\beta_0+\beta_1\hat{R}+\beta_2T+\beta_3K+\beta_4Q-\beta_5U)}}

\]

Interpretation: The probability of protective action increases with perceived risk \(\hat{R}\), trust \(T\), controllability \(K\), and message clarity \(Q\), but may fall when ambiguity \(U\) is high.

These models are simplified, but useful. They make visible the difference between formal risk, perceived risk, emotional risk, communicated risk, and action-guiding risk.

Risk perception and uncertainty

Risk perception becomes especially complex when individuals face deep uncertainty rather than known probabilities. In many real-world situations, probabilities cannot be estimated precisely, outcomes are interdependent, and the systems involved are dynamic rather than stable.

Examples include:

- financial market behavior;

- technological innovation;

- climate change risk;

- public health emergencies;

- geopolitical instability;

- infrastructure failure;

- environmental contamination;

- algorithmic and artificial-intelligence systems;

- institutional collapse or policy failure.

Under these conditions, people rely more heavily on prior experience, analogy, narrative framing, institutional trust, social signals, and mental models. Formal calculation may still matter, but it rarely settles the judgment because uncertainty is distributed across probability, consequence, timing, scope, exposure, vulnerability, and reversibility.

Risk perception under uncertainty is therefore not a special exception to judgment. It is one of the clearest examples of how human cognition normally operates when the world is too complex for complete probabilistic control.

Uncertainty also changes the ethics of risk communication. A communicator who pretends uncertainty does not exist may damage trust when outcomes change. A communicator who overwhelms people with uncertainty may produce paralysis. Effective communication must make uncertainty visible without making action impossible.

The psychometric paradigm and perceived hazards

A major tradition in risk-perception research is the psychometric paradigm, associated with work by Fischhoff, Slovic, Lichtenstein, Read, Combs, and others. This approach asks people to evaluate hazards across dimensions such as dread, familiarity, controllability, voluntariness, catastrophic potential, immediacy, equity, and perceived benefit.

The importance of this tradition is that it showed risk perception is not random. People evaluate hazards along structured psychological dimensions. A technology or activity may be judged risky not only because harm is likely, but because the risk is involuntary, catastrophic, unknown, delayed, unevenly distributed, or imposed by institutions that are not trusted.

Common psychometric dimensions include:

- Dread — whether the risk evokes fear, catastrophe, fatality, or lack of control.

- Unknown risk — whether consequences are uncertain, delayed, invisible, or scientifically unresolved.

- Controllability — whether people believe they can personally reduce the risk.

- Voluntariness — whether people choose the risk or have it imposed on them.

- Equity — whether risks and benefits are distributed fairly.

- Benefit — whether the activity producing the risk is seen as useful or necessary.

This framework is especially useful for public policy because technical risk estimates often fail to explain public concern. A community may reject a hazard not because it misunderstands probability, but because it perceives the hazard as involuntary, poorly governed, unfairly distributed, or historically linked to institutional neglect.

The psychometric paradigm therefore helps move risk research beyond the false opposition between “expert facts” and “public fear.” It shows that perceived risk includes dimensions of meaning that formal probability alone does not capture.

Affect, dread, and risk as feeling

Affective response plays a central role in risk perception. People often evaluate risky activities partly through the immediate feeling attached to them. If an activity evokes fear, disgust, anger, dread, or moral alarm, perceived risk tends to rise. If it evokes familiarity, trust, benefit, excitement, or control, perceived risk may fall.

The affect heuristic explains why perceived risk and perceived benefit are often inversely related. When people feel positively about an activity, they may judge its benefits as high and its risks as low. When they feel negatively, they may judge its risks as high and its benefits as low. This can occur even when the technical evidence is more mixed.

Affect is not merely a distortion. It can carry information from experience, memory, and social learning. Fear may warn of real danger. Dread may reflect awareness of irreversible harm. Anger may reflect perceived injustice. But affect can also be manipulated by vivid imagery, sensational media, political framing, or isolated anecdotes.

Slovic and Peters distinguish risk as analysis from risk as feeling. Risk as analysis involves deliberation, probability, evidence, and formal reasoning. Risk as feeling involves intuitive response, emotion, imagery, and immediate appraisal. Real-world risk judgment usually involves both.

The central question is not whether affect should be removed from risk perception. It is whether affect is calibrated, reflective, and connected to evidence rather than detached from context or exploited by manipulation.

Risk perception and behavioral economics

Research on risk perception played a major role in the development of behavioral economics. Daniel Kahneman and Amos Tversky showed that individuals systematically violate the assumptions of classical rational-choice theory when judging uncertain outcomes.

Their work on prospect theory demonstrated that individuals evaluate gains and losses relative to reference points and show asymmetric sensitivity to losses. This altered how economists and psychologists understood risk because it showed that people do not simply maximize objective expected value. They interpret outcomes through framing, reference dependence, subjective probability weighting, and loss aversion.

Key behavioral-economic ideas relevant to risk perception include:

- Reference dependence — outcomes are evaluated relative to a perceived baseline.

- Loss aversion — losses generally carry more psychological weight than equivalent gains.

- Diminishing sensitivity — the subjective impact of additional gains or losses often decreases as magnitude grows.

- Probability weighting — small probabilities may be overweighted and moderate or large probabilities underweighted.

- Framing effects — choices shift when equivalent outcomes are described differently.

These insights transformed economic theory by incorporating psychological structure into models of human choice. The integration of cognitive psychology and economic decision research is explored further in behavioral economics, where risk perception becomes part of a broader account of real decision behavior.

Behavioral economics also highlights the policy significance of risk perception. Insurance, savings, health behavior, investment, environmental policy, disaster preparation, and public-benefit design all depend on how people interpret uncertain future outcomes, not only on what probabilities are formally available.

Risk communication and public decision making

Understanding risk perception is essential for communication in public health, environmental policy, technological governance, infrastructure safety, emergency response, finance, and climate adaptation. When institutions communicate risk poorly, people may underestimate genuine dangers, distrust expert guidance, overreact to unlikely but vivid threats, or fail to take protective action.

Effective risk communication requires more than presenting statistical probabilities. It must also account for how uncertainty is interpreted emotionally, socially, and cognitively. Narratives, visual representations, comparative baselines, frequency formats, uncertainty ranges, source credibility, and contextual framing often matter as much as numerical precision.

Good risk communication should:

- state what is known, unknown, and changing;

- distinguish probability from consequence;

- use clear denominators and meaningful comparisons;

- avoid hiding uncertainty;

- avoid exaggerating certainty for short-term persuasion;

- connect risk information to actionable choices;

- acknowledge audience concerns and lived experience;

- explain who is exposed, who benefits, and who bears costs;

- preserve trust through transparency and correction.

The broader implication is that public reasoning about risk depends not only on what information is available, but on how that information is made psychologically meaningful and institutionally trustworthy.

Risk communication is also a justice issue. Communities that have experienced environmental harm, medical exploitation, policing failure, labor danger, or bureaucratic neglect may reasonably distrust official assurances. Communication that treats distrust as ignorance can deepen the very problem it tries to solve.

Risk perception in complex systems

Modern societies depend increasingly on large-scale technological, financial, environmental, and institutional systems whose risks are difficult for individuals to evaluate intuitively. Global supply chains, automated infrastructures, pandemics, climate systems, financial networks, energy grids, digital platforms, and artificial-intelligence systems all generate risks whose causal pathways are diffuse, delayed, and hard to observe directly.

As a result, institutions develop models, forecasts, sensors, dashboards, risk registers, expert advisory systems, and scenario-planning tools to supplement ordinary human judgment. These frameworks are partly compensatory: they attempt to extend cognitive capacities that, at the level of individual intuition, are poorly suited to complex systemic risk.

Even so, human interpretation remains central. Institutions still decide:

- which risks to prioritize;

- which models to trust;

- which warnings to believe;

- which thresholds count as urgent;

- which uncertainties are acceptable;

- which populations are protected first;

- which harms are treated as externalities;

- which failures are framed as rare accidents rather than system patterns.

Risk perception therefore continues to shape collective action even when formal models are present. A model can estimate hazard, but humans decide whether the hazard matters, whom it matters for, and what should be done.

The social amplification of risk framework is useful here because risk signals do not move through society unchanged. They are amplified, dampened, interpreted, politicized, commercialized, contested, and institutionalized through media, organizations, communities, experts, cultural meanings, and political structures.

Trust, inequality, and institutional risk

Trust is one of the most important conditions shaping risk perception. People are more likely to accept risk information when they trust the source, believe the process is transparent, and see the institution as competent, honest, and accountable. They are less likely to accept risk information when institutions have a history of concealment, neglect, discrimination, extraction, or harm.

This matters because risk is not evenly distributed. Some communities face higher exposure to environmental hazards, unsafe work, poor housing, inadequate healthcare, policing risk, infrastructure neglect, climate vulnerability, or algorithmic misclassification. In such contexts, heightened risk perception may reflect accurate social knowledge rather than bias.

Institutional risk perception also matters. Agencies, firms, courts, hospitals, schools, platforms, and governments all develop internal models of what counts as risk. These models determine which harms are measured, which populations are protected, which warnings are escalated, and which failures are normalized.

A serious account of risk perception therefore must ask:

- Who is exposed?

- Who benefits from the risky activity?

- Who bears the cost if the risk materializes?

- Who controls the data?

- Whose experience is treated as evidence?

- Which harms are visible to the model?

- Which communities have reason to distrust the communicator?

Risk perception is cognitive, but it is not only cognitive. It is also social, historical, and institutional. The same probability can mean different things depending on who is exposed, who is protected, and who has been believed in the past.

Risk perception and artificial intelligence systems

Artificial intelligence creates new challenges for risk perception. Many AI systems are probabilistic, opaque, data-dependent, and difficult for non-specialists to evaluate. Users may overestimate their reliability because outputs appear fluent, precise, or authoritative. Others may underestimate useful systems because the technology feels unfamiliar, intrusive, or institutionally untrustworthy.

AI risk perception involves several overlapping judgments:

- How accurate is the system?

- How uncertain is the output?

- What data shaped the model?

- What errors are likely?

- Who is harmed if the system fails?

- Can the decision be appealed or corrected?

- Does the user understand the system well enough to rely on it?

- Does the system amplify existing inequality?

Human-AI decision support therefore requires calibrated risk perception. A user needs neither blind trust nor blanket rejection. They need a usable mental model of system capability, uncertainty, failure modes, evidence quality, and accountability.

AI systems can support better risk perception when they make uncertainty visible, preserve source provenance, expose limitations, show confidence appropriately, enable contestation, and encourage verification. They can undermine risk perception when they hide uncertainty, collapse contested claims into fluent summaries, or make institutional decisions appear more objective than they are.

The key design question is whether AI systems help people perceive risk more accurately and equitably — or simply shift risk onto users who are least able to detect system failure.

Future directions in risk-perception research

Current research on risk perception increasingly integrates cognitive psychology with neuroscience, computational modeling, behavioral science, systems analysis, communication research, public policy, environmental justice, and AI governance. Neuroimaging studies examine how emotional and cognitive networks interact during uncertain choice, while computational models explore how people approximate probabilistic reasoning under limited information and limited time.

At the same time, the field is expanding into domains such as climate adaptation, sustainability, misinformation, technological governance, platform risk, public trust, long-horizon uncertainty, and complex adaptive systems. These directions matter because many consequential risks in contemporary life are not simple one-off hazards. They are systemic, distributed, cumulative, uncertain, and politically contested.

Future research will need to integrate several levels of analysis:

- individual cognition and affect;

- group identity and social norms;

- institutional trust and accountability;

- media amplification and misinformation;

- systemic exposure and unequal vulnerability;

- technical models and uncertainty communication;

- human-AI interaction and decision support;

- long-term risks that exceed ordinary intuition.

Understanding how individuals and institutions perceive risk remains essential for explaining judgment in uncertain environments and for designing systems that support better collective reasoning under complexity.

R code for risk-perception data

The following R workflow illustrates analyses relevant to risk-perception research, including subjective probability, probability distortion, consequence severity, affect, dread, controllability, trust, ambiguity, communication clarity, perceived risk, safe choice, protective action, confidence, and response time.

# Install packages if needed:

# pak::pak(c("tidyverse", "lme4", "lmerTest", "emmeans", "broom.mixed"))

library(tidyverse)

library(lme4)

library(lmerTest)

library(emmeans)

library(broom.mixed)

# Expected columns:

# participant, condition, domain, trial, scenario_id,

# objective_probability, subjective_probability,

# consequence_rating, affect_rating, dread_rating,

# familiarity_rating, controllability_rating, trust_rating,

# ambiguity_rating, communication_clarity, perceived_benefit,

# perceived_risk, choose_safe, protective_action, rt_ms, confidence

dat <- read_csv("risk_perception_trials.csv") %>%

mutate(

participant = factor(participant),

condition = factor(condition),

domain = factor(domain),

scenario_id = factor(scenario_id),

choose_safe = as.integer(choose_safe),

protective_action = as.integer(protective_action),

probability_distortion = subjective_probability - objective_probability,

risk_benefit_gap = perceived_risk - perceived_benefit,

log_rt = log(rt_ms)

)

# -----------------------------

# 1. Descriptive profile

# -----------------------------

condition_summary <- dat %>%

group_by(condition) %>%

summarise(

n_trials = n(),

participants = n_distinct(participant),

mean_objective_probability = mean(objective_probability, na.rm = TRUE),

mean_subjective_probability = mean(subjective_probability, na.rm = TRUE),

mean_probability_distortion = mean(probability_distortion, na.rm = TRUE),

mean_consequence = mean(consequence_rating, na.rm = TRUE),

mean_affect = mean(affect_rating, na.rm = TRUE),

mean_dread = mean(dread_rating, na.rm = TRUE),

mean_controllability = mean(controllability_rating, na.rm = TRUE),

mean_trust = mean(trust_rating, na.rm = TRUE),

mean_ambiguity = mean(ambiguity_rating, na.rm = TRUE),

mean_clarity = mean(communication_clarity, na.rm = TRUE),

mean_benefit = mean(perceived_benefit, na.rm = TRUE),

mean_perceived_risk = mean(perceived_risk, na.rm = TRUE),

safe_choice_rate = mean(choose_safe, na.rm = TRUE),

protective_action_rate = mean(protective_action, na.rm = TRUE),

mean_rt_ms = mean(rt_ms, na.rm = TRUE),

mean_confidence = mean(confidence, na.rm = TRUE),

.groups = "drop"

)

print(condition_summary)

# -----------------------------

# 2. Perceived-risk model

# -----------------------------

risk_model <- lmer(

perceived_risk ~

condition +

domain +

objective_probability +

subjective_probability +

consequence_rating +

affect_rating +

dread_rating +

familiarity_rating +

controllability_rating +

trust_rating +

ambiguity_rating +

communication_clarity +

perceived_benefit +

(1 | participant) +

(1 | scenario_id),

data = dat,

REML = FALSE

)

summary(risk_model)

emmeans(risk_model, ~ condition)

# -----------------------------

# 3. Probability-distortion model

# -----------------------------

distortion_model <- lmer(

probability_distortion ~

condition +

domain +

objective_probability +

affect_rating +

dread_rating +

ambiguity_rating +

communication_clarity +

trust_rating +

confidence +

(1 | participant) +

(1 | scenario_id),

data = dat,

REML = FALSE

)

summary(distortion_model)

# -----------------------------

# 4. Safe-choice model

# -----------------------------

safe_model <- glmer(

choose_safe ~

condition +

domain +

perceived_risk +

consequence_rating +

affect_rating +

dread_rating +

controllability_rating +

trust_rating +

ambiguity_rating +

perceived_benefit +

(1 | participant) +

(1 | scenario_id),

data = dat,

family = binomial(),

control = glmerControl(optimizer = "bobyqa")

)

summary(safe_model)

emmeans(safe_model, ~ condition, type = "response")

# -----------------------------

# 5. Protective-action model

# -----------------------------

action_model <- glmer(

protective_action ~

condition +

domain +

perceived_risk +

trust_rating +

communication_clarity +

controllability_rating +

ambiguity_rating +

confidence +

(1 | participant) +

(1 | scenario_id),

data = dat,

family = binomial(),

control = glmerControl(optimizer = "bobyqa")

)

summary(action_model)

emmeans(action_model, ~ condition, type = "response")

# -----------------------------

# 6. Communication-clarity model

# -----------------------------

clarity_model <- lmer(

communication_clarity ~

condition +

domain +

trust_rating +

ambiguity_rating +

objective_probability +

consequence_rating +

affect_rating +

(1 | participant) +

(1 | scenario_id),

data = dat,

REML = FALSE

)

summary(clarity_model)

# -----------------------------

# 7. Response-time model

# -----------------------------

rt_model <- lmer(

log_rt ~

condition +

domain +

perceived_risk +

ambiguity_rating +

communication_clarity +

confidence +

choose_safe +

protective_action +

(1 | participant) +

(1 | scenario_id),

data = dat,

REML = FALSE

)

summary(rt_model)

# -----------------------------

# 8. Visualization

# -----------------------------

ggplot(dat, aes(x = subjective_probability, y = perceived_risk, color = condition)) +

geom_point(alpha = 0.25) +

geom_smooth(method = "lm", se = FALSE) +

labs(

title = "Subjective probability and perceived risk",

x = "Subjective probability",

y = "Perceived risk"

) +

theme_minimal()This workflow can be adapted for framing experiments, affective-risk studies, psychometric risk-perception surveys, public-health communication, climate-risk communication, technology-risk studies, AI-risk perception, uncertainty communication, behavioral-economics tasks, and protective-action modeling. Researchers should model participant and scenario effects whenever possible because risk judgments vary strongly across people, hazards, domains, message sources, and institutional contexts.

Python code for risk-perception data

The Python examples below parallel the R workflow and are useful for framing experiments, affective-risk judgments, uncertainty-based choice tasks, public-risk communication studies, and probability-distortion analysis.

import numpy as np

import pandas as pd

import statsmodels.formula.api as smf

import statsmodels.api as sm

import matplotlib.pyplot as plt

# Expected columns:

# participant, condition, domain, trial, scenario_id,

# objective_probability, subjective_probability,

# consequence_rating, affect_rating, dread_rating,

# familiarity_rating, controllability_rating, trust_rating,

# ambiguity_rating, communication_clarity, perceived_benefit,

# perceived_risk, choose_safe, protective_action, rt_ms, confidence

df = pd.read_csv("risk_perception_trials.csv")

categorical_cols = ["participant", "condition", "domain", "scenario_id"]

for col in categorical_cols:

df[col] = df[col].astype("category")

df["choose_safe"] = df["choose_safe"].astype(int)

df["protective_action"] = df["protective_action"].astype(int)

df["probability_distortion"] = df["subjective_probability"] - df["objective_probability"]

df["risk_benefit_gap"] = df["perceived_risk"] - df["perceived_benefit"]

df["log_rt"] = np.log(df["rt_ms"])

# -----------------------------

# 1. Descriptive profile

# -----------------------------

condition_summary = (

df.groupby("condition", observed=True)

.agg(

n_trials=("perceived_risk", "size"),

participants=("participant", "nunique"),

mean_objective_probability=("objective_probability", "mean"),

mean_subjective_probability=("subjective_probability", "mean"),

mean_probability_distortion=("probability_distortion", "mean"),

mean_consequence=("consequence_rating", "mean"),

mean_affect=("affect_rating", "mean"),

mean_dread=("dread_rating", "mean"),

mean_controllability=("controllability_rating", "mean"),

mean_trust=("trust_rating", "mean"),

mean_ambiguity=("ambiguity_rating", "mean"),

mean_clarity=("communication_clarity", "mean"),

mean_benefit=("perceived_benefit", "mean"),

mean_perceived_risk=("perceived_risk", "mean"),

safe_choice_rate=("choose_safe", "mean"),

protective_action_rate=("protective_action", "mean"),

mean_rt_ms=("rt_ms", "mean"),

mean_confidence=("confidence", "mean"),

)

.reset_index()

)

print(condition_summary)

# -----------------------------

# 2. Perceived-risk model

# -----------------------------

risk_model = smf.ols(

"perceived_risk ~ condition + domain + objective_probability "

"+ subjective_probability + consequence_rating + affect_rating "

"+ dread_rating + familiarity_rating + controllability_rating "

"+ trust_rating + ambiguity_rating + communication_clarity "

"+ perceived_benefit",

data=df,

)

risk_result = risk_model.fit(

cov_type="cluster",

cov_kwds={"groups": df["participant"]},

)

print(risk_result.summary())

# -----------------------------

# 3. Probability-distortion model

# -----------------------------

distortion_model = smf.ols(

"probability_distortion ~ condition + domain + objective_probability "

"+ affect_rating + dread_rating + ambiguity_rating "

"+ communication_clarity + trust_rating + confidence",

data=df,

)

distortion_result = distortion_model.fit(

cov_type="cluster",

cov_kwds={"groups": df["participant"]},

)

print(distortion_result.summary())

# -----------------------------

# 4. Safe-choice model

# -----------------------------

safe_model = smf.glm(

"choose_safe ~ condition + domain + perceived_risk "

"+ consequence_rating + affect_rating + dread_rating "

"+ controllability_rating + trust_rating + ambiguity_rating "

"+ perceived_benefit",

data=df,

family=sm.families.Binomial(),

)

safe_result = safe_model.fit(

cov_type="cluster",

cov_kwds={"groups": df["participant"]},

)

print(safe_result.summary())

# -----------------------------

# 5. Protective-action model

# -----------------------------

action_model = smf.glm(

"protective_action ~ condition + domain + perceived_risk "

"+ trust_rating + communication_clarity + controllability_rating "

"+ ambiguity_rating + confidence",

data=df,

family=sm.families.Binomial(),

)

action_result = action_model.fit(

cov_type="cluster",

cov_kwds={"groups": df["participant"]},

)

print(action_result.summary())

# -----------------------------

# 6. Communication-clarity model

# -----------------------------

clarity_model = smf.ols(

"communication_clarity ~ condition + domain + trust_rating "

"+ ambiguity_rating + objective_probability + consequence_rating "

"+ affect_rating",

data=df,

)

clarity_result = clarity_model.fit(

cov_type="cluster",

cov_kwds={"groups": df["participant"]},

)

print(clarity_result.summary())

# -----------------------------

# 7. Response-time model

# -----------------------------

rt_model = smf.ols(

"log_rt ~ condition + domain + perceived_risk "

"+ ambiguity_rating + communication_clarity + confidence "

"+ choose_safe + protective_action",

data=df,

)

rt_result = rt_model.fit(

cov_type="cluster",

cov_kwds={"groups": df["participant"]},

)

print(rt_result.summary())

# -----------------------------

# 8. Visualization

# -----------------------------

fig, ax = plt.subplots(figsize=(8, 5))

for condition, group in df.groupby("condition", observed=True):

ax.scatter(

group["subjective_probability"],

group["perceived_risk"],

alpha=0.35,

label=str(condition),

)

ax.set_xlabel("Subjective probability")

ax.set_ylabel("Perceived risk")

ax.set_title("Subjective probability and perceived risk")

ax.legend(title="Condition")

plt.tight_layout()

plt.show()The Python workflow is intentionally transparent and extensible. It can be expanded with prospect-theory parameter estimation, probability-weighting functions, Bayesian hierarchical risk models, psychometric hazard mapping, trust and ambiguity models, response-time models, public-health communication experiments, climate-risk communication studies, AI-risk perception, and dashboards for comparing objective probability with perceived risk.

GitHub Repository

The companion repository provides reusable code and research scaffolding for studying risk perception and uncertainty in cognitive psychology, including workflows for subjective probability, probability distortion, consequence severity, affect, dread, controllability, trust, ambiguity, framing, perceived risk, safe choice, protective action, communication clarity, confidence, and response time.

Complete Code Repository

Access the full companion repository for this article, including reproducible analysis materials and multi-language code workflows for risk-perception and uncertainty research.

Applications of risk-perception research

Risk-perception research has wide applications across public health, medicine, climate adaptation, environmental communication, financial decision making, safety engineering, emergency management, public policy, technology governance, infrastructure planning, insurance, organizational decision making, and artificial intelligence.

In public health, risk perception helps explain why people adopt or reject protective behaviors, how they respond to uncertainty, and why trust in institutions shapes compliance. In climate communication, it helps explain why long-horizon systemic risk can be difficult to make psychologically salient. In finance, it helps explain loss aversion, overconfidence, panic, and underpreparation. In technology governance, it helps explain why unfamiliar technologies may provoke public concern and why familiar systems may be underestimated despite real harm.

In policy design, risk perception matters because public acceptance depends on more than technical estimates. People evaluate fairness, voluntariness, controllability, institutional trust, and who bears the burden. A technically efficient policy may fail if it ignores how risk is perceived by those most exposed.

In artificial intelligence, risk perception helps evaluate how users interpret model uncertainty, system authority, automation error, and institutional accountability. Good AI systems should not merely output recommendations. They should help users perceive uncertainty, risk, evidence, and limitation more accurately.

Across these domains, risk perception research helps explain how uncertainty becomes action-guiding judgment.

Conclusion

Risk perception is the process through which uncertain outcomes become psychologically meaningful. By combining judgments about probability, consequence, affect, dread, controllability, trust, ambiguity, and benefit, the mind translates uncertainty into action-guiding representations.

Cognitive psychology shows that these judgments are neither purely rational calculations nor mere emotional reactions. They are constructed through interacting systems of attention, memory, heuristic reasoning, value, affect, prior experience, social meaning, and institutional trust.

The central lesson is that risk is not perceived only as a number. It is perceived through models, feelings, histories, frames, relationships, institutions, and unequal exposure. Understanding risk perception therefore helps explain why individuals and institutions respond to danger, uncertainty, and possibility in ways that may diverge from formal models while still remaining deeply structured and intelligible.

Related articles

- Cognitive Psychology

- Decision Making in Cognitive Psychology

- Heuristics in Cognitive Psychology

- Cognitive Biases in Decision Making

- Mental Models in Cognitive Psychology

- Metacognition: Thinking About Thinking

- Cognitive Load and Information Processing

- Behavioral Economics

- Artificial Intelligence Systems

Further reading

- American Psychological Association (2018) Risk perception. APA Dictionary of Psychology. Available at: https://dictionary.apa.org/risk-perception.

- Finucane, M.L., Alhakami, A., Slovic, P. and Johnson, S.M. (2000) ‘The affect heuristic in judgments of risks and benefits’, Journal of Behavioral Decision Making, 13(1), pp. 1–17. Available at: https://onlinelibrary.wiley.com/doi/abs/10.1002/%28SICI%291099-0771%28200001/03%2913%3A1%3C1%3A%3AAID-BDM333%3E3.0.CO%3B2-S.

- Fischhoff, B., Slovic, P., Lichtenstein, S., Read, S. and Combs, B. (1978) ‘How safe is safe enough? A psychometric study of attitudes towards technological risks and benefits’, Policy Sciences, 9, pp. 127–152. Available at: https://link.springer.com/article/10.1007/BF00143739.

- Kahneman, D. (2011) Thinking, Fast and Slow. New York: Farrar, Straus and Giroux.

- Kahneman, D. and Tversky, A. (1979) ‘Prospect theory: An analysis of decision under risk’, Econometrica, 47(2), pp. 263–291. Available at: https://www.jstor.org/stable/1914185.

- Kasperson, R.E. et al. (1988) ‘The social amplification of risk: A conceptual framework’, Risk Analysis, 8(2), pp. 177–187. Available at: https://onlinelibrary.wiley.com/doi/10.1111/j.1539-6924.1988.tb01168.x.

- National Research Council (1989) Improving Risk Communication. Washington, DC: The National Academies Press. Available at: https://www.nationalacademies.org/publications/1189.

- Slovic, P. (1987) ‘Perception of risk’, Science, 236(4799), pp. 280–285. Available at: https://www.science.org/doi/10.1126/science.3563507.

- Slovic, P. and Peters, E. (2006) ‘Risk perception and affect’, Current Directions in Psychological Science, 15(6), pp. 322–325. Available at: https://journals.sagepub.com/doi/abs/10.1111/j.1467-8721.2006.00461.x.

- Steele, K. and Stefánsson, H.O. (2023) ‘Decision theory’, Stanford Encyclopedia of Philosophy. Available at: https://plato.stanford.edu/entries/decision-theory/.

- Tversky, A. and Kahneman, D. (1974) ‘Judgment under uncertainty: Heuristics and biases’, Science, 185(4157), pp. 1124–1131. Available at: https://www.science.org/doi/10.1126/science.185.4157.1124.

References

- American Psychological Association (2018) Risk perception. APA Dictionary of Psychology. Available at: https://dictionary.apa.org/risk-perception.

- Finucane, M.L., Alhakami, A., Slovic, P. and Johnson, S.M. (2000) ‘The affect heuristic in judgments of risks and benefits’, Journal of Behavioral Decision Making, 13(1), pp. 1–17. Available at: https://onlinelibrary.wiley.com/doi/abs/10.1002/%28SICI%291099-0771%28200001/03%2913%3A1%3C1%3A%3AAID-BDM333%3E3.0.CO%3B2-S.

- Fischhoff, B., Slovic, P., Lichtenstein, S., Read, S. and Combs, B. (1978) ‘How safe is safe enough? A psychometric study of attitudes towards technological risks and benefits’, Policy Sciences, 9, pp. 127–152. Available at: https://link.springer.com/article/10.1007/BF00143739.

- Kahneman, D. (2011) Thinking, Fast and Slow. New York: Farrar, Straus and Giroux.

- Kahneman, D. and Tversky, A. (1979) ‘Prospect theory: An analysis of decision under risk’, Econometrica, 47(2), pp. 263–291. Available at: https://www.jstor.org/stable/1914185.

- Kasperson, R.E., Renn, O., Slovic, P., Brown, H.S., Emel, J., Goble, R., Kasperson, J.X. and Ratick, S. (1988) ‘The social amplification of risk: A conceptual framework’, Risk Analysis, 8(2), pp. 177–187. Available at: https://onlinelibrary.wiley.com/doi/10.1111/j.1539-6924.1988.tb01168.x.

- National Research Council (1989) Improving Risk Communication. Washington, DC: The National Academies Press. Available at: https://www.nationalacademies.org/publications/1189.

- Slovic, P. (1987) ‘Perception of risk’, Science, 236(4799), pp. 280–285. Available at: https://www.science.org/doi/10.1126/science.3563507.

- Slovic, P. and Peters, E. (2006) ‘Risk perception and affect’, Current Directions in Psychological Science, 15(6), pp. 322–325. Available at: https://journals.sagepub.com/doi/abs/10.1111/j.1467-8721.2006.00461.x.

- Steele, K. and Stefánsson, H.O. (2023) ‘Decision theory’, Stanford Encyclopedia of Philosophy. Available at: https://plato.stanford.edu/entries/decision-theory/.

- Tversky, A. and Kahneman, D. (1974) ‘Judgment under uncertainty: Heuristics and biases’, Science, 185(4157), pp. 1124–1131. Available at: https://www.science.org/doi/10.1126/science.185.4157.1124.